When Should You Claim Social Security? The Complete 2026 Guide to Age 62 vs 67 vs 70

Back in 2008, the Social Security Administration quietly pulled its own break-even calculator off the website. Turns out people were using it to basically bet against their own lifespan, treating one of the biggest financial decisions they'd ever make like a coin flip. Nearly two decades later, the question of when to claim Social Security has only gotten more complex.

- Claim at 62: If you have serious health issues limiting life expectancy or desperately need income now

- Claim at 67 (FRA): The "default" choice—your full earned benefit with no reductions or bonuses

- Claim at 70: For those in good health with other income sources—generates 77% more monthly income than claiming at 62

- Break-even point: Around age 80-81 for 62 vs 70 comparison, but longevity insurance value extends far beyond break-even math

- Married couples: Higher earner should usually delay to maximize survivor benefits

You've got viral social media posts and financial news segments warning that the math most people rely on is dangerously incomplete. And honestly? They're not wrong.

The difference between claiming Social Security at 62 and waiting until 70 is a 77% larger monthly check. For the average worker, that gap adds up to hundreds of thousands of dollars over a lifetime. And in 2025, fear-driven headlines about agency cuts and office closures pushed hundreds of thousands of additional Americans to file early. Financial researchers say that surge is going to cost a lot of those folks dearly.

So when should you actually claim Social Security? The answer depends on way more than a spreadsheet. Let's walk through it.

Social Security Benefits at 62 vs 67 vs 70: What You'll Actually Get

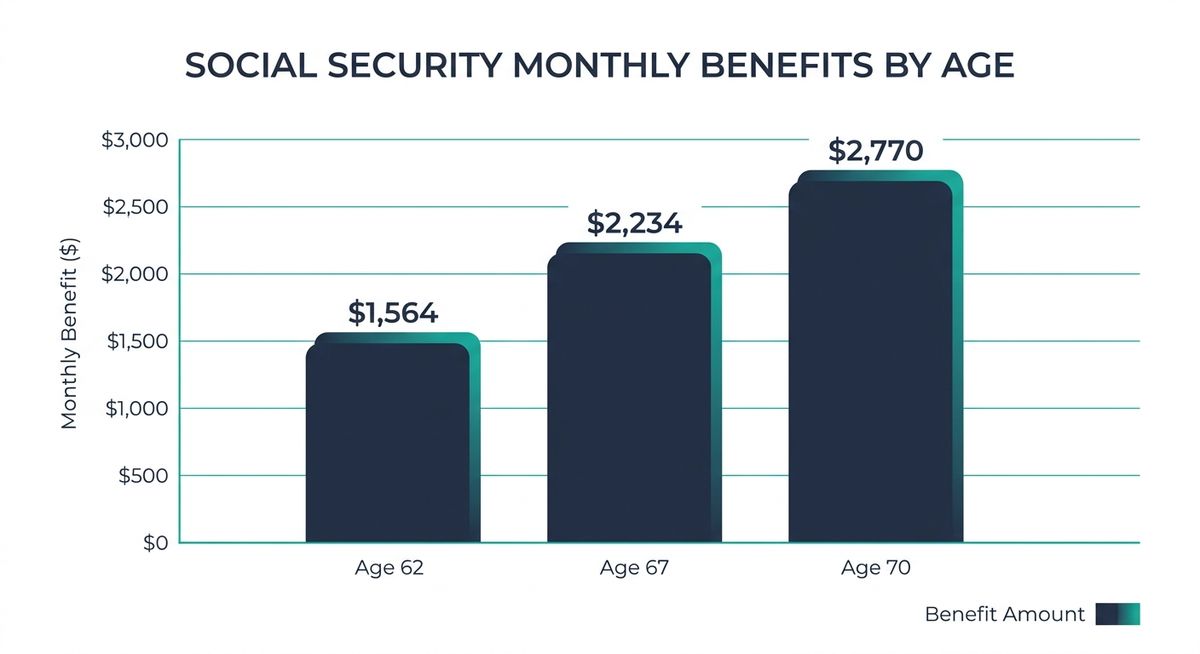

Let's start with the 2026 numbers, because most articles floating around are still citing outdated figures.

