The FIRE Community's Biggest Fear in 2026: What Happens When High-Income Tech Jobs Disappear?

My friend Sarah thought she had cracked the code for FIRE job security. Thirty-two years old, pulling down $180K, living in Austin, saving like a maniac. Then November 2023 happened, and she became one of 21,000 employees cut in Meta's massive layoff wave. Eight months later, she finally landed another gig—at 20% less pay.

If you don't have time to read the full article, here are the main takeaways:

- Tech layoffs have eliminated 150,000+ high-paying jobs since 2022, breaking traditional FIRE math

- New emergency fund minimum: 12-18 months of expenses for volatile careers

- Income diversification is now mandatory, not optional

- The "barbell strategy" maximizes savings during high-income periods while building backup plans

Action: Build recession-proof FIRE strategies before you need them.

"Ross," she told me over breakfast, "I thought I was being conservative. Turns out I was just being naive about FIRE job security."

Sarah's not alone. She's become the poster child for what I'm calling the Great FIRE Reality Check of 2026.

The Golden Goose Just Got Cooked: Why Tech Job Market FIRE Is Failing

Here's the thing about the FIRE movement that nobody wants to admit: it was built on quicksand.

For the past decade, FIRE worked because tech jobs were everywhere and they paid incredibly well. Google, Meta, Amazon—they were basically printing money and handing it out to anyone who could code. We all pretended this was normal.

It wasn't normal. It was a bubble.

The Numbers Don't Lie

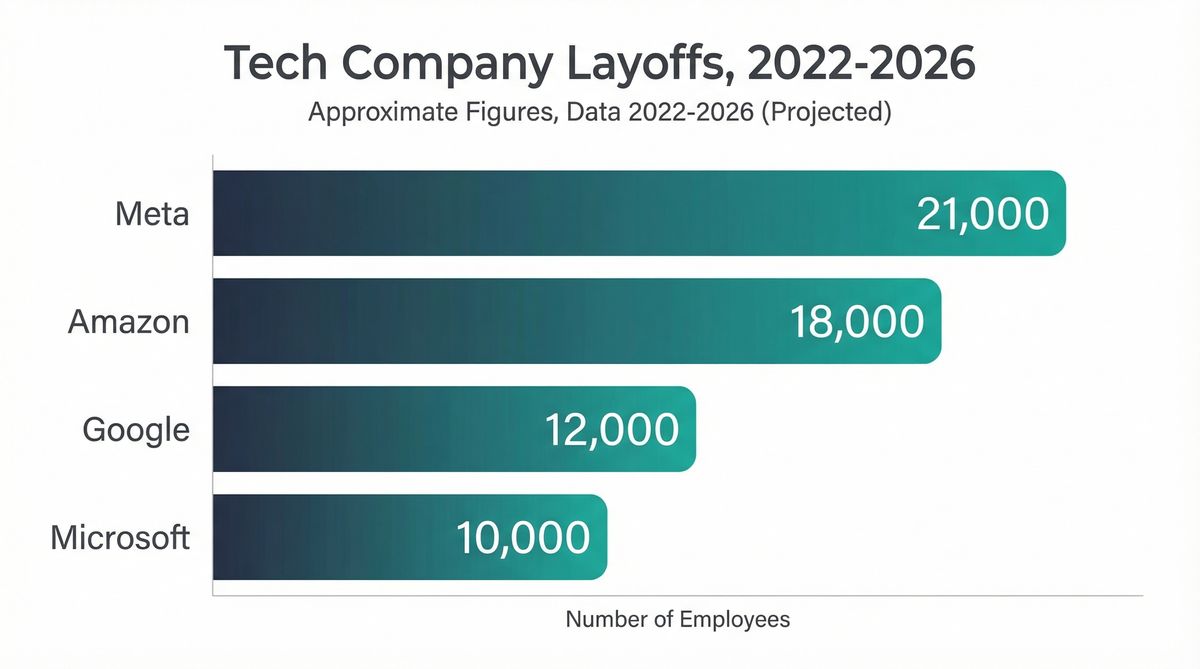

Since 2022, big tech has cut over 150,000 jobs. Meta: 21,000 people. Amazon: 18,000. Google: 12,000. Microsoft: 10,000. These aren't startups failing—these are the companies that funded thousands of FIRE dreams.

