FIRE Types Explained: Which Financial Independence Path Fits Your Life?

By Ross Williams • April 5, 2026

You know that feeling when you're staring at the clock, willing it to hit 5 PM? Yeah, we've all been there. But what if I told you that some people never have to do that again? Not when they turn 65 like everyone expects, but in 10 years. Maybe 15. Geez, some folks I know pulled it off in just 5.

This isn't some get-rich-quick fantasy. It's FIRE (Financial Independence, Retire Early), and real people are doing it every single day. But here's the thing most folks miss: financial independence isn't one approach fits everyone. It's more like choosing a coffee order. Some people want it black and simple, others want the full caramel macchiato with extra everything.

There are five main FIRE strategies, each targeting different lifestyles and savings goals:

- LeanFIRE: $40K/year or less • $1M needed

- ChubbyFIRE: $60K-$100K/year • $1.5M-$2.5M needed

- FatFIRE: $100K+/year • $2.5M+ needed

- BaristaFIRE: Portfolio + part-time work

- CoastFIRE: Save hard early, then coast to traditional retirement

The trick is picking the version that actually matches how you want to live.

We have subscribers doing FIRE all different ways. Sam in Berlin lives amazing on $30K a year. David in Washington DC needs $150K to feel comfortable. Both are very happy, just taking completely different paths.

Why Picking Your FIRE Strategy Actually Matters Right Now

The FIRE movement has blown up over the last few years, but 2026 is throwing some curveballs that make choosing smart more important than ever.

Healthcare costs? They're brutal. We're talking $1,100+ every month for ACA coverage if you retire early. Inflation has people scrambling to adjust their withdrawal strategies. On the flip side, the IRS just bumped IRA contribution limits to $7,500 (up from $7,000), which is great news if you can max it out.

2026 Reality Check

Healthcare costs for early retirees have increased 40% since 2022, making strategy selection more critical than ever. The answer isn't giving up on early retirement dreams—it's picking the right strategy for your actual situation.

LeanFIRE: Living Well on Less

What is LeanFIRE?

Target spending: $40,000 or less per year

Savings needed: ~$1 million (using 4% rule)

Best for: Minimalists who genuinely love simple living

LeanFIRE is all about hitting financial independence on a tight budget. We're talking $40,000 or less per year, which means you need roughly $1 million saved up if you follow the traditional withdrawal strategy.

Sarah figured this out perfectly. She's a graphic designer making $70K, and she calculated she could live really well on $35K annually. Her magic number? $875,000. She's saving 50% of her income and should hit LeanFIRE in about 15 years.

The math works, but let's be honest about what this means. You're cooking at home most nights. You're picking your entertainment carefully. You're embracing minimalism as a way of life.

LeanFIRE Advantages

- Lower savings target ~$1M

- Shorter timeline 10-15 years

- Freedom from high income needs ✓

- Geographic flexibility High

Reality Checks

- Emergency cushion Limited

- Healthcare costs Challenging

- Lifestyle flexibility Restricted

- Inflation risk High impact

FatFIRE: Keeping the Good Life

What is FatFIRE?

Target spending: $100,000 to $200,000+ per year

Savings needed: $2.5 million to $5+ million

Best for: High earners who want to maintain their current lifestyle

FatFIRE sits on the other end of the spectrum. These folks want early retirement without giving up their current lifestyle. We're talking $100K to $200K+ in annual spending, which means saving $2.5 million to $5 million.

Mark is a software exec making in $300K who wants to keep spending his current $150K per year in retirement. His FatFIRE number is $3.75 million. Even saving 60% of his income (which is aggressive), he's looking at 20+ years.

FatFIRE makes sense for people who love their lifestyle but can't stand their jobs anymore.

International travel, nice houses, great restaurants, helping out family members. All of that stays on the table.

The catch: You need sustained high income and serious saving discipline for years. When markets tank, your timeline can get pushed back significantly. Plus, having that much money invested means you're more exposed when sequence of returns risk becomes a factor.

BaristaFIRE: The Best of Both Worlds

What is BaristaFIRE?

Strategy: Portfolio covers most expenses + part-time income

Savings needed: $600K to $1M (varies by part-time income)

Best for: People who want flexibility but enjoy some work

This might be my favorite FIRE flavor because it's so practical for regular folks. Instead of saving enough to cover everything, you save enough to cover most of your expenses, then work part-time to fill the gap.

My neighbor Lisa nailed this approach. She needs $60K annually. Instead of saving $1.5 million for full FIRE, she saved $875K and makes $25K from part-time consulting. Her portfolio handles the other $35K at a 4% withdrawal rate.

The beauty is you cut hundreds of thousands off your required savings while keeping income and often health benefits. And the part-time work doesn't have to be slinging coffee (though nothing wrong with that). Lisa does freelance marketing. My cousin teaches yoga. Another friend drives for a tour company.

Why BaristaFIRE Works So Well

BaristaFIRE admits something many FIRE purists won't: complete retirement isn't for everyone. Some people thrive with the purpose and routine that work provides. They just don't want the 40-hour weeks, commutes, and demanding bosses.

