84% of Retirees Make This RMD Mistake — And It's Costing Them Big.

- 84% of retirees only take the minimum required distribution (RMD), creating a "tax time bomb" that gets worse every year

- The problem: This leads to underspending in your active years, higher taxes later, and Medicare surcharges that can cost $487/month

- Smart strategies: Budget-first withdrawals, Roth conversions during the "gap years" (59½-73), and Qualified Charitable Distributions

Your RMD is a minimum, not a target. Taking more now often means lower lifetime taxes and better cash flow when you can actually enjoy it.

"I take exactly what the government tells me to take from my IRA," he said. "Nothing more. Figured that was the safe play."

Turns out David's making the same mistake as 84% of retirees, according to a massive JPMorgan Chase study that looked at 31,000 people entering retirement. They found that once people hit RMD age, the vast majority only withdrew the bare minimum from their retirement accounts.

80% of retirees who hadn't yet reached RMD age weren't touching their accounts at all.

I get it. On the surface, that sounds responsible. You saved this money for decades — why rush to spend it? But here's the thing: this "play it safe" approach is quietly doing some serious damage. We're talking lower spending during the years you're healthiest, a growing tax nightmare that gets worse every year, and a financial mess that eventually gets dumped on your kids.

Let me walk you through why the minimum isn't actually the smart move — and what you should be doing instead.

The Required Minimum Distribution Problem Most People Don't See Coming

When you turn 73 (or 75 if you were born in 1960 or later), Uncle Sam says you *must* start pulling money from your traditional IRA or 401(k). That's your Required Minimum Distribution — your RMD. Miss it, and you'll get walloped with a 25% penalty on whatever you should have taken out.

So most folks do exactly what they're told: take the minimum and not a penny more.

It feels logical. You're preserving your nest egg. Being careful. Your financial advisor probably even nods along.

The RMD approach is inefficient. It does not generate income that supports retirees' declining spending behavior and may leave a sizable account balance at age 100.

Think about this for a second. You could die with a massive account balance — not because you planned it that way, but because you let the IRS formula run your retirement instead of running it yourself.

Why "Just Take the RMD Minimum" Actually Backfires

Your Tax Bill Gets Worse, Not Better

This is the big one, and most people completely miss it.

Every year you take only the required minimum distribution, the rest of your tax-deferred money keeps growing. And growing. Which means your future RMDs keep getting bigger too.

Let me give you a real scenario that might hit close to home:

Rosa's RMD Reality Check

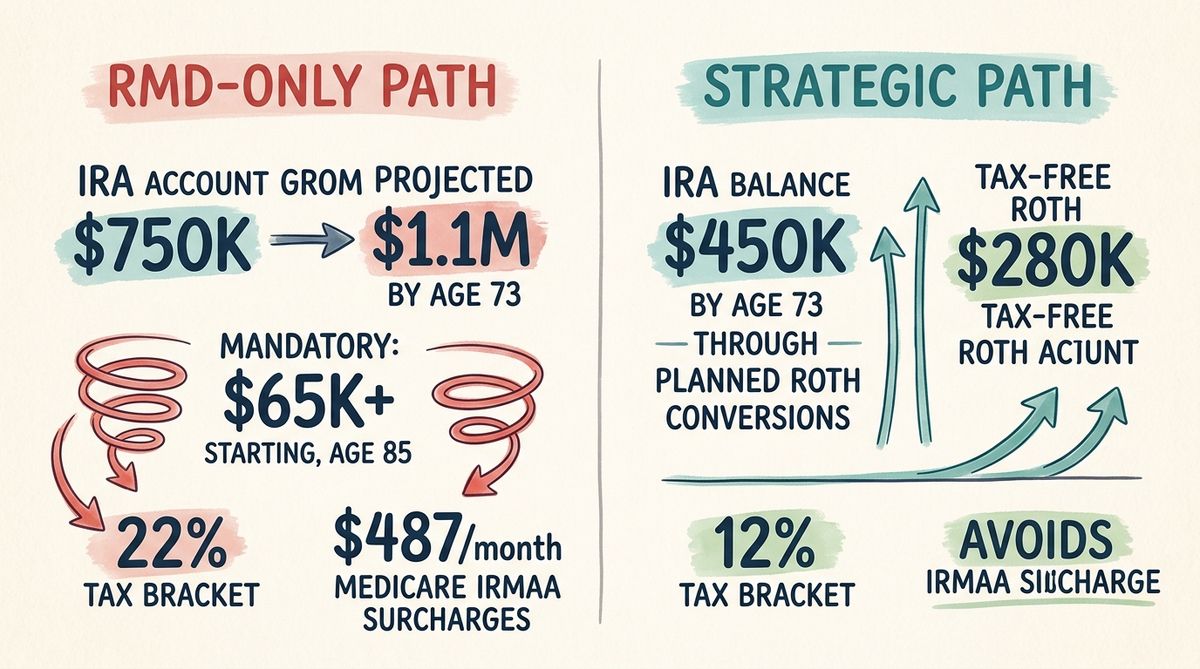

My client Rosa retired at 65 with $750,000 in a traditional IRA. By age 85 with only minimum withdrawals, her RMDs exceed $65,000/year — pushing her into the 22% tax bracket and triggering $487/month Medicare surcharges.

