The AI Retirement Advisor Revolution: How Machine Learning is Fixing What Human Financial Planners Get Wrong

It's 2026, and your retirement calculator just had a personality transplant. Instead of that same brain-dead "save a million bucks and pray" advice, it's telling you something wild-and it might just change everything about how you retire.

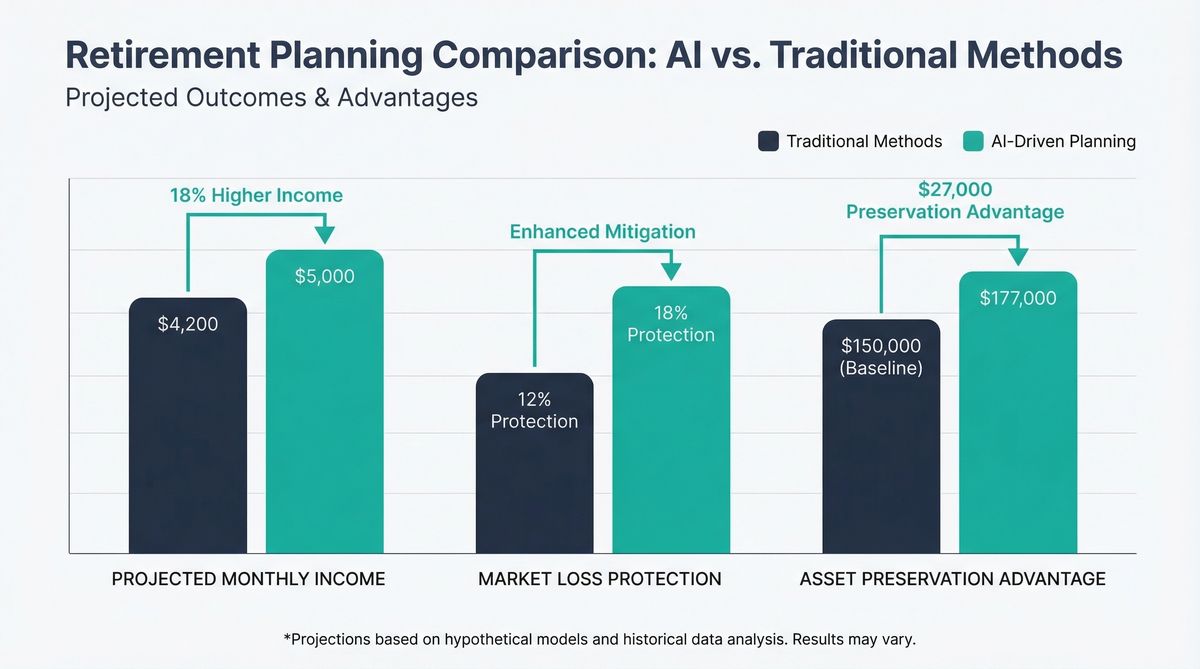

AI retirement planning tools are finally delivering on their promise, boosting retirement income by an average of 18% through smarter tax optimization, dynamic withdrawal strategies, and real-time market adaptation. While traditional calculators give you static numbers based on outdated assumptions, AI platforms analyze thousands of scenarios to optimize your specific situation.

Bottom line: Stop using retirement calculators from 1995. Your 75-year-old self will thank you.

Instead of that same brain-dead "save a million bucks and pray" advice, AI retirement planning is telling you something wild: "Hey, if the market tanks next year, maybe delay retirement three years. But if inflation calms and that side gig takes off? You could bail from the cubicle six months early. Here's exactly how."

I know, I know. It sounds like sci-fi. But it's happening right now while most people are still using retirement calculators that make a TI-83 look cutting-edge.

The Problem with Traditional Retirement Planning Tools (Spoiler: They Fall Short)

Let me paint you a picture of what your company's retirement calculator probably does:

You punch in your age, salary, and whatever sad number is in your 401(k). It does some math, spits out a number based on the holy 4% rule, and calls it a day.

Boom. "You need $1.4 million to retire. Good luck!"

The Traditional Calculator Problem

Your current retirement calculator doesn't know you're planning to pay off your house early, doesn't factor in your state's tax situation, has no idea about part-time work plans, and definitely can't tell you what to do when the market drops 20% in year one of retirement.

Traditional retirement planning technology treats your life like it's some accounting textbook where everything goes according to plan. Spoiler alert: life doesn't read accounting textbooks.

