Part-Time Retirement Jobs: The Healthcare Bridge That Saves $50,000+

I want you to sit with a number for a second: $95,000. That's roughly what a couple retiring at 62 could blow on health insurance premiums before Medicare shows up at 65. Three years. Ninety-five grand. Poof. Not on flights to Portugal, not on spoiling the grandkids, not on finally building that woodshop — just so you don't go bankrupt if your knee gives out or you need a colonoscopy.

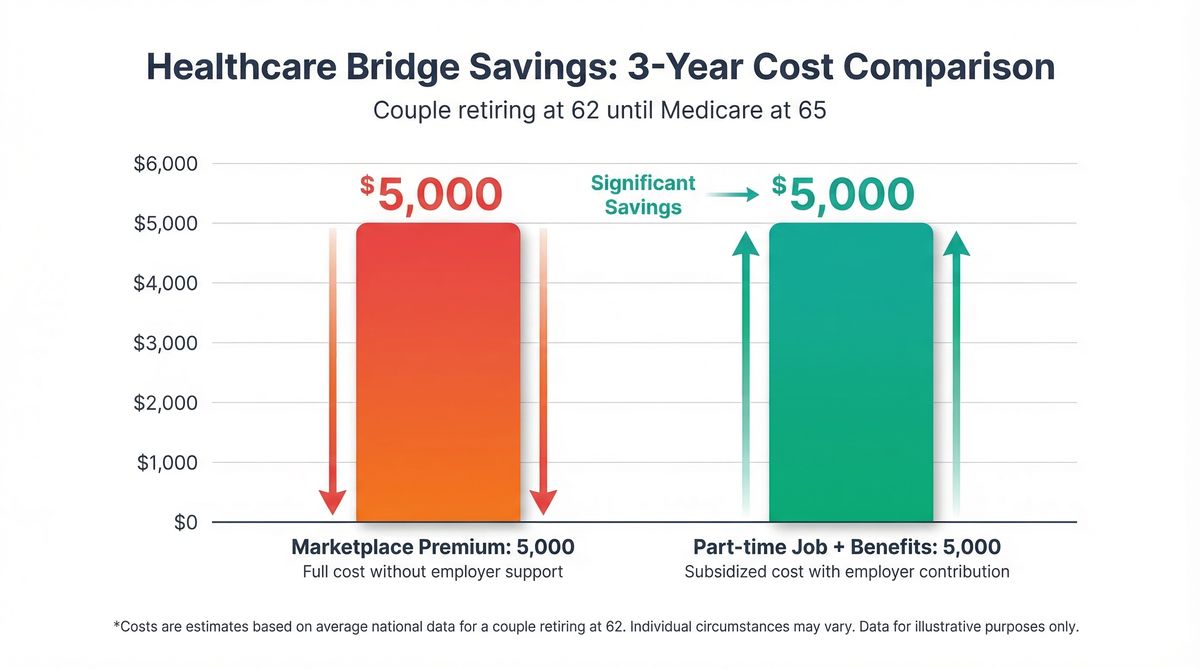

The 2026 healthcare cliff hit early retirees hard, but part-time jobs with benefits offer a smart solution:

- Save $50,000+ over three years compared to marketplace premiums

- Starbucks, Costco, UPS lead in part-time benefit offerings

- 20-23 hours/week typical minimum for coverage

- Strategy works best for ages 62-65 until Medicare kicks in

Action: Research part-time benefit options before your early retirement date to bridge the healthcare gap.

And as of 2026? That number ain't some worst-case scenario I pulled out of thin air. It's what people are actually paying for the early retirement healthcare gap.

Let me explain.

The 2026 Healthcare Cliff That Caught Early Retirees Off Guard

If you've been building your early retirement plan around those nice, affordable ACA marketplace premiums… I'm sorry. The game changed on January 1, 2026.

Those enhanced premium tax credits — the ones from the American Rescue Plan back in 2021, extended by the Inflation Reduction Act — they expired on December 31, 2025. Congress didn't renew them.

What Changed in 2026

Premium Tax Credit Cliff: Enhanced subsidies expired, causing marketplace premiums to more than double overnight for many early retirees. The average person saw a 114% increase in out-of-pocket costs.

