The Widow's Financial Survival Guide: How to Secure Your Money When Everything Falls Apart

Your husband died on a Tuesday morning. By Thursday, you're staring at paperwork that might as well be written in ancient Greek, and some bureaucrat from Social Security is dropping deadlines on you like they're discussing the weather.

If you're dealing with a spouse's death, here are the critical deadlines and decisions you can't afford to miss:

- 60 days: Social Security survivor benefits, 401k rollover, COBRA health insurance

- 90 days: Update all beneficiaries, organize accounts, file insurance claims

- First year: Revise investment strategy, update estate planning, adjust withdrawal plan

Bottom line: You have about 60 days to make financial choices that'll impact the next 30 years. This guide walks you through each step.

Here's the thing nobody wants to tell you: You've got about 60 days to make financial decisions that'll impact the next 30 years of your life. While you're grieving. While you can barely remember if you fed the dog this morning.

If that sounds impossible, you're not wrong. But you're also not alone. My friend Janet went through this exact scenario three years ago, and she told me something that stuck: "The hardest part wasn't losing David. It was learning that the financial world doesn't give you time to breathe."

Three-quarters of women become financially vulnerable within five years of losing their spouse. But Janet isn't one of them. And you don't have to be either.

What to Do Financially When Your Spouse Dies: The 60-Day Timeline

When your spouse dies, the financial system keeps chugging along like nothing happened. It's cold, it's mechanical, and missing these deadlines can cost you serious money.

Week 1: Essential Widow Financial Planning Steps

Before you can make any smart moves, you need to figure out what you're working with. This is tough when you're already overwhelmed, but it's the foundation of everything else.

Death Certificates: Order More Than You Think

Order 10-15 certified copies, not 3 or 4. Every bank, insurance company, and government office wants their own original copy. Getting extras later is like trying to get concert tickets after they're sold out – expensive and frustrating.

Hunt down the financial stuff. Bank statements, insurance papers, retirement account docs, the last three years of tax returns. If your husband was the "finance guy" in your relationship, this stuff is probably scattered everywhere. Check that junk drawer in the kitchen, the filing cabinet that's been locked for five years, and yes, that mysterious box in the closet.

Make a list. I'm talking old-school pen and paper here. Every account, every policy, every monthly bill. Account numbers, phone numbers, balances if you can find them. This becomes your map for the next few months.

Week 2-4: Critical Financial Decisions for Surviving Spouses

This is where things get real. You're making choices you can't undo, so pay attention.

Surviving Spouse Social Security Benefits

Call them now. Not when you feel ready, not next week when your sister can drive you. Now.

You can get survivor benefits worth up to 100% of your husband's monthly Social Security payment. But here's where it gets interesting – and this is something most people don't know.

If you've got your own work record, you can play a little game with timing. You might take survivor benefits now and let your own benefit grow until age 70. Or flip it – take your benefit first and switch to survivor benefits later.

The $50,000 Mistake

The math here matters more than you think. My buddy Carlos is a financial planner, and he says getting this wrong can cost someone $50,000 or more over their lifetime. Don't guess. Let Social Security run the numbers for you.

Surviving Spouse 401k Rollover Decisions

Your husband's work retirement account needs attention fast. You've got 60 days to decide what to do with it, and the default option is usually terrible.

If you let them just cut you a check, they're gonna withhold 20% for taxes. Even if you plan to roll it over later. So that $200,000 in his 401(k)? They send you $160,000 and ship $40,000 straight to the IRS. Getting that money back means waiting for next year's tax refund, which is wasteful.

Instead, do what's called a "direct rollover" to a traditional IRA. Money goes from his 401(k) to your IRA, no taxes, no drama, no lost money.

Important Exception

If your husband was under 59½ when he died, you might want to leave some money in his 401(k) for a while. Why? Because you can pull money out of an inherited 401(k) without that pesky 10% early withdrawal penalty. Roll it to an IRA and you lose that advantage.

Health Insurance Reality

If you were on his work insurance, you've got 60 days to decide on COBRA. Yeah, it's expensive. You'll pay what his employer was covering, plus 2% extra. But depending on your health situation, it might still beat buying your own coverage.

Do the math. Compare COBRA to what's available on the marketplace. Don't just look at monthly premiums – check deductibles, out-of-pocket costs, and whether your doctors are covered. Insurance is boring until you need it, then it's everything.

Week 4-8: Your New Financial Reality

Now comes the fun part. And by fun, I mean the part where you realize your household income just dropped by 30-50% while most of your bills stayed exactly the same.