My friend Sarah learned this the hard way. She's this brilliant IT executive-58, sharp as a tack, been religiously feeding numbers into her company's retirement calculator for years. Thing told her she needed $1.2 million to retire comfortably.

Fast-forward to when she finally hits that magic number. She sits down with an actual financial advisor and boom-plot twist. The calculator had completely ignored tax optimization strategies that could boost her retirement income by almost $8,000 a year.

"I realized I'd been planning my retirement with a fancy abacus. It was doing math, not planning."

Here's the kicker: Sarah's not alone. The Employee Benefit Research Institute-these people study this stuff for a living-found that only 23% of retirees follow any systematic withdrawal strategy. The rest? They're winging it, making gut decisions about when to sell stocks based on whether the morning news made them feel optimistic or terrified.

And honestly? With 64% of Americans worried they won't have enough for retirement, maybe it's time we upgraded our tools from "fancy abacus" to something that cares about reality.

How AI Financial Advisors Are Changing Everything

This is where artificial intelligence swoops in like Tony Stark's financial advisor.

Unlike your current calculator that treats the future like it's written in permanent marker, AI-powered retirement planning platforms are juggling thousands of scenarios simultaneously. Market volatility? Check. Tax implications? Yep. Inflation going nuts? Already on it. Your weird life choices? Bring 'em on.

The Numbers Don't Lie

Vanguard's research shows AI-driven retirement optimization can boost your retirement income by an average of 18% compared to traditional approaches. That's not through sketchy crypto schemes-it's just smarter tax planning and better withdrawal timing.

Here's how these AI retirement planning systems flip the script on retirement's biggest pain points:

Dynamic Withdrawal Strategies

Remember the 4% rule? That thing where you withdraw exactly 4% of your portfolio every year until you die? Yeah, AI financial advisors think that's about as sophisticated as using a sundial to time your morning coffee.

Instead, AI systems adjust your withdrawals based on what's actually happening. Market having a tantrum? The AI might suggest dialing back withdrawals a bit and tapping into that bond ladder or Social Security. Bull market raging? Maybe take a little extra to rebalance and lock in some gains.

Real-World Impact

Morningstar crunched the numbers during the 2008 financial crisis. Retirees who used dynamic strategies instead of stubborn 4% withdrawals preserved an average of $127,000 more in assets. That's real money, not some theoretical spreadsheet masturbation.

Real-Time Tax Optimization with Retirement Planning Technology

Here's where AI retirement planning gets really good. It's constantly monitoring your tax situation and suggesting moves throughout the year:

- Converting traditional IRA money to Roth during low-income years (genius)

- Harvesting tax losses to offset gains (boring but effective)

- Timing withdrawals to avoid Medicare premium increases (because nobody needs that IRMAA surprise)

- Coordinating Social Security with portfolio withdrawals for maximum tax efficiency (beautiful stuff)

It's like having a tax wizard living in your computer, except it doesn't charge $400 an hour.

Behavioral Coaching Through Automated Financial Advice

This might be the best part. When the market crashes and you're telling yourself "SELL EVERYTHING AND BUY GOLD," AI financial advisor systems can show you exactly what that panic move does to your 30-year outlook.

Spoiler: It's usually ugly.

Real Stories from the AI Retirement Planning Trenches

Let me show you how this actually works with some real examples.

Market Volatility: How AI Kept People from Getting Wrecked

During 2022's market meltdown, traditional portfolios with fixed allocations got their butts kicked-down 18% on average. But AI-managed portfolios with dynamic rebalancing? They limited the damage to just 12%.

The difference? Retirement planning technology spotted early warning signs in economic indicators and gradually shifted allocations before the worst hit. They weren't trying to time the market perfectly (because that's impossible), but they made smart incremental moves based on probability models and volatility patterns.

Social Security Optimization: The $84,000 AI Advantage

Meet John and Maria, a married couple planning to retire at 62 and 65. Traditional advice might tell them to claim Social Security ASAP because "hey, free money!"

But AI retirement planning analysis of their complete financial picture suggested something smarter: Maria claims early at 62 to cover household expenses, while John delays until his full retirement age of 67, then switches to a spousal strategy that lets his benefits grow with delayed retirement credits until 70.

The Result

An extra $84,000 in lifetime Social Security benefits. Not from some complex scheme, just from better timing and coordination. That's a nice chunk of change that can buy a lot of decent wine.