The math was simple: get hired at XYZ Tech Company, live below your means, save 50% of your income, retire at 45. Boom.

Except the first step—getting hired at XYZ Tech Company—just became a lot harder. And staying hired? Even harder.

What the Hell Happened to FIRE Job Security?

Three things broke the traditional tech job market FIRE formula, and they all happened at once.

Interest Rates Killed the Party

When the Fed started hiking rates, tech stock prices went from "to the moon" to "what goes up must come down." Suddenly, companies that were hiring like drunk sailors had to show actual profits. Wild concept, I know.

AI Started Eating Jobs (The Good Ones)

Here's what's messed up: AI isn't coming for the minimum wage jobs. It's coming for the $200K product manager roles and the $150K program coordinator positions. You know, the exact jobs that funded most FIRE journeys.

My buddy Dave was making $220K as a program manager at a major tech company. His entire department got "reorganized" (corporate speak for "replaced by ChatGPT"). He's now freelancing and making about 60% of what he used to make.

Remote Work Killed Geography Arbitrage

Remember when you could get Silicon Valley money while living in Kansas? Yeah, that's done. Why pay a San Francisco salary when you can hire someone just as good from Poland for half the price?

The arbitrage game changed overnight.

The New Reality of Layoffs Retirement Planning

I've been talking to people in the FIRE community who got steamrolled by these changes. Their stories reveal why traditional layoffs retirement planning falls short.

Before the Reality Check

- Lisa & Tom's Combined Income $350K

- Expected FIRE Date 2034

- Confidence Level Very High

After the Layoffs Hit

- New Combined Income $180K

- New FIRE Date 2041

- Timeline Extension +7 Years

"We went from feeling ahead of the game to feeling like we were starting over," Lisa told me. "And the worst part? We did everything 'right' according to every FIRE blog we'd ever read."

That's the problem with the old FIRE playbook—it assumed your income was a given. It's not.

Building Recession Proof Financial Independence: The New Playbook

But here's the weird thing: some people are thriving in this chaos by focusing on recession proof financial independence strategies.

Marcus used to be a senior engineer. When the layoffs hit his team, he was ready. Not because he saw it coming, but because he'd accidentally built what I call "anti-fragile FIRE."

While still employed, he'd started consulting on weekends. Built a couple of small software products that brought in a few grand a month. Nothing crazy, but enough to matter.

When he was shown the door, his side income covered 70% of his living expenses immediately.

"Ross, getting fired was the best thing that ever happened to my FIRE plan. I realized I wasn't building financial independence—I was building really expensive dependence on my employer."

Smart. That's the foundation of true recession proof financial independence.

Emergency Funds for FIRE Job Security in 2026

Forget everything you've heard about emergency funds when it comes to FIRE job security.

Three months of expenses? That's cute. Six months? Better, but still not enough for proper layoffs retirement planning.

Sarah was unemployed for eight months. Eight months. Her old emergency fund would've lasted three.

New Emergency Fund Rules

The new minimum for anyone pursuing FIRE job security in a volatile career: Twelve to eighteen months of expenses in cash. I can hear the FIRE purists screaming about opportunity cost, but consider the alternative: liquidating investments during a bear market because you lost your job.

Look, I get it. Sitting on 18 months of expenses feels like parking money in a savings account while inflation eats it up. But consider the alternative: having to liquidate investments during a bear market because you lost your job.

That's not opportunity cost. That's financial suicide.

Skills That Support Recession Proof Financial Independence

Here's what I've learned watching people navigate this mess: some skills survive everything and are essential for building recession proof financial independence.

Sales and Relationships

AI can write code, but it can't take clients to dinner and make them feel good about spending money.

Creative Problem Solving

The ability to look at a weird situation and figure out something that's never been tried before.

Physical World Skills

Plumbers, electricians, nurses—AI can't unclog your toilet or stick an IV in your arm.

Working WITH AI Instead of Against It

The people thriving aren't the ones trying to compete with ChatGPT. They're the ones using it to do their jobs better and faster.

My friend Elena was a content marketer making $90K. Instead of panicking about AI writing tools, she learned to use them. Now she's freelancing, using AI to handle the grunt work, and charging clients for strategy and creativity. She's making $130K working for herself.

Same skills. Different application. That's recession proof financial independence in action.

The Barbell Approach to FIRE Job Security

The smartest FIRE people I know have adopted what I call the barbell strategy for maximum FIRE job security.