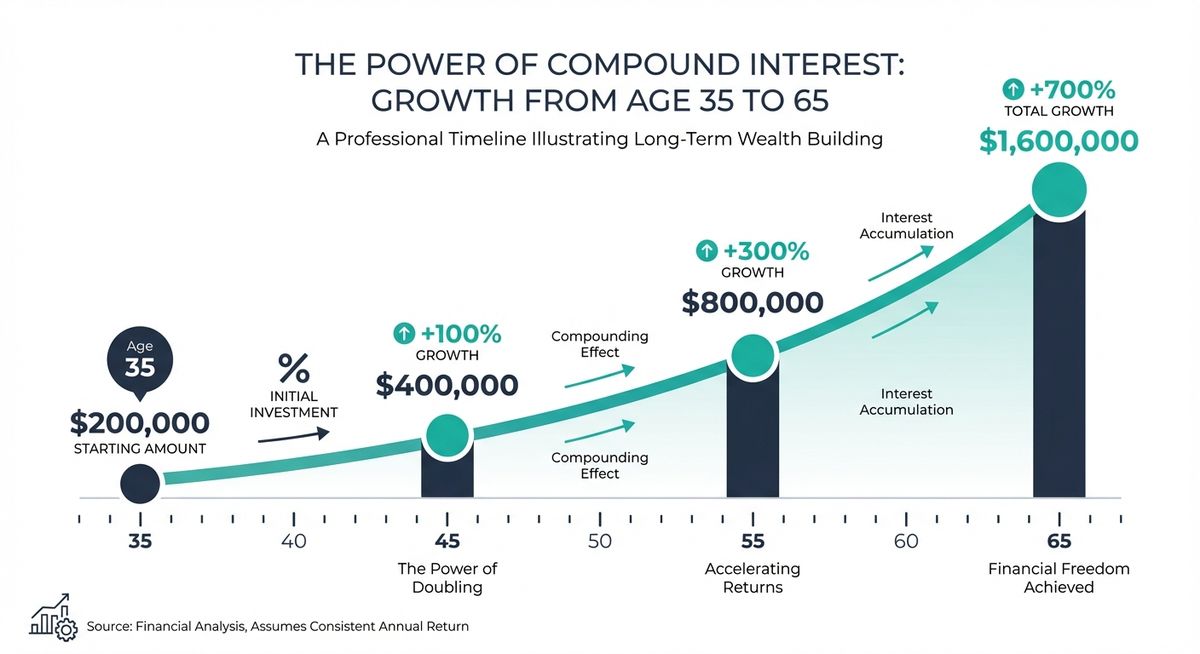

CoastFIRE: The Early Bird Gets the Compound Interest

What is CoastFIRE?

Strategy: Save aggressively early, then let compound interest do the work

Timeline: Reach "coast number" by 30-35, retire traditionally at 60-65

Best for: Young high earners who want long-term security

CoastFIRE is all about hitting compound interest hard in your early years when it matters most. You save aggressively when you're young, then coast on growth.

Jennifer figured this out at 25. She calculated that getting $200K saved by age 35 would grow to $1.6 million by 60 (assuming 7% annual returns). After hitting her CoastFIRE number at 35, she can dial way back on saving but still retire comfortably at normal age.

The math is pretty sweet. That $200K at age 35 becomes:

- $400K at 45

- $800K at 55

- $1.6 million at 65

The psychological win: Once you hit your CoastFIRE number, you know you'll be fine no matter what. Want to switch to that lower-paying job you'd actually enjoy? Go for it. The financial pressure is off.

ChubbyFIRE: The Sweet Spot in the Middle

What is ChubbyFIRE?

Target spending: $60,000 to $100,000 per year

Savings needed: $1.5 million to $2.5 million

Best for: Upper-middle-class folks who want more than bare bones but don't need luxury

ChubbyFIRE sits between regular FIRE and FatFIRE, targeting $60K to $100K in annual spending. It's perfect for upper-middle-class folks who want more than bare bones but don't need luxury.

You'll need $1.5 to $2.5 million saved, which is totally doable for households making $100K to $200K with solid saving over 15-20 years.

How to Pick Your Financial Independence Strategy

Choosing comes down to three big factors:

Income-Based Guidelines

- Under $75K LeanFIRE or CoastFIRE

- $75K-$150K BaristaFIRE or ChubbyFIRE

- Over $150K FatFIRE becomes realistic

Risk Tolerance

- Play it safe CoastFIRE or BaristaFIRE

- Comfortable with risk LeanFIRE or aggressive FatFIRE

- Somewhere in between ChubbyFIRE

What you actually want your life to look like: Be honest here. If you love nice restaurants, travel, and quality stuff, don't kid yourself that you'll be happy with LeanFIRE. On the flip side, if you genuinely prefer simple living, don't assume you need FatFIRE to be content.

The 2026 Reality Check: What Every FIRE Plan Needs to Handle

Healthcare costs are absolutely crushing people. Retiring before Medicare kicks in at 65 can mean massive healthcare expenses. This reality has pushed lots of folks toward BaristaFIRE just to keep employer coverage and bridge the gap.