Social Security survivor benefits help, but they're usually less than what you had when both of you were alive. If you were both collecting Social Security, you keep the bigger check and lose the smaller one entirely. It's like financial musical chairs, except someone always loses.

Meanwhile, the mortgage doesn't care that you're alone now. Neither do property taxes, utilities, or car insurance. Some costs might even go up – like paying someone to do stuff your husband used to handle.

This is where you need to get real about your budget. Not tomorrow, not when you're feeling better. Now. Figure out what's coming in versus what's going out. If there's a gap, you need to know about it while you can still do something.

Widow Financial Planning: The 90-Day Cleanup Project

Once you've handled the urgent stuff, you get some breathing room. Use it wisely.

Update Everything (Yes, Everything)

Every account that had your husband as a beneficiary needs updating. Bank accounts, retirement accounts, life insurance, investment accounts. All of it.

This isn't just busy work. Janet told me she put this off for months after David died because it felt too final. Then she had a minor heart episode and realized if something happened to her, nobody would know where anything was. Her kids would've been stuck dealing with lawyers and probate courts.

While you're at it, update your own estate planning stuff. Your will probably says everything goes to your husband. Your power of attorney docs definitely name him. Time for a refresh.

The Account Mess

You might be looking at accounts scattered across half a dozen financial companies. His 401(k) here, your IRA there, life insurance money somewhere else. It's like financial whack-a-mole.

Consolidating can make life simpler, but don't just move money to move it. Moving stuff can trigger taxes or fees.

Multiple small savings accounts earning nothing? Yeah, combine those. But investment accounts with different purposes – emergency money, growth stuff, income investments – maybe keep those separate. Sometimes organization means keeping things organized, not just dumped in one pile.

The Tax Surprise That Bites Everyone

Here's something that caught Janet completely off guard: Your taxes are about to get way worse.

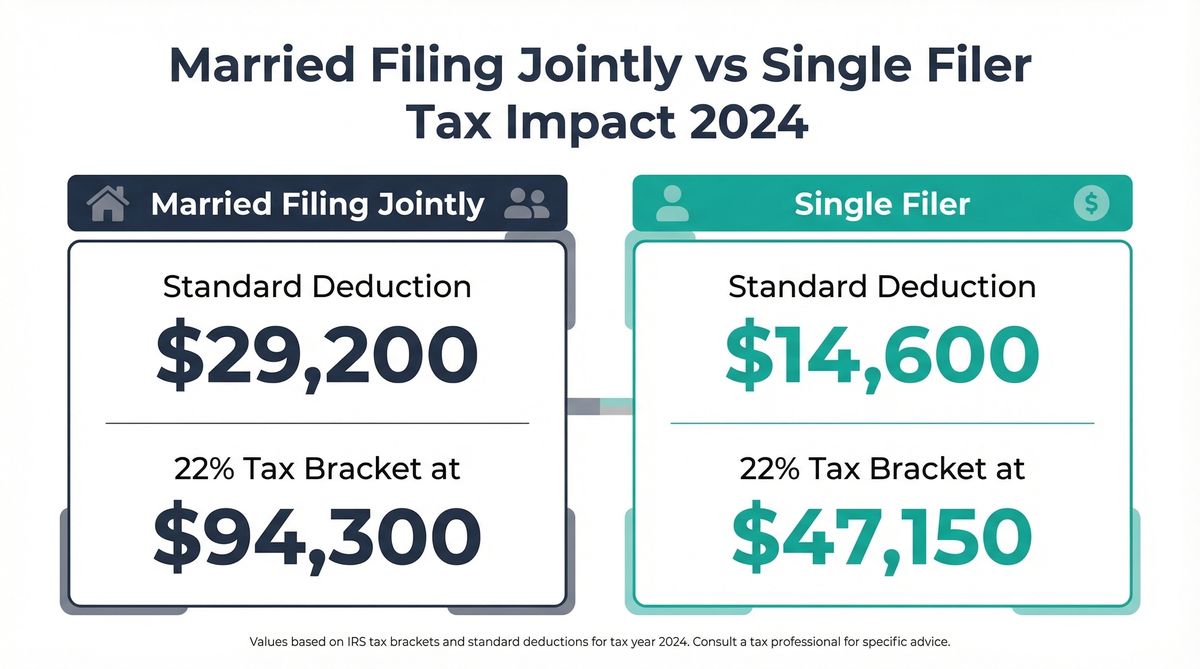

Last year you filed "married filing jointly," which has the best tax treatment. This year you're filing as "single," which is basically the government's way of saying "tough luck."