One end: aggressive saving when money is good. Instead of the standard 25-50% savings rate, they're pushing 60-70% when they can.

Other end: building recession proof financial independence backup plans. Multiple income streams. Location independence. Skills that travel.

My buddy James did this perfectly. Software engineer, living in a tiny apartment, banking almost 70% of his income. Seemed crazy at the time.

Then his company went through layoffs. But James had been freelance consulting on the side and had enough saved to take a year off if he wanted.

Instead, he moved to Mexico City, kept freelancing, and is now making more money than he did with about 1/3 the stress.

The barbell strategy recognizes something traditional FIRE advice doesn't: high incomes are temporary. Maximize them while you have them, but don't bet your entire future on them lasting.

What You Should Actually Do for FIRE Job Security

Alright, enough theory. Here's your playbook for building recession proof financial independence in an unstable world:

Get Real About Your Risk

How screwed would you be if your income disappeared tomorrow? Not just financially—emotionally, practically, all of it. If the answer is "very," you need to fix that before you worry about optimizing your portfolio allocation.

Build Real Insurance for FIRE Job Security

- Bump your emergency fund to 12-18 months for proper layoffs retirement planning. Yes, it sucks holding that much cash. Do it anyway.

- Develop at least one income stream that doesn't depend on your main job. Doesn't have to be huge, just consistent.

- Learn skills that complement AI rather than compete with it.

- Actually maintain your professional network. Not LinkedIn fake networking—real relationships.

Save Like the World Is Ending (When You Can)

If you're in a high-income role right now, consider this a temporary situation. Save aggressively while the money is flowing as part of your tech job market FIRE strategy.

Plan for Chaos in Your Layoffs Retirement Planning

Build FIRE scenarios that assume your career won't be linear. What happens if you're unemployed for a year? What if you have to take a 30% pay cut? What if you need to relocate?

Tools like the ones we built at Ready Aim Retire can help you model these scenarios for better FIRE job security planning.

The Upside of Modern Layoffs Retirement Planning

Here's something weird: almost everyone I know who's been through a major career setback says it made them better at building recession proof financial independence.

Not just more careful—better. More creative. More resilient. More realistic about risk.

Sarah, my friend from before? She's now making $145K at a smaller company, has three freelance clients, and feels more financially secure than she ever did making $180K at a big tech company.

"Getting laid off taught me that real FIRE job security isn't about hitting a number. It's about knowing you can handle whatever gets thrown at you."

That's a hell of a lot more valuable than any spreadsheet.

Build for Reality, Not Fantasy

The biggest mistake the FIRE community made was assuming the good times would roll forever in the tech job market FIRE world.

Tech salaries would only go up. Jobs would be plentiful. Geographic arbitrage would last indefinitely.

None of that was ever guaranteed.

The people who are still on track for FIRE in 2026 are the ones who built for volatility from the start. Multiple income sources. Longer emergency funds. Skills that transfer across industries. That's true recession proof financial independence.

They planned for the economy we actually have, not the one they wished we had.

That's not pessimism. That's just good layoffs retirement planning.

🎯 Your Action Plan: Building FIRE Job Security Today

- Assess your risk profile: How long would your emergency fund last? What happens if your income disappears?

- Extend your safety net: Build 12-18 months of expenses in easily accessible accounts.

- Diversify your income: Start one alternative income stream before you need it.

- Develop future-proof skills: Focus on areas that complement AI rather than compete with it.

- Model various scenarios: Use planning tools to see how career setbacks affect your FIRE timeline.

- Build real relationships: Your network is your safety net when algorithms fail.

The tech job market isn't getting more stable. AI isn't going to suddenly stop disrupting careers. The days of guaranteed high-income trajectories are over.

But that doesn't mean FIRE is impossible. It just means you need to get smarter about building recession proof financial independence.

Build multiple income streams. Save aggressively when you can. Develop skills that travel. Plan for setbacks as part of your layoffs retirement planning strategy.

And most importantly: stop assuming your current job will be there next year.

Because it might not be. And that's okay—if you're prepared for it with proper FIRE job security planning.

Cheers!

Want to stress-test your FIRE plan against job loss, pay cuts, and other career curveballs? Check out Ready Aim Retire's scenario planning tools. Because hope is not a strategy, but proper planning is.