Why the 4% Rule Is Broken in 2026 (And What to Do Instead)

So you saved a million bucks. Congrats — seriously. You did the thing most people never do. You ran the math: 4% of a million is $40,000 a year, toss Social Security on top, and you're golden. Except...

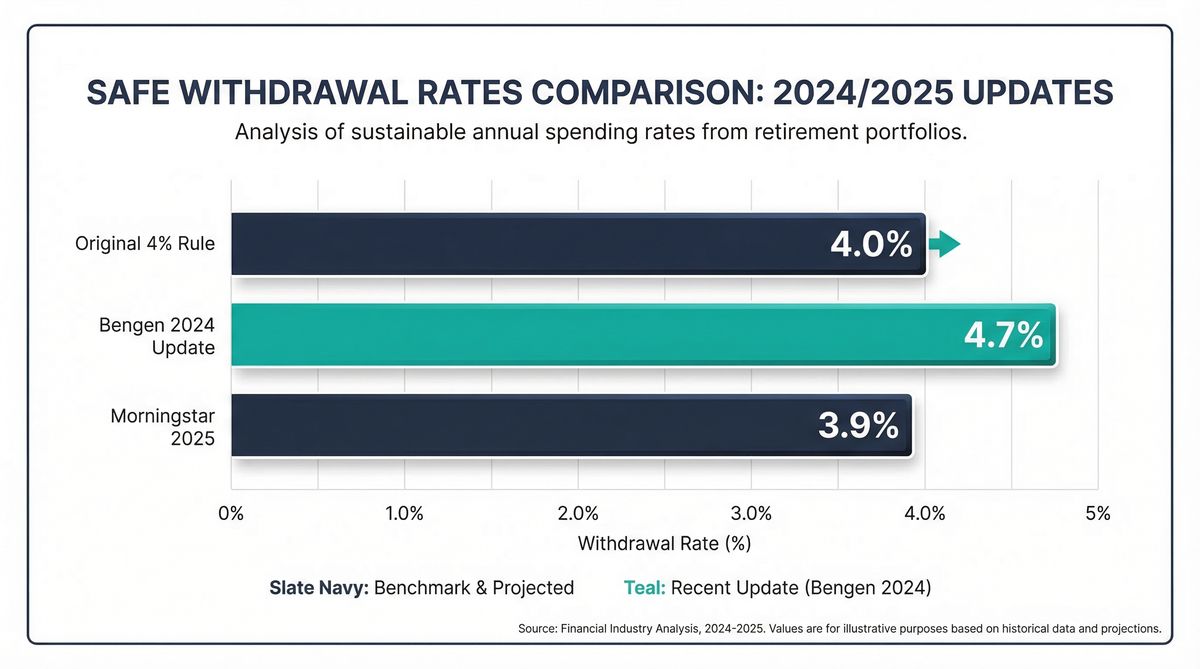

- The creator of the 4% rule now says 4.7%. Morningstar says 3.9%. That's an $8,000/year gap on a million-dollar portfolio.

- Sequence of returns risk — not market crashes — is the real retirement killer.

- Better strategies exist: the bucket strategy, guardrails method, bond ladders, and the part-time bridge.

- The retirees who stress least aren't the richest — they're the most flexible.

Start at 4%, keep 2-3 years in cash, and stay ready to adjust. Flexibility beats formulas.

Because the guy who invented the 4% rule just changed his own number. And the two most respected voices in retirement research can't even agree on what the new number should be.

Bill Bengen — the financial planner who published the original 4% rule back in 1994 — dropped a book last August bumping his recommendation to 4.7%. Then Morningstar comes out in December 2025 and says nah, the safe withdrawal rate for 2026 retirees is 3.9%.

Bengen's Updated Number

- Withdrawal Rate 4.7%

- On $1M Portfolio $47,000/yr

- Approach Historical worst-case

- Requires Small-cap value + intl. bonds

Morningstar's 2025 Report

- Withdrawal Rate 3.9%

- On $1M Portfolio $39,000/yr

- Approach Forward-looking projections

- Requires Balanced portfolio, adjust as you go

That's an $8,000-a-year gap on a million-dollar portfolio. Eight grand. That's not a rounding error.

Here's the thing though — they're both right. They're just answering different questions. And understanding why they disagree might be the single most useful retirement planning thing you read this year.

What the 4% Rule Actually Says (Because Most People Get This Wrong)

Quick history lesson.

In 1994, Bengen went back and looked at every 30-year retirement period since 1926. He wanted to find the absolute worst-case scenario — like, the unluckiest person in history retiring at the worst possible time — and figure out the max they could've pulled out each year without going broke.

