Medicare Supplement Insurance: The Decision That'll Cost You $50K (Or Save You $50K)

When you turn 65, you get one six-month window to buy Medicare supplement insurance without health questions. Miss it, and you could face devastating out-of-pocket costs or be locked out forever. This is the decision that separates "ready" retirees from those who pay tens of thousands more.

If you don't have time to read the full article, here are the main takeaways:

- You have ONE chance: 6-month window starting when you turn 65 and enroll in Medicare Part B

- Original Medicare has NO out-of-pocket maximum — 20% coinsurance can mean $100K+ bills

- Plan G is best for most people — comprehensive coverage for $140-$220/month

- Plan N saves money — $30-$60/month less with small copays

- Medicare Advantage vs. Medigap is a one-way door — choose carefully

Bottom line: Skipping this decision could cost you $40,000-$50,000 over the next decade. Don't be Barbara (you'll meet her below).

My buddy's mom — let's call her Barbara — turned 65 last spring. She signed up for Medicare Parts A and B like you do. But Barbara's one of those people who hasn't seen the inside of a hospital since Reagan was president, so when her insurance broker said "hey, you should grab a Medigap policy," she waved him off. "Why am I paying $180 a month for something I'll never use?"

Eleven months later she needed a hip replacement. Then the first surgery got infected and she needed another one. Out-of-pocket under Original Medicare? Over fourteen grand. In one year.

She tried to buy a Medigap plan after all that. Two companies said no. A third said sure — $470 a month with a surcharge baked in forever. Forever.

Barbara's window had closed. That one non-decision is gonna cost her somewhere between $40,000 and $50,000 over the next decade compared to what she would've paid if she'd just signed up when she had the chance.

I tell you this not to scare you. I tell you because almost nobody talks about this medicare supplement decision with the urgency it deserves. People spend more time picking a mattress than they do on this, and it's legitimately one of the biggest money decisions you'll make at 65.

Why Your Medicare Supplement Decision Can't Wait

Here's the thing about Medicare that blindsides people: Original Medicare has no out-of-pocket maximum.

None. Zero. Nada.

You get hit with cancer, a major surgery, some extended hospital stay — there's no cap on what you owe. Medicare Part A covers hospital stays after a $1,736 deductible per benefit period (and yeah, you can rack up multiple benefit periods in one year). Part B covers 80% of outpatient stuff after a $283 annual deductible.

You cover the other 20%.

And 20% of a $500,000 cancer treatment is a hundred grand. Let that sit for a second.

That's what Medigap — medicare supplement insurance — exists for. It fills the gaps Original Medicare leaves wide open.

But here's where it gets real.

You Get One Shot

A six-month Medigap Open Enrollment window. Starts the month you turn 65 and are enrolled in Part B. During those six months, insurance companies have to sell you a policy at their standard rate. They can't ask about your health. Can't charge extra. Can't turn you down.

Once that window closes? Whole different ballgame. They'll scrutinize every detail of your health. Every pill you take, every diagnosis, every procedure. If anything meaningful has changed since you turned 65, you're looking at massive surcharges or a straight-up denial.

There are some exceptions. If your Medicare Advantage plan bounces from your area, you might get another shot. A handful of states — Connecticut, Massachusetts, Maine, New York — offer protections no matter when you apply. But for everybody else in the other 46 states? That six-month window is pretty much it.

I'm not trying to be dramatic. This is just how the program works. And it's important to be start about it.

Medigap Plans Comparison: What Each Plan Actually Covers

One thing I actually like about medicare supplement insurance: the plans are standardized by the feds. A Plan G from Blue Cross covers the exact same stuff as a Plan G from Mutual of Omaha or AARP/UnitedHealthcare. Same benefits, different price tags.

There are ten plan types with letters (A, B, C, D, F, G, K, L, M, N). Plans C and F are dead to anyone who became Medicare-eligible after January 1, 2020, so we can skip those.

State Exceptions

If you're in Massachusetts, Minnesota, or Wisconsin, your state does its own thing with plan structures. Hit up your State Health Insurance Assistance Program (SHIP) for the specifics.

