What $1 Million Actually Buys in Retirement (2026 Reality Check)

Everyone's throwing around the million-dollar retirement number like it's the universal truth. Hit seven figures in your 401(k) and retirement paradise, right? Let's talk about what that money actually looks like in 2026.

- A $1M portfolio generates roughly $35,000/year using a conservative 3.5% withdrawal rate - about $2,917/month before taxes.

- After taxes and healthcare costs, you're looking at roughly $1,540/month from your portfolio alone.

- Social Security helps, but a truly "comfortable" retirement starts at around $1.4 million in 2026.

- Long-term care costs ($120K–$140K/year) can wipe out a third of your savings in just a few years.

Bottom line: $1 million is real money, but it buys the bare-bones retirement package — not financial freedom.

The 4% Rule Is Getting Crushed

Here's the classic advice: take 4% out of your portfolio every year and you'll never run out of money. Sounds neat and tidy, right? Your million becomes $40K a year. About $3,300 a month.

But there are two massive problems with this approach.

First, the 4% rule was built for 30-year retirements. That worked when people retired at 65 and died at 75. But if you retire at 62 and live to 95 (which is becoming pretty normal), you need that money to stretch for 33 years. And that changes everything.

The 4% Rule - Updated

Most financial planners now recommend a 3% to 3.5% withdrawal rate to account for longer lifespans. That brings your million down to $35,000 a year — $2,917 a month, before taxes and healthcare.

And here's the second gut punch: $40K in 2026 doesn't buy what $40K bought when your parents retired. What cost you a dollar in 2006 now costs about $1.60. So your million today has the purchasing power of about $700K from 20 years ago.

The retirement income from $1 million? It's not looking so magical anymore.

Where Your Money Actually Goes

Let me walk you through what happens to that $35K when it meets reality.

Taxes Will Take Their Cut First

If your money's sitting in a traditional 401(k) or IRA (which is probably where most of it is), Uncle Sam gets his cut of every dollar you withdraw. Add in your Social Security benefits — which also get taxed — and you could easily hit that 22% bracket.

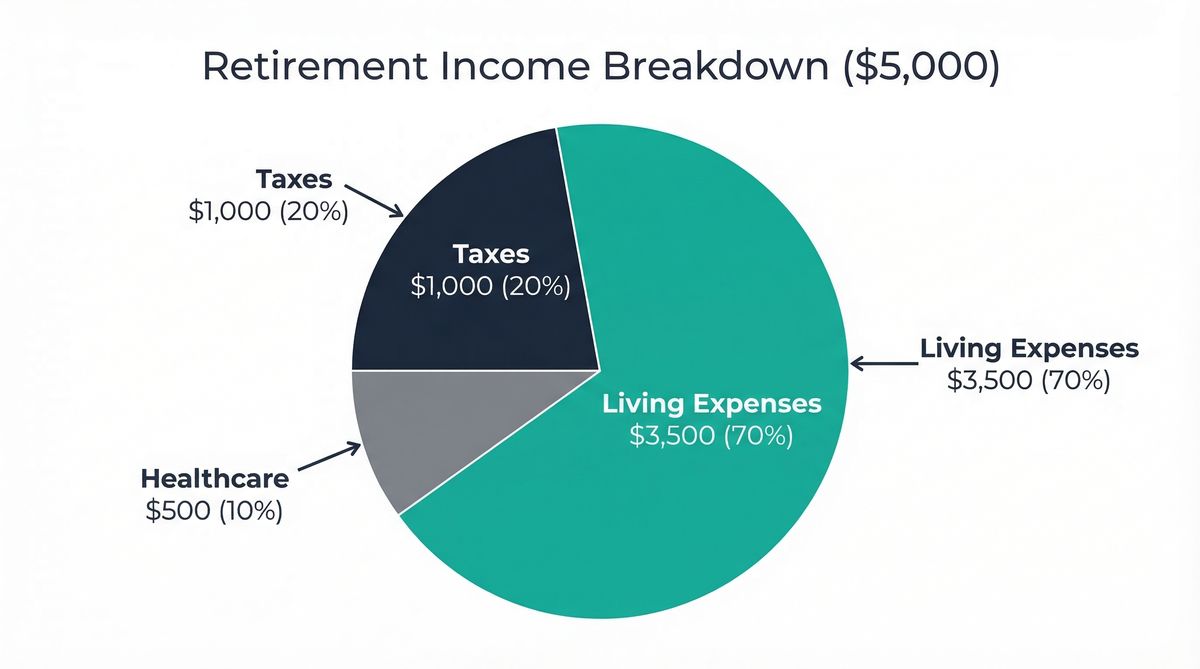

So you're pulling $35K from your retirement account, getting about $29K from Social Security, and paying roughly $8K–$10K in taxes depending on your state. Your $35K just became $25K–$27K.