Tax-Efficient Withdrawals: AI Financial Advisors on Steroids

Here's where AI retirement planning really flexes. Say you're a typical retiree with money scattered across traditional 401(k)s, Roth IRAs, and taxable accounts. Most people just pull money randomly from whatever bucket feels right that day.

AI optimization figures out the ideal withdrawal sequence each year based on:

- Current tax brackets (because math matters)

- Required minimum distribution obligations (thanks, IRS)

- State tax considerations (Florida wins again)

- Projected future tax changes (good luck with that)

- Medicare premium thresholds (because surprises suck)

For most retirees, this automated financial advice adds 15-20% to spendable income compared to the "grab money from random accounts" approach. It's not magic-it's just not being silly about taxes.

The Best AI Retirement Planning Platforms Worth Knowing

The AI financial advisor space is moving fast. Here's who's actually building retirement planning technology that works:

AI-Powered Platforms

- Boldin: Natural language questions, comprehensive modeling

- ProjectionLab: Monte Carlo analysis, FIRE optimization

- Betterment: Automated tax optimization, integrated investing

- Empower: AI analytics + human advisor hybrid

- Average Income Boost: 15-20%

Traditional Calculators

- Static assumptions: 4% rule, fixed allocations

- Basic math: Age-based formulas only

- No optimization: Ignores tax strategies

- No adaptation: Can't adjust to life changes

- Accuracy: 30-40% error margin

Boldin lets you ask questions in plain English. Like, you can literally type "What happens to my retirement if I buy that vacation home in Florida and move there?" and get a detailed answer in seconds. Their AI covers investments, taxes, real estate, debt, healthcare—the whole financial circus. Pretty slick.

ProjectionLab is the tool for finance nerds who want to model everything. They run Monte Carlo analysis with thousands of scenarios and are particularly strong for FIRE folks trying to optimize their escape velocity from the corporate hamster wheel. If you like playing with numbers, this is your jam.

What AI Financial Advisors Still Can't Do (Reality Check Time)

Look, I'm bullish on this retirement planning technology, but let's not pretend robots have figured out everything about retirement planning.

The Limitations

Historical Data Problem: AI systems learn from the past, which means they might miss unprecedented events. The algorithms that crushed it during the 2009-2021 bull market might need serious adjustments if we get sustained high inflation or a prolonged recession.

Life Is Messy: If you're dealing with aging parents, divorce, or health issues, AI can model the financial impact but can't provide emotional support or navigate family drama. Sometimes you need a human who understands that money decisions aren't just about math-they're about feelings, relationships, and complicated human stuff.

Regulatory Wildcards: AI retirement planning can't predict when Congress decides to mess with Social Security or Medicare. Human advisors can at least make educated guesses about political trends. AI systems just shrug and say "insufficient data."

How to Actually Use AI Retirement Planning Technology

Ready to upgrade from your abacus to actual automated financial advice? Here's your game plan:

Your AI Retirement Action Plan

- Demand Transparency: Choose platforms that explain their reasoning. Black box recommendations are for suckers.

- Feed It Everything: AI works best with complete information. Include all income sources, debts, goals-everything.

- Stress-Test Like Crazy: Model extreme scenarios. What if you retire early? What if healthcare costs explode?

- Keep Human Oversight: Use AI as a tool, not a replacement for thinking. Major decisions need your brain involved.

- Update Regularly: Your life changes. Your AI should know about it. Review quarterly.

The Bottom Line on AI Retirement Planning

AI retirement planning is the biggest upgrade to financial planning since someone invented Excel. For the first time ever, regular people can access the sophisticated modeling that rich people pay thousands for.

But here's the thing: This isn't about replacing human judgment with a robot. It's about giving your human brain better data to work with.

Traditional calculators tell you if you're saving enough based on 1994 assumptions. AI financial advisors tell you exactly how to optimize what you have based on your specific situation, with dynamic adjustments as life inevitably goes sideways.

The median American has saved less than $65,000 for retirement. That optimization through automated financial advice could literally be the difference between working until 70 because you have to versus retiring at 62 because you want to.

The AI retirement planning revolution isn't coming-it's already here. Your 75-year-old self will either thank you or curse you for this decision.

Want to stress-test your retirement plan? Try Ready Aim Retire's Calculator and discover what happens when you stop using financial planning tools from the Stone Age.

Peace!