Is $300K Enough to Retire? The Math Says Yes (Here's How)

You've seen the number. Northwestern Mutual's 2026 study says Americans think they need $1.46 million to retire comfortably. You've got $300,000. And if you're anything like my friend David, you read that headline, felt your chest tighten, and started Googling "jobs for 70-year-olds" at 11 p.m. on a Tuesday.

Stop Googling. Close that tab.

That $1.46 million figure is designed to scare clicks, not reflect reality. For a couple retiring at 67 with:

- $300,000 in savings

- $4,000/month combined Social Security

- 5 years of part-time work by one spouse

Result: ~$70,000 annual income by age 72 with almost zero federal taxes — that's a comfortable, sustainable retirement.

That $1.46 million figure is a headline designed to scare you into clicking, not a number that has anything to do with your actual life. For a couple retiring at 67 with $300,000 in savings, $4,000 a month in combined Social Security, and a willingness for one spouse to keep working part-time for a few years? The math tells a completely different story.

So let's actually run the numbers. Not vibes. Not scare tactics. The real, specific math for your situation.

Your $300K Isn't What You Think It Is

Mental Shift: $300K Is Your Supplement, Not Your Paycheck

Your real retirement income is Social Security. At $4,000/month combined, that's $48,000/year before touching savings — 25% above the average retired couple's benefit.

Here's the mental shift that changes everything. $300,000 is not your retirement income. It's your supplement.

Your real retirement income is Social Security. At $4,000 per month combined, you're bringing in $48,000 a year before you touch a single dollar of savings. That puts you roughly 25% above the average retired couple's Social Security benefit of $3,208 per month. Not too shabby.

Think of it this way. Your Social Security is the paycheck. Your $300,000 portfolio is the savings account you dip into when the paycheck doesn't quite cover everything. And that part-time job one of you plans to keep for five years? That's the secret weapon nobody talks about. More on that in a minute.

Reality Check

The median retirement savings for households aged 55 to 64 is $185,000, according to the Federal Reserve's Survey of Consumer Finances. With $300,000, you're ahead of most American households approaching retirement. You're not behind. You're ahead.

The Part-Time Work Shield: Your Most Powerful Asset

Financial planners love to talk about "sequence-of-returns risk." That's a fancy way of saying: if the market crashes in your first few years of retirement and you're selling investments to pay bills, your portfolio may never fully recover.

This is the single biggest threat to a $300,000 nest egg. And your part-time job neutralizes it almost entirely.

Here's why. With $4,000 per month from Social Security and $833 per month from part-time work, you're pulling in $4,833 a month. That's about $58,000 a year, without withdrawing anything from your portfolio. And here's something a lot of people don't realize: because you've hit full retirement age at 67, there's no earnings limit on your Social Security. You keep every dollar of both.

If your annual expenses stay at or below $58,000, your $300,000 sits completely untouched for five full years. Just growing.