For everyone making this call in 2026, it really comes down to three options. Here's how they stack up in our medigap plans comparison:

Plan G — The Best Medigap Plan for Most People in 2026

Plan G covers basically everything Original Medicare doesn't, except the $283 Part B annual deductible. That's it. You pay $283 a year and Plan G handles the rest — hospital deductibles, coinsurance, skilled nursing, excess charges, even emergency care when you're traveling abroad (which, as someone who's spent years bouncing between countries, I appreciate).

Premiums run roughly $140 to $220 a month depending on where you live, how old you are, which company you go with. Some areas cheaper, some more expensive. You know how it goes.

Plan N — The "I Want Protection But I Also Like Saving Money" Option

Plan N covers most of what G does, but you'll pay up to $20 for some office visits, up to $50 for ER visits that don't lead to an admission, and it doesn't cover Part B excess charges.

The excess charges thing sounds scarier than it is. Most Medicare providers accept "assignment" — meaning they charge the Medicare-approved amount and that's that. A bunch of states ban excess charges entirely.

Premiums: roughly $110 to $170 a month. So you're saving $30 to $60 compared to Plan G.

Plan A — The Bare Bones

Plan A is the cheapest option and it shows. Covers Part A coinsurance, some extra hospital days, Part B coinsurance, blood. But it does not cover the Part A deductible ($1,736 in 2026), skilled nursing coinsurance, or foreign travel emergency care.

One hospital stay and you're eating that full $1,736 deductible yourself. Personally, that makes me twitchy, but everybody's got a different risk tolerance.

Plan G

- Part A deductible ($1,736) ✓ Covered

- Part B deductible ($283) ✗ You pay

- Part B coinsurance (20%) ✓ Covered

- Part B excess charges ✓ Covered

- Office visit copays ✓ None

- ER copay (no admission) ✓ None

- Monthly premium $140–$220

Plan N

- Part A deductible ($1,736) ✓ Covered

- Part B deductible ($283) ✗ You pay

- Part B coinsurance (20%) ✓ Covered

- Part B excess charges ✗ You pay

- Office visit copays Up to $20

- ER copay (no admission) Up to $50

- Monthly premium $110–$170

Let's Do The Actual Math

Most articles on this get hand-wavy right about here. I'd rather just show you the numbers.

Scenario 1: Helen — Healthy, Low Usage

Helen's 67, takes one generic med, sees her doctor twice a year. Under Original Medicare alone, she's spending maybe $2,000–$3,000 a year.

With Plan G at $180/month, she's paying $2,160 in premiums plus the $283 deductible. Call it $2,443.

Without Medigap, she might spend $1,500–$2,500 in a good year.

So yeah, in a healthy year, Helen's "overpaying" by maybe $500 to $900. But what she's buying is the thing money literally cannot buy later — guaranteed protection at a locked-in rate, no medical questions asked. That peace of mind has a value. You just can't put it on a spreadsheet.

Scenario 2: Steve — Needs Knee Surgery

Steve's got Plan G and needs a knee replacement. Total Medicare-approved charges: $55,000. Medicare pays its chunk, leaving about $11,000 in Part B coinsurance plus the $1,736 Part A hospital deductible.

Without Medigap? Steve owes roughly $12,700. With Plan G? He pays his $283 Part B deductible and his monthly premiums. Done.

Plan G saves Steve over ten grand in a single year. That's not hypothetical. That's just math.

Scenario 3: Carol — Multiple Chronic Conditions

Carol's dealing with diabetes, high blood pressure, early-stage kidney disease. Multiple specialists, regular labs, five medications. Her annual Medicare coinsurance and deductibles without supplemental coverage: $6,000 to $8,000 a year.

With Plan G at $195/month ($2,340/year) plus the $283 deductible, Carol's total is about $2,623. Without it, she's spending $6,000 to $8,000.

Plan G saves Carol $3,400 to $5,400 every single year. Over ten years that's $34,000 to $54,000. And that's before she ends up in the hospital for anything.

Those are the kinds of numbers that make the medicare supplement decision pretty obvious for a lot of people. But I get it — not everyone's Carol.

What Medicare Supplement Insurance Doesn't Cover

Before we go any further, there's a big gap in Medigap itself: no prescription drug coverage. You need a separate Part D plan for that, usually $30–$50 a month in premiums. Good news though — thanks to the Inflation Reduction Act, Part D now caps your out-of-pocket drug costs at $2,000 a year. That's a solid win.