The Kaiser Family Foundation ran the numbers, and the average person who'd been getting premium tax credits saw their out-of-pocket payments **more than double** overnight. We're talking a 114% increase if you kept the same plan. One hundred and fourteen percent. Just let that marinate.

For early retirees, it's even uglier. Here's the thing most people don't realize: the ACA lets insurers charge older adults up to *three times* more than younger folks. So you're already paying more just because you're closer to 60 than 30. Now stack the return of the "subsidy cliff" on top of that — where your premium help vanishes completely once your household income crosses 400% of the federal poverty level — and you've got what KFF politely calls a "double whammy."

I'd call it something else.

Here's what the early retirement healthcare gap actually looks like. A 60-year-old making $65,000 — just a hair above the subsidy cutoff — is now paying roughly **$10,400 more per year** in premiums than they were in 2025. The cheapest bronze plan for a 60-year-old averages about $11,625 nationally. Want a decent silver plan? That's $15,914. Got a spouse? Double it.

Here's where it gets really sneaky: it's not just wages that count toward that number. IRA withdrawals. 401(k) distributions. Capital gains. Dividends.

And — this one trips up a ton of people — **100% of your Social Security benefits** count toward MAGI, even though only a portion is taxable on your regular return. I've talked to folks who thought they were safely under the line until they realized a modest Roth conversion or one good year in their brokerage account pushed them right over the edge.

Meanwhile, the dream of employer-sponsored retiree health coverage? Pretty much dead. Only about 27% of large companies even offer coverage to pre-65 retirees anymore, and for smaller employers it's way less. COBRA? That'll run you $1,500 to $2,500 a month for a couple and it expires after 18 months anyway.

So picture this: you've been disciplined. You saved your stacks. You're finally ready to walk away from the cubicle or the Zoom calls or whatever your version of the grind looks like. And healthcare is about to eat your nest egg alive during the three most vulnerable years before Medicare.

Not exactly the retirement dream you had on your vision board.

But there's a solution that bridges this gap — and it comes with some side benefits that honestly surprised me when I started digging into it.

Part-Time Retirement Jobs: Your Healthcare Bridge Strategy

What if, instead of watching your portfolio bleed $24,000 to $32,000 a year on premiums, you just… worked 20 hours a week somewhere that gave you benefits?

I know. I know. "Ross, I didn't save all this money just to go back to work."

Hear me out. This isn't about *needing* to work. This is about being smart with the hand you've been dealt.

A bunch of major employers — names you know — offer legit medical, dental, and vision coverage to part-time workers. And I'm not talking about some garbage plan with a $10,000 deductible that only kicks in if you get hit by a bus. These are real working in retirement benefits where you might pay $100 to $300 per paycheck instead of $1,000 to $1,300 a month on the open market.

The $50,000 Savings Play

Work part-time for benefits and you could save $50,000 or more over a three-year retirement healthcare bridge to Medicare. Your portfolio stays intact — compounding away like it should be.

Do the math with me. Work part-time for benefits and you could save **$50,000 or more** over a three-year retirement healthcare bridge to Medicare. Your portfolio stays intact — compounding away like it should be. Your stress goes down. And oh yeah, you're also picking up a paycheck on top of it.

There's another angle most people miss: **income management.** If your part-time earnings and other income stay below that ACA cliff, you might actually qualify for subsidized marketplace coverage for a spouse who isn't working. That's a two-for-one play. But even without getting fancy with the subsidy math, employer coverage through a part-time gig almost always beats unsubsidized marketplace plans. It's not even close.

The FIRE community — those "Financial Independence, Retire Early" folks — they've got a name for this: "Barista FIRE." The idea is you save enough to leave your demanding career, then work part-time mostly for the health benefits and a little extra bread on the side. The name comes from Starbucks, probably the most famous company offering part-time health coverage. But the strategy goes way beyond pulling espresso shots.