My friend Rosa retired at 65 with $750,000 in a traditional IRA. Smart lady — she didn't touch it until RMDs kicked in at 73. With 5% annual growth (pretty reasonable), her IRA had ballooned to roughly $1.1 million by then.

Her first RMD? About $41,000. Add her $28,000 in Social Security, and she's looking at $69,000 in taxable income.

But here's where it gets painful. By age 85, with continued growth and only minimum withdrawals, her IRA could be worth $1.3 million. Her RMDs would exceed $65,000 a year. Combined income: over $93,000. She's now in the 22% tax bracket and paying those Medicare IRMAA surcharges — extra premiums that kick in when your income tops $109,000 for single filers ($218,000 for married couples). Those surcharges can add up to $487 per month.

So Rosa spent her early retirement living on less than she needed to, only to face higher taxes and bigger Medicare bills in her 80s when she's naturally spending less anyway.

That's not conservative planning. That's accidentally making retirement harder than it needs to be.

You're Living on Less Than You Should in Early Retirement

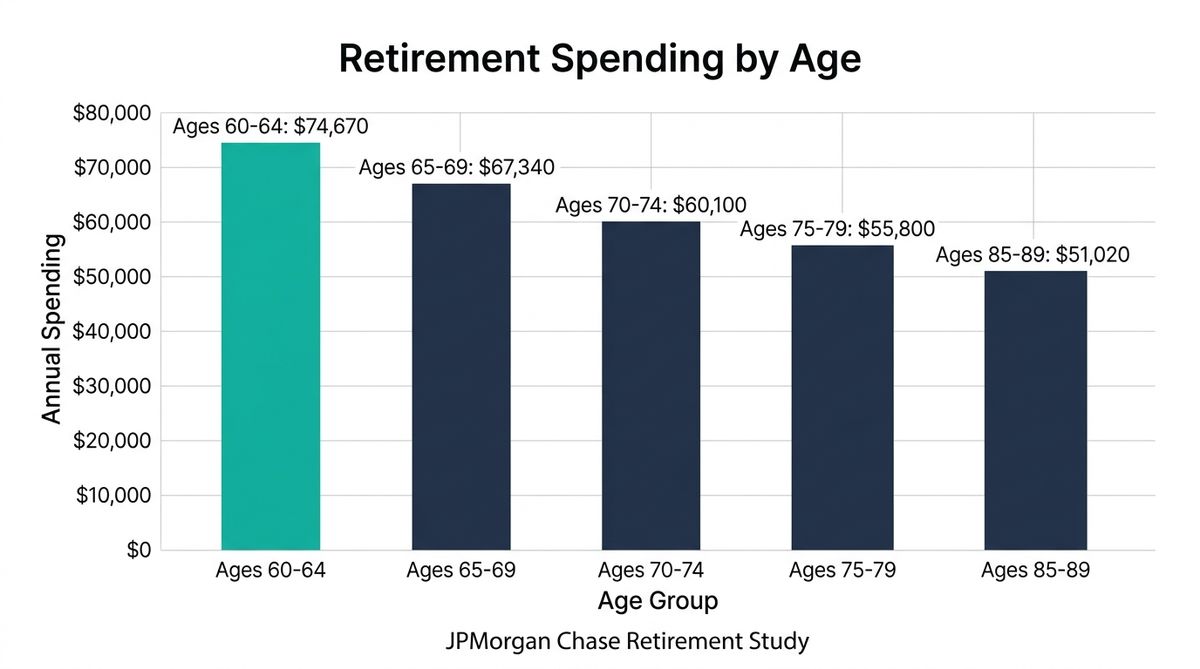

Here's something that really gets me: JPMorgan's research shows that retirees spend the most in their 60s and early 70s — what they call the "go-go years." That's when you're traveling, renovating the house, picking up new hobbies, actually enjoying the retirement you worked so hard for.