The 4% rule is getting stress-tested by inflation. That traditional 4% withdrawal rate assumes historical returns and inflation. Some experts now suggest 3.5% or flexible strategies that adjust when markets get crazy.

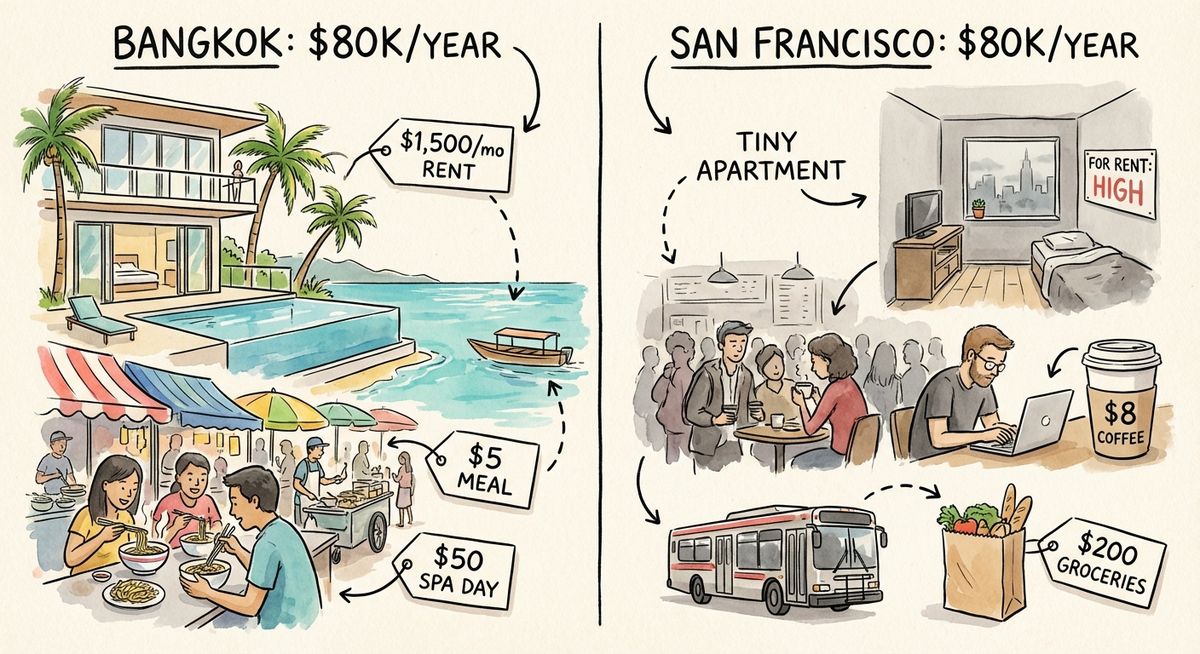

Where you live matters more than ever. Your FIRE number in San Francisco could fund a luxury lifestyle in Mexico or Thailand. Lots of people now build international moves into their planning from day one.

🎯 Your 5-Step FIRE Game Plan

- Step 1: Figure out what you actually spend Track everything for three months. Most people seriously underestimate their real costs.

- Step 2: Get specific about your dream retirement Travel the world? Live quietly? Help family? Paint a clear picture of what you want life to look like.

- Step 3: Run your FIRE numbers Use the 4% rule as a starting point: multiply annual spending by 25 to get your target.

- Step 4: Max out your savings potential With 2026 IRA limits at $7,500 (plus $1,100 catch-up if you're 50+), prioritize tax-advantaged accounts first.

- Step 5: Stay flexible You can mix strategies. Many people save for CoastFIRE, then switch to BaristaFIRE for early retirement flexibility.

| FIRE Type | Annual Spending | Savings Target | Timeline | Best For |

|---|---|---|---|---|

| LeanFIRE | $25K-$40K | $625K-$1M | 10-15 years | Minimalists, location flexible |

| ChubbyFIRE | $60K-$100K | $1.5M-$2.5M | 15-20 years | Upper-middle class, balanced lifestyle |

| FatFIRE | $100K+ | $2.5M+ | 20+ years | High earners, luxury lifestyle |

| BaristaFIRE | Portfolio + Work | $600K-$1M | 12-18 years | Part-time work enthusiasts |

| CoastFIRE | Traditional timing | $200K by 35 | 30+ years total | Young savers, long-term planners |

Plan Your First 5 Years Carefully

Once you reach financial independence, the first five years of retirement are absolutely critical. This is when market volatility can do the most damage to your long-term financial security.

Here's the Thing: Your FIRE Should Fit You

Financial freedom isn't about picking the "correct" FIRE flavor. It's about picking the right one for you, then consistently working toward it.

The best part about all these FIRE flavors is choice. You don't have to copy someone else's early retirement vision. Whether your path involves tiny houses or luxury travel, passion projects or complete work exit, there's a strategy that fits.

The key is being honest with yourself. What lifestyle do you actually want? What savings rate can you realistically keep up? How much uncertainty can you handle without losing sleep?

Start where you are, use what you've got, and adjust as your life changes. Trust me, future you will be incredibly grateful you started today, no matter which FIRE path you choose.

Thanks for reading if you've made it this far!

Happy saving!