Roth Conversion Strategy: When to Convert and How Much to Save on Taxes

The IRS is coming for your traditional IRA. A Roth conversion lets you defuse that tax time bomb on your terms — but mess it up, and you'll pay more than if you'd done nothing. Here's the real math.

- Convert strategically — fill your current tax bracket without jumping to the next one.

- Target low-income years — the gap between retirement and Social Security is the sweet spot.

- 2025–2028 is a golden window — the OBBBA senior deduction adds up to $12,000 in extra deductions for 65+ couples.

- Watch IRMAA cliffs — conversions can spike your Medicare premiums two years later.

- Spread it out — a 5–10 year plan beats dumping everything at once.

The bottom line: a well-planned Roth conversion can save tens of thousands in lifetime taxes. But you need a multi-year strategy, not a one-time move.

I'm gonna tell you something that bugs me about retirement planning: the IRS is coming for your traditional IRA. They're patient. They'll wait. But once those required minimum distributions hit at 73 (or 75 if you were born in 1960 or later), they decide how much you pull out — and how much you owe.

You lose the driver's seat.

If you've got $500K or more parked in a traditional IRA or an old 401(k), you're sitting on a tax time bomb. And I don't say that to scare you — I say it because I've watched people get blindsided by this over and over again.

A Roth conversion lets you defuse that bomb on your terms. But mess it up, and you'll actually pay more in taxes than if you'd done nothing. So let's dig into the real numbers — no hand-waving, no "it depends" garbage.

What Is a Roth Conversion and How Does It Work?

Real quick: a Roth conversion moves money from your traditional IRA (pre-tax) into a Roth IRA (after-tax). You pay income tax on whatever you move now, but everything in the Roth — including all the growth from here to eternity — is tax-free. Forever.

Key Rules at a Glance

No income limit. Unlike Roth IRA contributions, literally anyone can convert any amount. No take-backs. Since 2018, you can't undo a conversion — the Tax Cuts and Jobs Act killed that. December 31 deadline. Not April 15 like contributions. You gotta get it done by year-end.

- No RMDs on Roth IRAs. Your money grows tax-free and nobody can force you to take it out. That's huge.

- The 5-year rule is a thing. Each conversion starts its own 5-year clock. Withdraw converted amounts before 5 years and before 59½, and you might get slapped with a 10% penalty. It won't mess with tax-free earnings after 59½, but it's worth knowing if you're converting on the younger side.

How Much Should You Convert to a Roth IRA?

This is where most advice turns into mush. Everyone says "fill up your tax bracket" like it's some profound insight, but nobody bothers showing the actual math.

Let me fix that.

Step 1: Calculate Your Roth Conversion Room

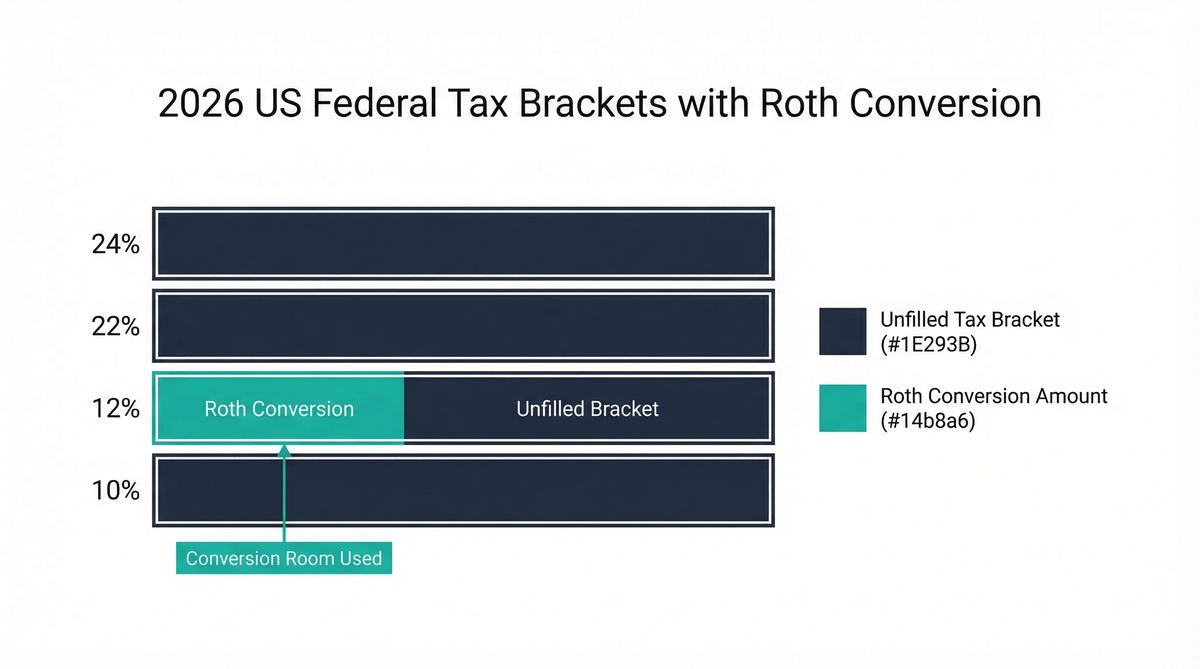

Your conversion room is just the gap between your current taxable income and the top of whatever tax bracket you're willing to fill up.