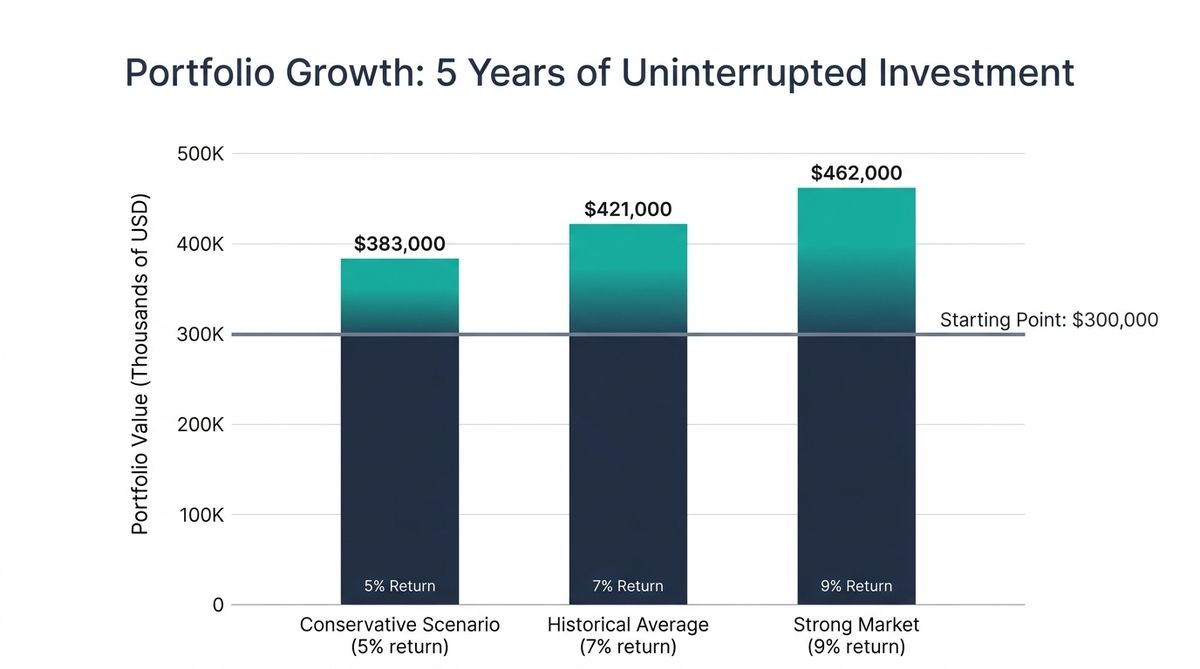

So what happens to $300,000 left alone in a 70/30 stock-and-bond portfolio for five years?

| Scenario | Annual Return | Portfolio at Age 72 |

|---|---|---|

| Conservative | 5% | ~$383,000 |

| Historical average | 7% | ~$421,000 |

| Strong market | 9% | ~$462,000 |

Even in a conservative scenario, your portfolio grows by $83,000 without you adding a dime. That $10,000-a-year part-time gig doesn't just cover groceries. It buys your portfolio five years of uninterrupted growth during the most dangerous period of your retirement.

Over five years, you'll earn $50,000 from part-time work. But the real payoff? The $83,000 to $162,000 your portfolio gains because you never had to touch it.

Almost nobody quantifies this effect when they write about $300,000 retirements. They really should.