Healthcare Costs Are On The Rise

This is the one that blindsides everyone. Medicare isn't free. Not even close.

For a single person, healthcare alone costs about $8,400 per year. For a couple, that's $16,800 annually just to not die from treatable illnesses.

The Real Math on $35K

After taxes (~$8K) and healthcare for one person (~$8,500), you've got about $18,500 left for everything else. That's $1,540 a month — total.

Social Security helps — the average person gets about $2,400/month. But even with that safety net, you're budgeting. Hard.

Real-World Examples: What This Actually Looks Like

These are real scenarios, not some made-up financial planning fantasy.

Maria in Phoenix: The Single Retiree

Maria's got her million split between a 401(k), some Roth money, and taxable accounts. Social Security sends her $2,400 a month.

Maria's Income

- Portfolio Withdrawals $35,000/yr

- Social Security $28,800/yr

- Total Income $63,800/yr

After Deductions

- Taxes −$11,500

- Healthcare −$8,500

- Spendable $43,800/yr

In Phoenix with a paid-off house, she's making it work — property taxes, groceries, keeping her 2018 Honda running, and hitting her favorite restuarant maybe once a month. But there's zero margin for error. Her transmission goes out? That's her vacation fund and then some.

The verdict: Okay, but one surprise expense away from stress.

Tom & Linda in Denver: The Comfortable Couple

They've got their million combined, plus a $400K house that's paid for. Combined Social Security brings in $4,200/month.

Annual income: $85,400 ($35K withdrawals + $50,400 Social Security). After taxes and healthcare: About $55,400 left, or $4,617/month.

Denver's expensive — about 30% higher than the national average. They can eat out a few times a month, maybe take a road trip to Yellowstone. But help the grandkids with college? That European river cruise Linda's always wanted? Those conversations become very serious.

The verdict: Comfortable, but every big decision is a negotiation.

James: The Early Retiree Who Did the Math Wrong

James hit his million at 55 and thought he was done. No more cubicle, no more boss, no more alarm clock. Problem: no Social Security for at least 7 more years.

Annual income: $30,000 from portfolio withdrawals. After buying health insurance on the marketplace and paying taxes, maybe $8K–$12K left for actual living. That's $670–$1,000 a month for everything.

The verdict: A million isn't enough to retire at 55. Period.

The Hidden Costs Nobody Talks About

Here's what really messes people up: they think retirement is a destination. Like you hit the number, stop working, and coast for 20 years. But retirement is 20–30 years of real life. And life gets more expensive as you age.

Healthcare costs go up 4–6% every year — double the rate of everything else. That $12K healthcare bill today becomes $20K in 10 years and $30K in 20.

Two or three years of serious long-term care can wipe out a third of your million. That's the stuff that turns a "we're fine" retirement into a crisis.

Nursing homes are running $120K–$140K a year now. Home health aides cost $35/hour. Three years of care? That's $360K, gone.

The Real Numbers for 2026

It depends on where you want to live, how you want to live, and how long you're going to live. But here are some honest numbers:

| Retirement Level | Annual Spending | Portfolio Needed | What It Looks Like |

|---|---|---|---|

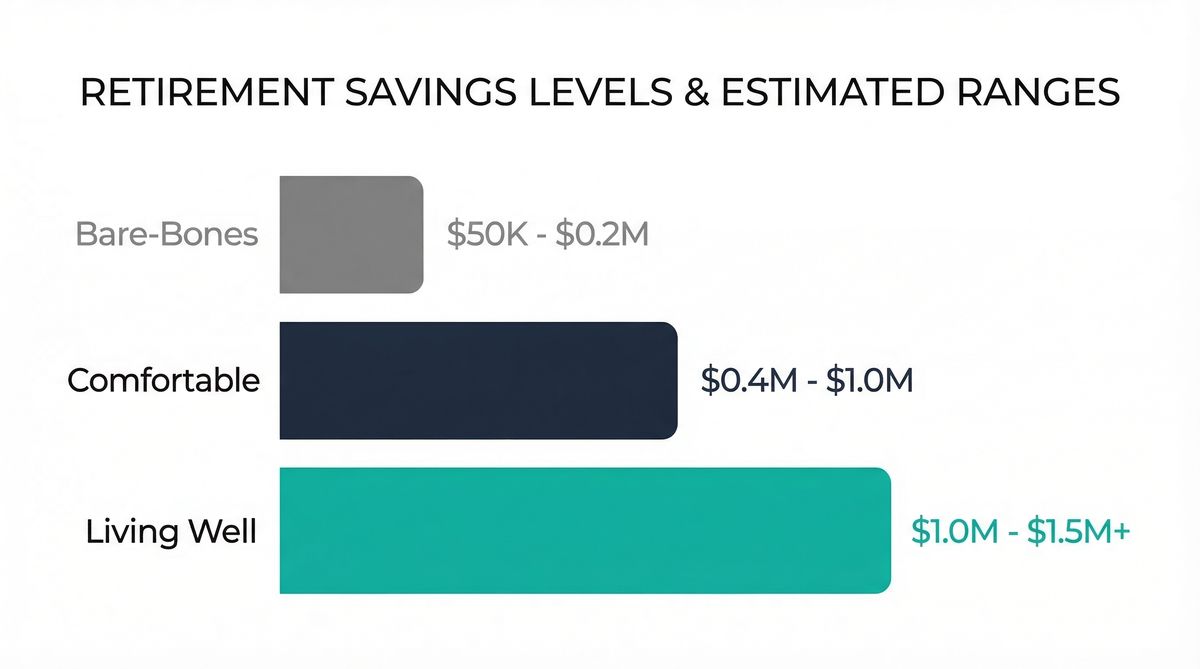

| Bare-Bones | $30K–$40K | $850K–$1.2M | Paid-off house, low-cost area, careful budgeting |

| Comfortable | $50K–$75K | $1.4M–$2.1M | Travel, hobbies, helping the kids, flexibility |

| Living Well | $75K–$120K+ | $2.1M–$3.5M+ | Multiple trips, second home, premium everything |

See what happened there? "Comfortable" starts at $1.4 million. Your million-dollar retirement gets you the bare-bones package in most of America.

And you know what? That's not necessarily bad. Some of the happiest retirees I know are living on less than you'd expect. But they went in with their eyes open.

Strategies That Actually Move the Needle

If you're reading this and feeling that pit in your stomach, take a breath. Here's what actually works:

🎯 Your Retirement Action Plan

- Diversify your tax buckets. Stop putting everything in traditional 401(k)s. Build Roth money. Do Roth conversions. Tax-free withdrawals in retirement are like getting a 20–25% raise.

- Get real about geography. This is the biggest lever you have. The same million supports a completely different lifestyle in Asheville vs. San Jose. If you're flexible, you can upgrade your entire retirement.

- Plan for long-term care now. Nobody wants to think about it, but having a plan — insurance, savings, family help — keeps one bad health year from destroying 30 years of saving.

- Build multiple income streams. Social Security, part-time work, rental income, a small pension — the people who retire well usually have several sources coming in.

- Run your actual numbers. Stop relying on rules of thumb. Use calculators that account for your real expenses, location, health, and inflation.

The Bottom Line

A million dollars is still a lot of money. Most people would love to have that problem. And with smart planning, it can absolutely fund a good retirement.

But it's not the magic bullet everyone thinks it is. In 2026, after inflation has been chipping away at buying power and healthcare costs have gone bananas, a million-dollar retirement looks more like "careful budgeting" than "financial freedom."

The question isn't whether you hit some arbitrary number. It's whether your plan matches your actual expenses — in your real city, with your real health situation, over 20–30 years of inflation and surprises.

That's what we focus on at Ready Aim Retire. Not bumper sticker wisdom, but actual plans for actual people. Because your retirement is too important for generic advice from a magazine article.

Want to know where you really stand? Stop guessing and start calculating.