Here are the 2026 federal brackets for married filing jointly:

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | Up to $24,800 |

| 12% | $24,801 – $100,800 |

| 22% | $100,801 – $211,400 |

| 24% | $211,401 – $403,550 |

Standard deduction for 2026 is $32,200 for married couples. If you're both 65+, you also get the additional standard deduction ($1,650 each, $3,300 total) — plus a brand-new senior deduction from the One Big Beautiful Bill Act worth up to $6,000 per person. That one's temporary though. More on that gold mine in a minute.

Step 2: Do the Tax Impact Math

Take your gross income. Subtract your deductions. That's your taxable income. Now look at the brackets and see how much room you've got before you hit the next tier.

Let me show you what this looks like with actual humans.

When to Do a Roth Conversion: The Early Retiree Gap Years

Dave and Linda. Both 60, just retired. They've got $800K in traditional IRAs and pull about $30K a year in dividends and interest from their taxable accounts. No Social Security yet. No pension.

Their taxable income: $30,000 minus $32,200 (standard deduction) = basically zero. Zilch.

Now look at that bracket table again. They could convert up to $100,800 and stay entirely in the 12% bracket. But they're smart, so they target $70K a year — leaving room for any surprises.

Dave & Linda's Conversion Math

Convert $70K/year for 5 years = $350,000 moved to Roth. Total tax: ~$40,000. If that money came out later through RMDs at 22–24%, they'd owe $77K–$84K. That's $37,000–$44,000 in savings — before counting tax-free Roth growth.

Those "gap years" between retirement and Social Security are the single best window for Roth conversions. Your income's at rock bottom, which means your tax rate is too.

Roth Conversion Strategy Using the OBBBA Senior Deduction (2025–2028)

Here's something that flew under a lot of people's radar: the One Big Beautiful Bill Act created a new deduction for folks 65 and older — up to $6,000 per person, or $12,000 for a married couple. It's available from 2025 through 2028, then it's gone.

Stack that on top of the regular standard deduction and the existing senior deduction, and a 65+ couple can deduct up to $47,500 in 2026 ($32,200 standard + $3,300 existing senior + $12,000 OBBBA senior). That's a massive runway for cheap Roth conversions.

Phase-Out Warning

The $6,000-per-person OBBBA senior deduction phases out if your modified adjusted gross income tops $150,000 as a couple ($75K single). You lose 6% of every dollar above that threshold. A couple at $200K in MAGI would lose $3,000 of the deduction. Factor that into your math.

Tom and Carol. Both 66, married. They've got $500K in traditional IRAs and collect $40K a year combined from Social Security. After accounting for the taxable portion of their Social Security and their beefed-up deductions, their taxable income barely registers.

Their financial planner found room to convert about $50K a year while keeping their tax rate low and staying under the IRMAA thresholds. Over three years — 2026 through 2028 — that's $150,000 shifted to Roth while the enhanced deduction exists.

After 2028? That senior deduction expires, and the same conversions cost a lot more. This window is closing.

Roth Conversion Tax Impact on Medicare: The IRMAA Trap

OK, this is where people get burned. Your Roth conversion doesn't just hit your income tax — it can jack up your Medicare premiums through something called IRMAA (Income-Related Monthly Adjustment Amount).

Here's the fun part: Medicare uses your income from two years ago to set your premiums. So a fat conversion in 2026 could mean higher premiums in 2028. Surprise!

And it's not gradual. It's a cliff. Go one dollar over a threshold and you pay the higher premium for the whole year.

| Your MAGI (MFJ) | Monthly Part B Premium (per person) |

|---|---|

| Up to ~$218,000 | ~$190 (standard) |

| ~$218,001 – $273,000 | ~$267 |

| ~$273,001 – $343,000 | ~$381 |

| ~$343,001 – $411,000 | ~$494 |

For a couple, tripping that first cliff means roughly $1,850 a year in extra Medicare premiums. Hit the third tier and you're looking at over $4,600 a year extra. That's real money.

Navigating IRMAA With Your Roth Conversion Strategy

Karen. She's 68, single, on Medicare. Her pension and Social Security add up to $95K a year. She's sitting on $1.2 million in her traditional IRA and wants to start converting.

The single filer IRMAA threshold is roughly $109,000. Karen's only got about $14K of conversion room before she triggers higher Medicare premiums.

But here's where it gets interesting. If she accepts the first IRMAA tier bump, she could convert up to roughly $37,000. That means paying about $900 a year in additional Medicare premiums.

The IRMAA Trade-Off

Karen's $37,000, invested for 20 years at 7% growth, becomes roughly $143,000 — all tax-free in the Roth. Paying $900 to help create $143,000 in tax-free wealth? That's a trade worth taking.

Roth Conversion During a Market Downturn: The Tax Discount Trick

This one's sneaky — in a good way.