Best Part-Time Retirement Jobs With Health Benefits

Here's the thing — not every employer that talks about "part-time benefits" actually delivers working in retirement benefits. Some require so many hours you're basically full-time with a different title. Others have waiting periods that'll leave you uninsured for months. We went through the fine print so you don't have to. Here's what's actually real for 2026:

Starbucks: The Gold Standard

- Minimum Hours 20/week

- Waiting Period 240 hrs over 3 months

- Coverage Medical, dental, vision

- Extras 401(k) match, stock equity

- Best For Predictable schedules

Costco: Premium Pay

- Minimum Hours 23/week

- Waiting Period 60 days

- Average Pay $22/hour

- Premium Cost 11-12% of total

- Best For Higher income needs

Starbucks: The Original Part-Time Retirement Job

Still the gold standard, and for good reason. Work at least **20 hours per week** and you get medical, dental, and vision. You need to log 240 hours over three consecutive months to become eligible, then keep up 520 hours per six-month audit period to stay covered. They throw in a 401(k) match, stock equity (they call it "Bean Stock" — I respect the branding), 20 therapy sessions a year, and free Headspace.

Yeah, the culture skews young. Yeah, the work is on your feet. But a lot of retirees actually dig the social side of it. My friend's mom worked at a Starbucks in Denver after she retired from teaching and said it was the best part of her week. Take that for what it's worth.

Best for: People who want a clear, well-documented path to benefits with a predictable schedule.

Costco: Premium Pay for Your Healthcare Bridge

You'll need to average about **23 hours per week**, and benefits kick in the first of the month after **60 days** of continuous work. The trade-off? The pay is legitimately good — average hourly rate around **$22/hour** as of 2025, with experienced employees pulling over $30. Part-timers pay roughly 11-12% of their healthcare premiums, which is wild when most big retailers charge 33-40%.

Oh, and time-and-a-half on Sundays. That's real money.

The catch: Everybody wants to work at Costco. Their turnover is crazy low, which means openings are hard to come by. If this is your play, apply early, be persistent, and don't get discouraged if it takes a minute.

Best for: People who want the best pay and don't mind the physical side of warehouse work.

UPS: Union Benefits for Part-Time Retirees

This one's interesting. UPS stands out because of **union benefits** through the Teamsters — and those benefits can cover a huge chunk of your premiums. Sometimes 100%. Let me say that again: *zero premium costs* for your retirement healthcare bridge. In 2026. That's basically a unicorn.

Part-time package handling jobs are pretty widely available, though the hours and physical demands depend on your location and role. The union contract also comes with pension benefits, which is another thing you almost never see anymore.

The catch: A lot of these positions are early morning or late evening shifts, and the work is repetitive and physical. If your back or knees are already talking to you, this probably isn't your move.

Best for: People who are still in solid shape and want to pay as close to zero for healthcare as possible.

Other Options Worth Exploring

Don't stop with this list. **Chipotle, Home Depot, and JPMorgan Chase** have all offered part-time benefits in some form, though the details shift around. **School districts and local government agencies** are a sleeper pick — they often provide benefits at lower hour thresholds than private companies. And if you've got a professional skill — writing, accounting, IT, whatever — some **consulting gigs through staffing firms** actually come with benefits packages.

Five Questions to Ask Before Committing

- What's the minimum hours per week to qualify for health benefits?

- How long is the waiting period before coverage starts?

- What's my out-of-pocket cost for individual and couple coverage?

- Does coverage extend to my spouse or partner?

- Is there a measurement period where you're tracking my hours — and what happens if I dip below the threshold?

Don't be shy about asking. These aren't gotcha questions. Any decent employer will answer them straight.

Making Your Part-Time Retirement Strategy Work

Look, nobody dreams about working part-time at 62 to get health insurance. I get it. But this is one of the smartest plays on the board for bridging the early retirement healthcare gap. You protect your nest egg, you stay active, you stay connected to people, and in three years when Medicare kicks in, you walk away with your portfolio intact and your sanity in one piece.

That's not settling. That's strategy.

🎯 Your Part-Time Healthcare Bridge Action Plan

- 3-6 months before retirement: Research part-time opportunities at employers with strong benefit packages. Apply early since good spots fill fast.

- Compare the math: Calculate 3-year premium costs for marketplace vs. part-time employer coverage. Include deductibles and out-of-pocket maximums.

- Plan your income: Structure part-time earnings to stay below ACA subsidy cliffs if you have a non-working spouse.

- Have a backup: Apply to 2-3 employers since some may have waiting lists or seasonal hiring patterns.

- Set a clear timeline: Know exactly when you'll transition from part-time work to Medicare at age 65.

Thanks for reading if you've made it this far. Peace! ✌️