Medigap also doesn't touch dental, vision, or hearing. Medicare Advantage plans often bundle those in, which is why people get tempted. If you need that stuff, you'll have to buy separate coverage or pay out of pocket.

Medicare Advantage vs. Supplement Plans: The Fork in the Road

Alright, this is the big medicare advantage vs supplement question — and it's where people get confused. You can't have both. It's Medigap or Medicare Advantage. Pick one.

Medicare Advantage (Part C) comes from private insurers. Lots of plans have $0 or super low premiums. Many include drugs, dental, vision, hearing — all the stuff Original Medicare ignores. On paper it looks like a no-brainer.

But — and this is a big but — Advantage works like an HMO or PPO. Network restrictions. Referrals for specialists. And while Advantage plans do have an out-of-pocket max (up to $9,250 for in-network in 2026), you're paying copays and coinsurance at every turn.

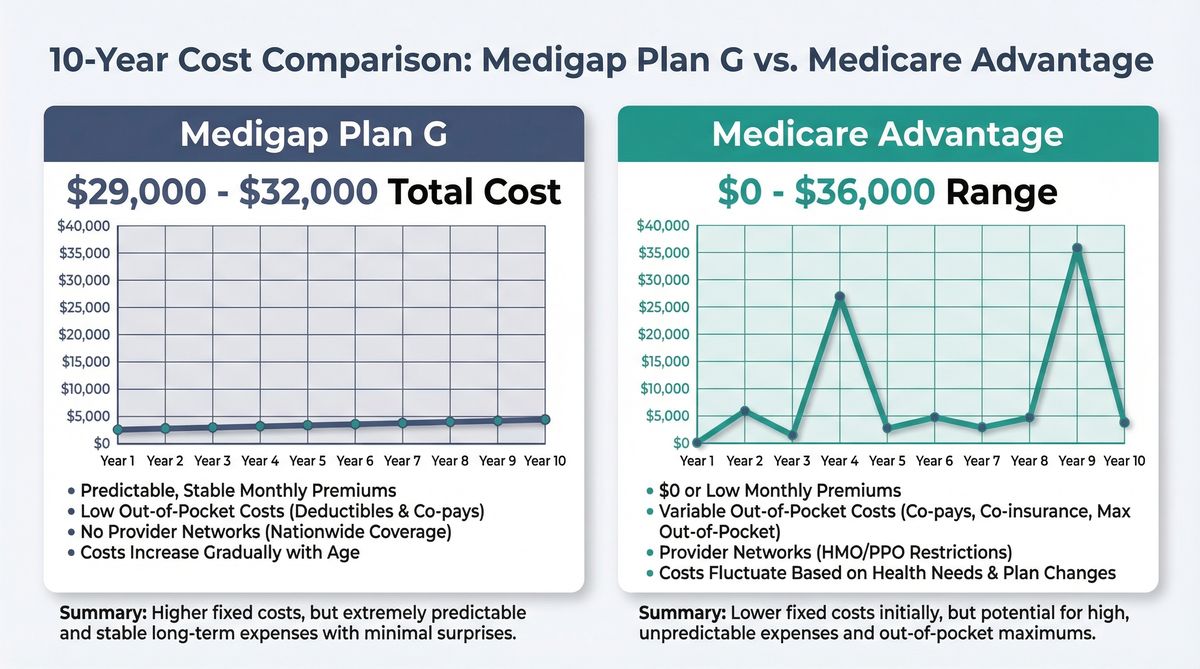

Here's the ten-year math for a moderately healthy person:

Medigap Plan G Route

- Medigap premiums ~$21,600

- Part B deductible (10 years) ~$2,830

- Part D drug plan ~$4,800

- Extra costs Minimal

- Ten-year total ~$29,000–$32,000

Medicare Advantage Route

- MA premiums $0–$6,000

- Copays, coinsurance, deductibles $20,000–$50,000

- Network restrictions Risk factor

- Coverage changes annually Risk factor

- Ten-year total ~$20,000–$56,000

Look at that range on Advantage. $20K to $56K. That's not a plan — that's a coin flip. Stay healthy, stay in-network, and Advantage wins on cost. Get seriously sick or need an out-of-network specialist? Costs blow right past Medigap.

And here's the part that keeps me up at night on behalf of people making this choice: switching from Medicare Advantage back to Medigap is brutally hard.