Married Filing Jointly

- Standard Deduction (2024) $29,200

- 22% Tax Bracket Starts $89,450

- Your Old Reality Better Rates

Single Filer

- Standard Deduction (2024) $14,600

- 22% Tax Bracket Starts $47,150

- Your New Reality Higher Taxes

So you might owe taxes on an extra $14,600 of income just because of your filing status. It's not the government being mean. It's just math. But it's math that can surprise you with a much bigger tax bill.

Working Around the Tax Hit

If you inherited traditional retirement accounts, be smart about pulling money out. Every dollar you withdraw counts as income, and now you're paying single-person rates.

Spread big withdrawals across multiple years instead of taking everything at once. If you don't need the money right away, let it keep growing while you figure out your new tax situation.

Life insurance money is usually not taxable, which is good news. But if it's sitting in a savings account earning basically nothing, it's not working very hard for you.

Widow Retirement Planning: Your New Game

Everything you thought you knew about retirement planning just got flipped upside down. You're not planning for two people anymore – you're planning for one person who might live a really long time.

The average 65-year-old woman has a 50% chance of living to 88. One in four makes it to 94. That's a lot of years to fund on less income.

The 4% Rule Needs a Rethink

Maybe you and your husband planned to pull 4% of your investments each year in retirement. That might not work anymore.

Your expenses didn't drop by half when your income did. You still need a place to live, food, healthcare, transportation. Some stuff might cost more – like paying for services your husband used to provide.

Plus, you're planning for potentially the same lifespan but with less money coming in from Social Security and pensions. The money has to stretch just as far with less coming in the door.

You might need to be more conservative with withdrawals, more aggressive with investments, or both. This is where getting professional help makes sense, especially if numbers make your head hurt.

Long-Term Care Gets More Important

When you're married, you have a built-in helper for everyday stuff. Doctor appointments, remembering medications, basic care when you're sick.

When you're alone, you're either paying for that help or relying on your kids who have their own lives. Long-term care insurance that seemed like a "nice to have" when you were married might now be essential.

Mistakes That Cost Real Money

Mistake #1: Waiting Too Long

Grief makes you want to put off big decisions, which makes total sense. But financial deadlines don't care about your emotional timeline. Missing those 60-day windows can cost thousands.

Mistake #2: Cashing Out Everything

When you're scared about money, it's tempting to cash out his 401(k) just to have cash in the bank. Don't do it.

Cashing out means paying taxes on everything, possibly pushing you into higher tax brackets. That $200,000 might only net you $140,000 after taxes, and you've given up decades of growth.

Mistake #3: Changing Nothing

Your husband's investment strategy was designed for a couple's retirement, not a single woman's future. Your situation is different now. Your strategy should be different too.

Mistake #4: Doing Everything Alone

There's no shame in getting help. A good financial planner can help with Social Security decisions and withdrawal strategies. A CPA can help with tax planning. An estate attorney can update your legal docs.

Yeah, professionals cost money. But screwing up six-figure financial decisions costs more.

| Month | Focus | Key Actions |

|---|---|---|

| 1 | Crisis Management | Death certificates, Social Security, 401k rollover, health insurance |

| 2-3 | Organization | Update beneficiaries, account inventory, insurance claims, tax planning |

| 4-6 | Strategy | Financial planner, estate documents, withdrawal plan, LTC insurance |

| 6-12 | Implementation | New investment strategy, spending adjustments, support network |

Moving Forward

Look, losing your spouse changes everything about money. From daily budgets to 30-year plans. The decisions you make in the first few months matter a lot, but they don't have to be perfect.

Your goal isn't to optimize every detail right away. It's to avoid the big mistakes while you figure out what your new life looks like.

You're not the same person you were when you were married. Your money plan shouldn't be the same either. That's not failure – that's adapting.

If all this planning feels overwhelming, tools like Ready Aim Retire can help you run different scenarios and see how various decisions might play out. But remember, spreadsheets are just one piece of the puzzle. Your comfort with your plan matters as much as the math.

Take it one decision at a time. You don't need to solve the next 30 years this week. Just get through the first 60 days without major mistakes, and you'll have built a solid foundation.

The money side of widowhood is hard, but it's learnable. And you're tougher than you think.

🎯 Your Next Steps

- If it's been less than 60 days: Focus on the critical deadlines - Social Security, 401k rollover, health insurance. Everything else can wait.

- If it's been 60-90 days: Start the cleanup project - update beneficiaries, organize accounts, begin tax planning for your new filing status.

- If it's been more than 90 days: Time for strategic planning - meet with professionals, update legal documents, revise your retirement plan.

- Remember: You don't have to figure out everything at once. Progress over perfection.

Peace!