His answer: 4%. Take out 4% of your portfolio in year one, adjust that dollar amount for inflation every year after. Even the most cursed retiree in history would've been fine.

The 4% Rule — What It Actually Means

Withdraw 4% of your portfolio in year one of retirement. Each year after, adjust that dollar amount for inflation — not 4% of the current balance. Based on a 50/50 stock-bond portfolio over a 30-year horizon. It was designed as the worst-case floor, not a recommended target.

But here's what basically everyone gets wrong: 4% was the floor, not the ceiling. In the average scenario, retirees could've safely pulled around 7%. The 4% was worst-of-the-worst. It was the "even if you retire the day before the apocalypse" number.

The other thing people miss: Bengen assumed a plain 50/50 stock-bond portfolio, specific bond yields, and exactly 30 years. Change any of those and you get a different number. These are the core 4% rule problems that most retirement advice glosses over.

My buddy Jake retired two years ago thinking 4% was like... a law of physics. It's not. It's a starting point from 1994 based on specific assumptions. Good research but not gospel.

The Problems With the 4% Rule in 2026

The Shiller CAPE ratio — that's just a fancy way to measure how expensive the stock market is compared to what companies actually earn — is sitting around 39 right now.

The CAPE Ratio Is Flashing a Warning

At ~39, today's Shiller CAPE ratio is nearly 2.5x the long-term average of 16. The only time it was higher? Late 1999, right before the dot-com crash. History says: when you buy expensive, the next decade's returns tend to disappoint.

For comparison, the long-term average is about 16. The only time the CAPE was higher than this? Late 1999 at the peak of the dot-com bubble, when it hit 44.

Does this mean the market's gonna crash tomorrow? Nobody knows. But history's crystal clear on one thing: when you buy stocks at crazy-high prices, your returns over the next decade tend to suck.

Plus the S&P 500's top 10 stocks now make up over 35% of the whole index. So your "diversified" index fund? Not as diversified as the name suggests.

If you're still working, this is interesting bar trivia. If you're about to retire and start pulling money out? This is everything.

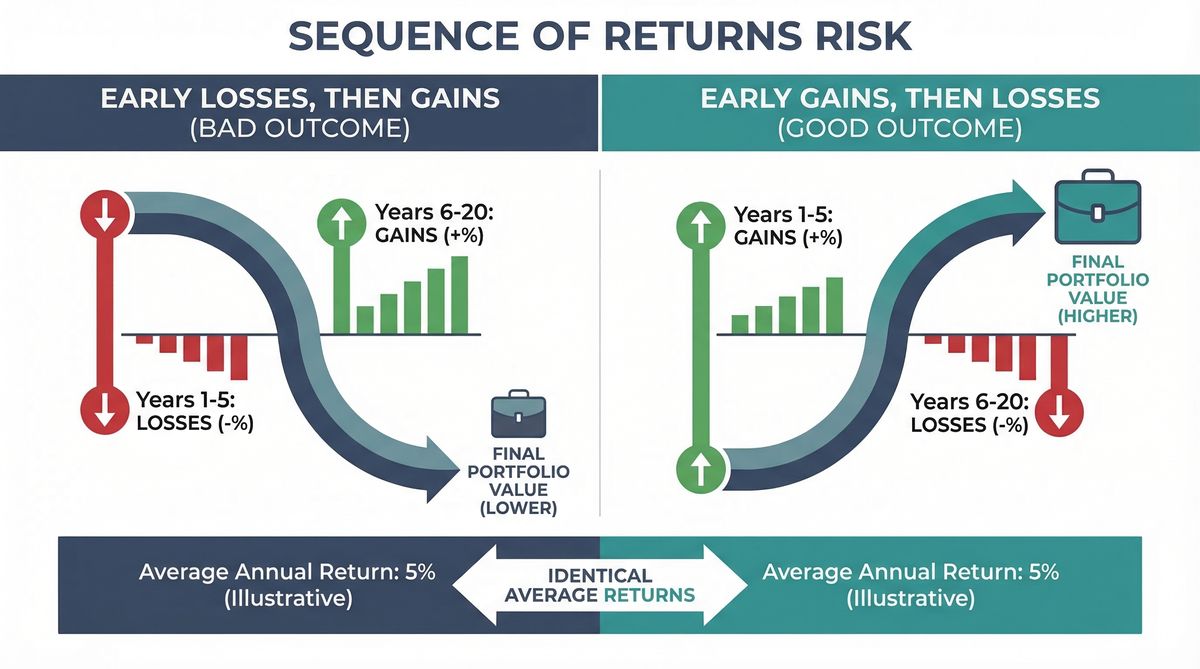

The Real Retirement Killer (And It's Not What You Think)

The thing that actually ruins retirement portfolios isn't market crashes. It's something called sequence of returns risk — basically, bad luck with timing.