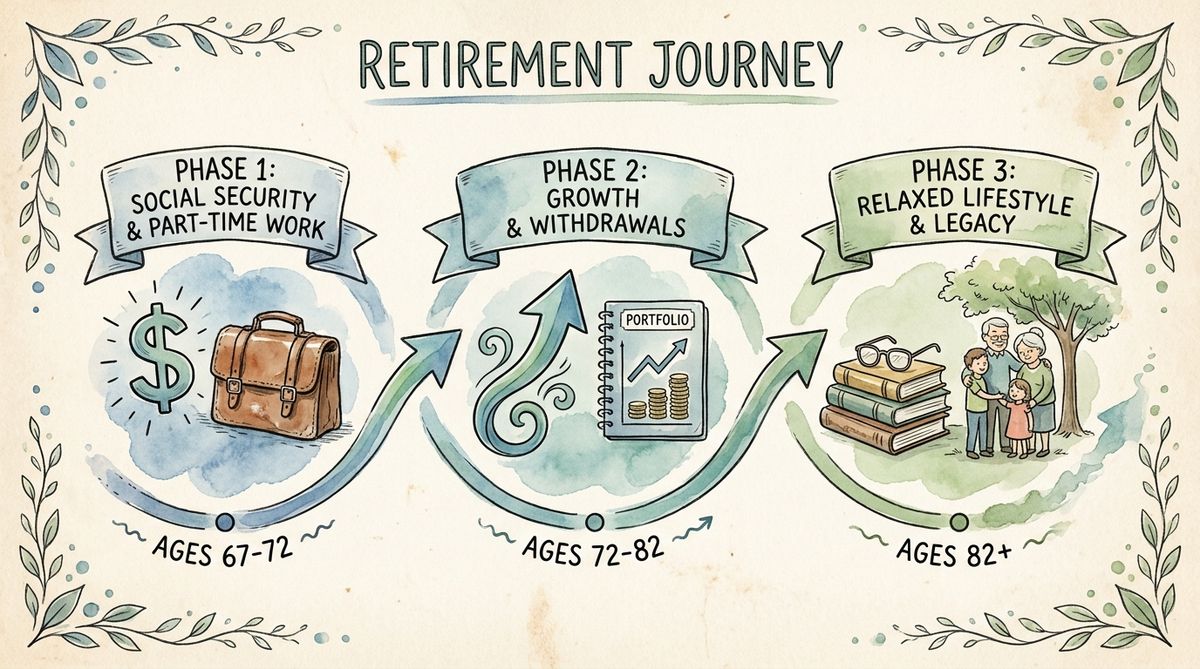

Three Phases of a $300K Retirement

Here's something I wish more people understood. Retirement isn't one long, unchanging stretch. It moves through distinct phases, and your strategy should shift with each one.

My buddy Carlos, who retired from teaching at 66, told me the best advice he got was to "think of retirement in chapters, not one big book." He was right.

Phase 1: The Growth Window (Ages 67 to 72)

This is your strongest period. Social Security plus part-time income covers your expenses. Your portfolio grows untouched. You're active, healthy, and earning.

Phase 1 Income (Ages 67-72)

- Social Security $4,000

- Part-time work $833

- Portfolio withdrawal $0

- Total Monthly $4,833

Annual Breakdown

- Social Security $48,000

- Part-time earnings $10,000

- Portfolio growth $83K-$162K

- Total Annual Income $58,000

Your only job during these five years (besides the actual part-time job) is to resist the temptation to dip into your portfolio. I know it's sitting right there. I know the new patio furniture looks great online. Leave it alone. Every dollar you leave invested is working for your future self.

Phase 2: The Sustainable Withdrawal Years (Ages 72 to 82)

The part-time job ends. But two things have changed in your favor.

First, your portfolio has grown to roughly $383,000 to $421,000. A 4% annual withdrawal from $400,000 gives you $16,000 a year, or about $1,333 per month.

Second, Social Security has been getting cost-of-living adjustments every single year. At an average COLA of 2.5%, your $48,000 annual benefit has grown to approximately $54,300 by age 72. By age 82, it could reach $69,000.

Income Actually Increases at 72

You're making more money at 72 than you were at 67 — roughly $70,300/year vs $58,000/year. Let that sink in for a second.

When Required Minimum Distributions kick in at 73, you'll need to withdraw about $15,100 per year from a $400,000 traditional IRA (based on the IRS Uniform Lifetime Table divisor of 26.5). That lines up almost perfectly with a 4% withdrawal rate. So the IRS mandate and the smart strategy happen to be the same number. I love when that works out.

Phase 3: The Slower Years (Ages 82 and Beyond)

Researchers describe retirement spending in three stages: go-go, slow-go, and no-go. I know those sound a little silly, but they're actually pretty useful.

By 82, most retirees have naturally slowed their spending. Travel winds down. The second car goes away. Saturday nights shift from restaurants to time with the grandkids. And honestly? Most people I've talked to say they're happier in this phase than they expected.

Social Security, now approaching $69,000 or more annually with compounded COLAs, covers a larger share of your reduced expenses. Your portfolio, even after a decade of withdrawals, likely holds $200,000 to $350,000 depending on market conditions and how closely you stuck to a 4% withdrawal rate.

The One Real Risk

The genuine wildcard is healthcare, specifically long-term care. Medicare doesn't cover custodial long-term care, and costs can run $60,000-$120,000/year. Consider long-term care insurance while you're still in your 60s when premiums are manageable.

The Tax Surprise Nobody Mentions

Here's something the "$1.46 million or bust" crowd doesn't realize: at $300,000, the tax code is actually on your side.

I was having coffee with my friend Lisa, who's a CPA in Charlotte, and she put it this way: "The tax code doesn't punish modest retirees. It practically rolls out a red carpet for them." She wasn't kidding.