The Spending Curve Reality

JPMorgan found that for households with $250K–$750K in investable assets, spending goes from about $74,670 between ages 60–64 down to roughly $51,020 by ages 85–89.

So what happens when you only take the minimum? You artificially squeeze your retirement income during the years you'd actually use and enjoy the money. Then the IRS forces you to take *more* money in your 80s and 90s — when you need it least and it costs you the most in taxes.

The RMD formula doesn't know you want to take your grandkids on vacation at 68. It doesn't know you'd love to renovate that kitchen at 70. It just applies a boring government divisor to your balance and spits out a number.

We can do better than that.

Your Kids Inherit a Tax Mess

Under the SECURE Act, most non-spouse beneficiaries have to empty an inherited IRA within 10 years. If you leave behind a $1 million traditional IRA, your children are forced to take roughly $100,000 per year in taxable distributions — on top of whatever they're already earning.

That could easily push them into the 32% or even 35% tax bracket.

My buddy Mike in Portland told me his dad left him a massive traditional IRA, and between his engineering salary and the forced distributions, he's paying more in taxes than he ever thought possible. "Dad was trying to be responsible," he said, "but it would have been better if he'd spent more of it himself."

By strategically drawing down your accounts during your lifetime, you reduce the balance — and the tax burden — your heirs inherit. It's one of those rare situations where spending more now actually helps your family later.

How to Avoid the RMD Mistake 84% of Retirees Make

1. Create a Retirement Income Plan (Budget First, RMD Second)

This is hands down the most important shift you can make.

Instead of letting some IRS formula dictate your cash flow, start with this question: *What do I actually want my retirement to look like?*

Build a retirement income plan based on your real spending needs. Figure out what your go-go years cost, what your slow-go years might look like, and plan withdrawals around that — not around some table the government published decades ago.

RMD-Only Approach

- Age 100 balance: $20,000+

- Early spending: Artificially low

- Late-life taxes: High

- Quality of life: Restricted

Spending-Based Approach

- Age 100 balance: ~$2,000

- Early spending: Optimal

- Late-life taxes: Lower

- Quality of life: Maximized

The JPMorgan study found that a 72-year-old with $100,000 using the RMD approach would still have over $20,000 left at age 100. Using a spending-based approach? Just a couple thousand. The difference isn't waste — it's decades of higher quality of life.

Your RMD is a *minimum*, not a target. There's no penalty for withdrawing more. You just have to pay the taxes, which you'd pay eventually anyway — and likely at a higher rate if you wait.

2. Use the "Gap Years" for Roth IRA Conversions

If you retire before 73, you've got what I like to call a golden window that most people completely waste.

The years between retirement (or age 59½, when you can withdraw penalty-free) and RMD age are often your lowest-income years. Your paycheck is gone, Social Security might not have started yet, and your tax bracket is probably lower than it's been in decades.

This is the perfect time to convert chunks of your traditional IRA to a Roth IRA.

Why? Roth IRAs have no RMDs during your lifetime. The money grows tax-free and comes out tax-free. Every dollar you convert now is a dollar that won't inflate your RMDs later.

Let's go back to my friend Rosa. In a smarter version of her story, she takes $40,000 per year from her IRA starting at 65 for living expenses, and converts $30,000 per year to a Roth during ages 65–72.

By 73, her traditional IRA is around $450,000 instead of $1.1 million. Her first RMD drops to roughly $16,400. Her Roth has grown to about $280,000 — money that will never be taxed and never trigger an RMD.

Her combined income stays in the 12% bracket. No IRMAA surcharges. And she had $40,000 a year in spending money during her most active years.

Same total savings. Completely different outcome.

A few things to keep in mind with Roth IRA conversions:

- Pay conversion taxes from non-retirement money if you can. Using IRA funds to pay the tax bill defeats part of the purpose.

- Convert gradually over multiple years. A massive one-time conversion can spike your income and push you into a higher bracket — or trigger those IRMAA penalties.

- Watch the IRMAA threshold. Medicare looks at your income from two years ago. A conversion in 2026 affects your 2028 premiums.

- Conversions are permanent under current law. Once you convert, there's no going back.

- Mind the pro-rata rule if you have both pre-tax and after-tax IRA contributions.

3. Use Qualified Charitable Distributions for Tax-Efficient RMDs

If you give to charity — even just a few hundred bucks a month — this strategy is basically a no-brainer.

Starting at age 70½, you can transfer money directly from your IRA to a qualified charity. This counts toward your RMD but is completely excluded from your taxable income. The 2025 annual limit is $108,000 per person.