Sequence of Returns Risk

The risk that poor investment returns in the early years of retirement will permanently deplete your portfolio — even if your long-term average returns are perfectly fine. It's the order of returns that matters, not just the average.

Here's the weird part: Two people can earn the exact same average return over their retirement, but the one who gets hammered early ends up way worse off.

Picture two retirees, both starting with a million bucks, both pulling $40,000 a year. They get the exact same returns — just in opposite order. After six years, the one who hit losses first has about $178,000 less than the lucky one. Same returns. Same withdrawals. Completely different outcomes.

You can do everything right and still get screwed by timing. That's sequence of returns risk — retirement roulette.

4% Rule Alternatives That Actually Work in 2026

Forget the 4% rule. Here's what smart people are doing instead:

1. The Bucket Strategy (Most Popular)

Split your money into three buckets:

- Short-term (years 1-3): Cash and CDs. Boring. Safe.

- Medium-term (years 4-10): Conservative bonds, maybe some dividend stocks.

- Long-term (years 11+): Growth stocks, index funds, the fun stuff.

When the market's up, you sell some long-term gains to refill the short buckets. When it's down, you leave the growth stuff alone and live off the safe money.

David Blanchett from Morningstar calls this the "dynamic approach." It's not sexy, but it works.

2. The Guardrails Method

Start with 4% but adjust based on what's happening:

- If your portfolio's doing great, bump your withdrawal up to 5% or even 6%.

- If it's getting hammered, cut back to 3% or 3.5%.

Yeah, it means your income bounces around. But you're way less likely to go broke. This retirement withdrawal strategy requires flexibility but offers better long-term security.

3. The Bond Ladder (For the Cautious)

Buy individual bonds that mature when you need the money. Year one needs $40k? Buy a bond that pays exactly $40k in year one. Year two needs $41k? Different bond.

Boring as hell. Inflation's a pain. But you know exactly what you're getting.

4. The Part-Time Bridge

Work part-time for the first few years of retirement. Even $15,000 a year lets you pull way less from your portfolio during those crucial early years.

Rosa did this with consulting work. Kept her brain engaged, covered some expenses, and let her portfolio breathe during a rough market stretch.

| Strategy | Best For | Trade-off |

|---|---|---|

| Bucket Strategy | Most retirees — balanced approach | Requires periodic rebalancing |

| Guardrails | Flexible spenders | Income varies year to year |

| Bond Ladder | Risk-averse, predictability lovers | Inflation can erode purchasing power |

| Part-Time Bridge | Early retirees, high-CAPE markets | Requires willingness (and ability) to work |

What the Experts Actually Recommend for 2026

Morningstar's 2025 report: Start at 3.9% for a balanced portfolio, adjust as you go.

Bill Bengen's updated research: 4.7% works if you're flexible with small-cap value stocks and international bonds.

Wade Pfau (retirement researcher at American University): Forget withdrawal rates altogether. Build a floor with Social Security and annuities, then take more risk with what's left.

Our take: Start at 4%, be ready to adjust. Have 2-3 years of expenses in cash so you can ride out the inevitable rough patches without selling stocks when they're beaten up.

The Real Secret Nobody Talks About

Here's what I learned from talking to a dozen actual retirees: The ones who stress least about money aren't the ones with the biggest portfolios. They're the ones with the most flexibility.

They can cut spending when markets suck. They can pick up some work if they need to. They didn't lock themselves into a lifestyle that requires exactly $X every month no matter what.

The retirees who stress least about money aren't the richest. They're the most flexible.

The 4% rule assumes you'll spend the exact same amount (adjusted for inflation) every year for 30 years. That's not how real humans live.

Some years you'll travel more. Some years you'll stay home. Some years you'll be healthy. Some years... you won't. Build wiggle room into your plan.

Your Next Move

🎯 Your Retirement Withdrawal Game Plan

- Figure out your floor — what's the absolute minimum you need to cover basic expenses.

- Build 2-3 years of that in cash — so you never have to sell stocks at the worst time.

- Start at 4% of your remaining portfolio — not 4% of the whole thing.

- Stay flexible — be ready to spend more when markets are up, less when they're down.

- Consider working part-time initially — even a little income makes a huge difference in those critical early years.

The 4% rule was a good start. But 2026 isn't 1994. The market's more expensive, bonds pay less, and you're probably going to live longer than those original studies assumed.

Don't follow a 30-year-old formula blindly. Use it as a starting point, then adapt to reality.