Say you've got $100,000 in stock index funds in your traditional IRA, and the market drops 25%. Those shares are now worth $75,000. If you convert them in-kind (just transfer the shares directly to your Roth without selling), you pay tax on $75,000 instead of $100,000.

Convert During Downturn

- Account Value $75,000

- Tax at 22% $16,500

- Recovery Growth Tax-Free

- Effective Cost $16,500

Convert at Full Value

- Account Value $100,000

- Tax at 22% $22,000

- Recovery Growth Tax-Free

- Effective Cost $22,000

You're basically buying future tax-free growth at a discount. Market crashes stink, but they can also be an opportunity if you're paying attention.

Roth Conversion Strategy for Beneficiaries and Inheritance

This one hits close to home for a lot of families.

Under the SECURE Act's 10-year rule, most non-spouse beneficiaries who inherit a traditional IRA have to drain it within 10 years. If your kids are in their peak earning years, they could be paying 32% or more on those forced distributions. Ouch.

With Roth Conversion

- IRA Balance $600,000

- Parents' Tax Rate 12%

- Convert $60K/yr × 10 yrs $72,000 tax

- Family Tax Savings $120,000

Without Conversion

- IRA Balance $600,000

- Kids' Tax Rate 32%

- Forced Distributions $192,000 tax

- Lost to Taxes $192,000

That's $120,000 that stays in your family instead of going to Uncle Sam. And all the future growth in the Roth is tax-free for your kids too.

The Widow's Tax Torpedo: Why Couples Should Convert Sooner

Here's one that almost nobody talks about, and it's brutal.

A married couple filing jointly might have combined income that fits comfortably in the 12% bracket. Life's good. But when one spouse passes away, the survivor files as single — and that same income suddenly lands in the 22% bracket or higher.

RMDs don't shrink just because one spouse died. Social Security might drop a little, but the tax brackets shrink way faster.

Proactive Roth conversions while both spouses are alive can protect the surviving spouse from a devastating tax cliff. It's one of the strongest arguments for converting sooner rather than later.

Common Roth Conversion Mistakes to Avoid

Converting everything at once. I've seen people convert their entire IRA in one year and catapult themselves into the 32% or 37% bracket. Spread it over 5–10 years and you might stay at 12%. The difference is insane.

Paying the tax from your IRA. If you convert $50,000 and pull $12,000 out of the IRA to cover the taxes, you've only actually moved $38,000 to the Roth — and if you're under 59½, that $12,000 gets whacked with a 10% penalty too. Pay the taxes from your checking or brokerage account.

Forgetting the pro-rata rule. If you've got both pre-tax and after-tax (nondeductible) money in your traditional IRA, you can't just cherry-pick the after-tax portion. The IRS treats all your traditional IRA money as one big pool. Each conversion is a proportional mix of taxable and nontaxable dollars.

Forgetting about state taxes. Federal brackets aren't the whole story. If you live in California, that conversion gets taxed at your state rate too. Planning to move to a no-income-tax state like Nevada or Texas? Do the conversion after you move.

Blowing the December 31 deadline. Don't wait until the last week. Brokerage transfers can take days to settle. Aim to wrap up your conversion by mid-December.

Skipping your RMD. If you're already at RMD age, you must take your required distribution for the year before you convert anything. The RMD itself can't be converted. Get that done first.

How to Build Your Own Roth Conversion Plan

🎯 Your 8-Step Roth Conversion Roadmap

- Add up your baseline income — Social Security, pensions, rental income, dividends, whatever side gig you're doing.

- Subtract your deductions — Standard deduction, plus the additional and OBBBA senior deductions if you qualify.

- Find your current taxable income — That's your starting line.

- Pick your target bracket — Most people aim for the top of the 12% or 22% bracket.

- Check IRMAA thresholds — If you're on Medicare or within two years of it, pay attention here.

- Watch the senior deduction phase-out — If your conversion pushes MAGI above $150K (married), you start losing that OBBBA deduction.

- Calculate the gap — That's your conversion room.

- Map it out for 5–10 years — Your income changes as Social Security kicks in and RMDs start. Plan across multiple years, not just one.

Grab a spreadsheet. Make columns for each year — income sources, conversion amount, tax bracket, IRMAA tier. It's not glamorous, but a simple roadmap beats guessing every single time.

The Bottom Line on Roth Conversion Strategy

A Roth conversion isn't a one-and-done thing. It's a multi-year play that can save you tens — or even hundreds — of thousands of dollars in lifetime taxes. But you gotta plan it out, not just wing it.

The people who win here are the ones who convert strategically: during low-income years, within the right brackets, while keeping an eye on IRMAA, and spreading it over multiple years instead of dumping it all at once.

And right now — especially between 2026 and 2028 — there's a window that might not come around again, thanks to that temporary OBBBA senior deduction. If you're within a few years of retirement or already retired, this is worth carving out a Saturday afternoon for.

Over at Ready Aim Retire, we're building retirement planning tools and guides to help you run these numbers yourself — because understanding the math behind your retirement plan matters way more than any single product or calculator somebody's trying to sell you.

Start with the basics. Run the numbers for your situation. And whatever you do, don't let December 31 sneak up on you.

Peace!