If you've been on Advantage for more than 12 months and want to go back to Original Medicare with a Medigap supplement, you're facing full medical underwriting. And if your health has gotten worse during those years on Advantage — which, I mean, you're aging, so odds are decent — you might not qualify at all.

Think about what that means. Choose Medigap at 65, and you can always switch to Advantage later if you want. Choose Advantage at 65, and you might never be able to get Medigap.

That's a one-way door, and most people don't realize they're walking through it.

How To Choose the Best Medigap Plan in 2026

I'm not gonna tell you what to pick. I've seen too many "Top 10 Best Medicare Plans!" articles that pretend there's one right answer. There isn't. But I can tell you how to think about it.

Go with Medigap Plan G if:

- You like knowing exactly what you'll pay, no surprises

- You want to see any doctor who takes Medicare, anywhere in the country

- You've got chronic stuff going on or your family history makes you nervous

- You travel a lot or split time between states (snowbirds, I'm talking to you)

- You can handle $140–$220 a month without sweating it

- Sleeping well at night is worth more to you than saving fifty bucks a month

Go with Medigap Plan N if:

- You want solid protection but don't mind small copays here and there

- Excess charges aren't a thing where you live

- You'd rather pocket the $30–$60 monthly savings vs. Plan G

- Your state bans excess charges anyway (CT, MA, MN, NY, OH, PA, RI, VT)

Think about Medicare Advantage if:

- Budget is tight and you need rock-bottom premiums

- Having dental, vision, and hearing in one plan matters to you

- You're cool with network restrictions and asking for referrals

- You're healthy and you're okay rolling the dice on cost variability

- You genuinely understand how hard it is to switch back to Medigap later

Pro Tip

Oh, and one thing people forget: you and your spouse don't have to make the same choice. If one of you has health issues and the other's running marathons, different coverage might make more sense. I've seen couples where one person's on Plan G and the other's on Medicare Advantage. That's not indecisive — that's smart.

Timing Details That Can Make or Break Your Medicare Supplement Decision

A few timing details that can make or break this whole thing:

Still working at 65? If you've got employer coverage, you can delay Medicare Part B without a penalty. And here's the good part — your Medigap window doesn't start when you turn 65. It starts when you actually enroll in Part B. So if you work till 68 and then sign up for Part B, boom, your six-month window opens at 68. That's actually great news.

Retiring before 65? You'll need to bridge the gap with COBRA, an ACA marketplace plan, or your spouse's coverage until Medicare kicks in. The Medigap clock doesn't start early, no matter how much you want it to.

Already missed your window? You still have some options, but they're limited. Some states have annual enrollment periods. Some insurers do a "birthday rule" thing where you can switch Medigap plans around your birthday without underwriting. And if you lose coverage for specific reasons — like your Advantage plan pulls out of your area — you might get a guaranteed-issue right to buy certain Medigap plans.

Those backup options are narrow. The original six-month window is the one that matters.

What This Really Comes Down To

Strip away all the plan letters and premium math and this decision is actually pretty simple: what kind of risk are you cool with carrying in retirement?

Medigap is paying a known amount every month to make healthcare costs basically disappear as a financial worry. Medicare Advantage is betting that you'll stay healthy enough for the lower premiums to be worth the cost variability.

Neither one is wrong. Seriously.

But making no choice — just letting that six-month window close while you "think about it" — that's almost always a mistake. Barbara can tell you all about that.

Your Next Steps

- Mark your calendar: Your Medigap window opens the first day of the month you turn 65 and are enrolled in Part B. Six months. Set multiple reminders.

- Talk to independent brokers: Not just one company's agent who's gonna push their own plans. Get quotes from at least three carriers.

- Compare Plan G and Plan N: Run the numbers with your actual expected healthcare costs and risk tolerance.

- Research Medicare Advantage options: Check what's available in your zip code, but understand the trade-offs and one-way door risk.

- Get comprehensive retirement planning help: This Medicare decision affects taxes, withdrawals, Social Security timing — everything needs to fit together.

If you want help figuring out how all of this fits into the bigger retirement picture — the taxes, the withdrawals, the Social Security timing, all of it — that's exactly what we do over at Ready Aim Retire. We're not selling insurance. We just want to make sure the pieces actually fit together.

Because a $180/month decision right now could save you $50,000 over the next decade. Or cost you that much.

Don't be Barbara.

You're doing great! ✌️