Here's how it works in the real world:

My client Tom is 74 with a $500,000 traditional IRA. His RMD is about $20,000. He donates $10,000 a year to his church and the local food bank anyway — has been doing it for years.

Instead of taking the full $20,000 as taxable income and then writing a $10,000 check to charity, he directs $10,000 of his RMD straight to the charities as a QCD. Only $10,000 shows up as taxable income.

Same charitable impact. Same money to the causes he cares about. But his tax bill is significantly lower. And here's a bonus: he doesn't even need to itemize deductions to benefit from the QCD. With the standard deduction being what it is, most retirees don't itemize — which means regular charitable donations don't reduce their taxes at all. QCDs do.

The key rules: the transfer has to go directly from your IRA to the charity (not to you first), and it only works with IRAs — not 401(k)s or other employer plans.

4. Consider Strategic Early Retirement Withdrawals

You don't have to wait until 73 to start pulling money from your retirement accounts. Once you hit 59½, there's no early withdrawal penalty.

The strategy: each year, take distributions that "fill up" your current tax bracket. If the 12% bracket covers income up to $47,150 for a single filer (2026 figures) and your other income is $20,000, you could withdraw $27,150 from your IRA and still stay in the 12% bracket.

This systematically reduces your balance before RMDs begin. You pay taxes at today's known rates instead of gambling on what future rates and future RMDs will look like. And you can reinvest the after-tax money in a regular brokerage account, where future gains get the more favorable long-term capital gains rate instead of ordinary income rates.

What About Retirees Who Don't Need the Money?

Fair question. Some retirees have solid pensions, Social Security, and other income that covers their needs. They truly don't need IRA withdrawals for daily expenses.

Christine Benz from Morningstar makes an important distinction: "It's a required minimum distribution, not required minimum spending. You have to pull the money out... but you don't have to spend it."

If you take your RMD and don't need it for living expenses, you've got options:

- Reinvest in a taxable brokerage account. You'll pay taxes on the distribution, but future growth gets long-term capital gains treatment.

- Fund a Roth IRA — if you have earned income, you can contribute up to the annual limit.

- Use QCDs if you're charitably inclined.

- Gift it to family members (up to the annual gift tax exclusion).

The point isn't that you *must* spend the money. It's that you should plan proactively rather than defaulting to the minimum and hoping it all works out.

The Tax Cascade Effect Nobody Talks About

What makes the RMD-only approach so damaging is that the problems compound. It's not just one issue — it's a cascade:

| Problem | Leads To | Annual Impact |

|---|---|---|

| Larger account balance | Bigger required minimum distributions | Exponential growth |

| Bigger RMDs | Higher taxable retirement income | Tax bracket creep |

| Higher income | Medicare IRMAA surcharges | Up to $487/month |

| Higher income | Social Security taxation | Up to 85% taxable |

| Larger remaining balance | Tax burden on heirs | 10-year forced distributions |

Each piece makes the others worse. And by the time most people notice what's happening, they're in their late 70s or 80s and the window for the most effective strategies — especially those Roth conversions during the gap years — has already slammed shut.

Frequently Asked Questions About RMD Strategy

Can I Take More Than My Required Minimum Distribution?

Yes! Your RMD is a minimum, not a maximum. There's no penalty for withdrawing more from your IRA or 401(k).

When Do Required Minimum Distributions Start?

Age 73 if you were born between 1951-1959, or age 75 if you were born in 1960 or later.

What's the Penalty for Missing an RMD?

25% excise tax on the amount you should have withdrawn, but this can be reduced to 10% if you correct it within two years.

Do Roth IRAs Have Required Minimum Distributions?

No. Roth IRAs have no RMDs during the original owner's lifetime, which is why they're so valuable for tax planning.

Can I Use QCDs Before Age 73?

Yes! You can start using Qualified Charitable Distributions at age 70½, even before your required distributions begin.

What To Do Right Now

- Stop treating your RMD as your withdrawal plan. It's a tax compliance mechanism, not a retirement strategy. Build a real plan based on how you want to live.

- Calculate your "gap years" opportunity. If you're between 59½ and 73, you're in prime Roth conversion territory. Don't waste it.

- Review your charitable giving. If you donate to charity, QCDs starting at 70½ can significantly reduce your tax burden.

- Consider strategic early withdrawals. "Fill up" lower tax brackets now instead of being forced into higher ones later.

Look, I've spent years helping people navigate this stuff, and the biggest regret I hear from retirees isn't that they spent too much. It's that they spent too little during the years when they could have really enjoyed it.

Your retirement savings exist to fund your retirement. Not to sit in an account.

You're wiser than that!

Explore Ready Aim Retire Tools

Happy spending!