For 2026, a married couple filing jointly where both spouses are 65 or older gets:

- Standard deduction: $32,200

- Additional senior deduction (both 65+): $3,300 ($1,650 per spouse)

- New "One Big Beautiful Bill" senior deduction (both 65+): $12,000 ($6,000 per spouse, for joint MAGI under $150,000)

- Total deductions: approximately $47,500

Your Federal Tax Bill: $0

During Phase 1 and most of Phase 2, your federal tax bill will likely be $0. Compare that to someone withdrawing $80,000/year from a million-dollar portfolio — they're paying real taxes while you keep every dollar.

During Phase 1, your total income is around $58,000. Only a small fraction of your Social Security is even taxable at this income level (based on "provisional income" rules), so your adjusted gross income lands well below $47,500 in deductions. Your federal tax bill? Almost certainly $0.

Now compare that to someone withdrawing $80,000 a year from a million-dollar portfolio. They're paying real taxes. You're paying almost nothing. The percentage of your income that actually reaches your pocket is significantly higher than someone with four times your savings.

That's the part nobody puts in the headlines.

What Could Go Wrong (And Why You'll Probably Be Fine)

A good plan doesn't just hope for the best. It looks at the worst and says, "Yeah, I can handle that too." So let's stress-test this.

The market crashes 30% in Year 1. Your $300,000 drops to $210,000. That's painful to watch. But here's the thing: your Social Security and part-time income cover all your expenses. You don't sell a single share. Markets have historically recovered within 3 to 5 years. By age 72, your portfolio is back to $275,000 to $290,000. Not as strong as the base case, but absolutely workable. The part-time income is the hero of this scenario.

A $30,000 medical emergency hits at age 70. Your portfolio drops from $380,000 to $350,000. That's still above your starting balance. The buffer you built during the growth window absorbs the hit. That's exactly what buffers are for.

Social Security gets cut. The Social Security trust fund faces potential depletion around 2032 to 2033, according to the latest projections from the CBO and SSA Trustees. Even in the worst-case scenario of an automatic 23% across-the-board cut, your combined benefit drops from $4,000 to roughly $3,080 per month. That's tighter, no question. But combined with portfolio withdrawals, it's still manageable. And let's be honest: Congress has enormous political incentives to prevent that cut from ever happening. Tens of millions of voters tend to notice when their checks shrink.

🎯 Five Moves to Make Your $300K Bulletproof

- Set up the bucket system: Divide your portfolio into cash (1-2 years expenses), bonds (years 3-7), and stocks (year 8+). Never sell stocks during a downturn.

- Use the Roth conversion window: During Phase 1, your taxable income is essentially zero. Convert chunks of traditional IRA to Roth, filling up the 10% and 12% tax brackets.

- Consider geographic arbitrage: States like Wyoming (no income tax), South Carolina, and North Carolina (exempt Social Security) can stretch your dollars further.

- Apply guardrails to withdrawals: Start at 4-5%, but if portfolio drops 20%, cut withdrawals 10%. If it grows 20%, give yourself a 10% raise.

- Skip the annuity: With $300K, you need growth, liquidity, and inflation protection. Your 70/30 portfolio provides all three. Annuities provide none.

The Bottom Line

You don't need $1.46 million. You need a plan that fits your actual numbers.

A couple retiring at 67 with $300,000 in savings, $4,000 per month in Social Security, and five years of modest part-time income has a projected total income of roughly $70,000 per year by age 72, pays almost nothing in federal taxes, and can sustain that income for 25 to 30 years with a well-managed portfolio.

That's not scraping by. That's a comfortable, sustainable retirement built on math instead of fear.

Your next step is straightforward. Sit down this weekend, maybe with a cup of coffee and some quiet, and map your actual monthly expenses. If they come in under $5,000 a month, you're not just okay. You're ahead of schedule.

And that feels pretty good.

Ready to Plan Your Retirement?

Want to run the numbers for your specific situation? Our retirement calculator lets you model different scenarios with your actual savings, Social Security estimates, and expenses. It's free, no email required.

Thanks for reading if you've made it this far. Peace!

This article is for informational purposes only and does not constitute financial advice. Tax laws and benefit amounts change annually. Consider consulting a fee-only financial advisor to review your specific situation.