If your full retirement age (FRA) benefit is $2,234 per month (the current average for men), here's what claiming at each age looks like:

| Claiming Age | Your Monthly Benefit | What That Means |

|---|---|---|

| 62 | $1,564 | 30% permanent reduction |

| 67 (FRA) | $2,234 | 100% of your earned benefit |

| 70 | $2,770 | 24% bonus above full benefit |

For women, whose average FRA benefit is $1,802, the pattern looks the same but the stakes are arguably higher. Women live longer on average, collect benefits for more years, and are more likely to depend on survivor benefits after a spouse dies.

The Maximum Benefit Story

The maximum possible benefit tells an even bigger story: $2,969 at 62 versus $5,181 at 70. That's an extra $2,212 every single month. For life. Adjusted for inflation.

Before your FRA, every month you delay reclaims a portion of the early-filing reduction. After your FRA, your benefit grows by exactly 8% per year until 70. After 70, there's no additional increase, so waiting beyond that age doesn't do you any good.

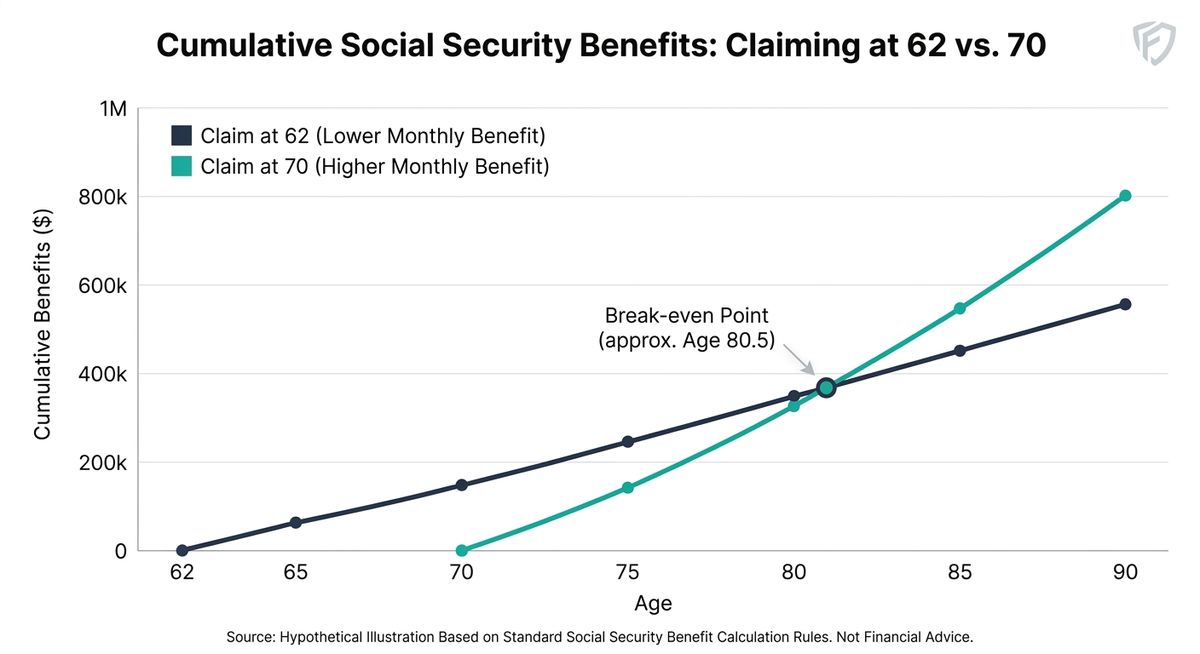

The Social Security Break Even Analysis (and Why It's Only Half the Story)

The break-even calculation is straightforward. If you claim early, you get smaller checks for more years. If you delay Social Security, you get larger checks for fewer years. At some point, the total dollars received by the person who waited catches up to the early claimer.

Here's a concrete example. Say your FRA benefit is $2,500 per month:

Claim at 62

- Monthly Benefit $1,750

- Total by age 80 $378,000

Claim at 70

- Monthly Benefit $3,100

- Total by age 80 $372,000

The break-even point lands right around age 80 to 81. Live longer than that, and delaying wins. Die before that, and claiming early was the better financial move.

For the 62 versus 67 comparison, break-even hits around age 78 to 79. For 67 versus 70, it's roughly 82 to 83.

What Break-Even Analysis Misses

These numbers are real, and they matter. But here's what the Social Security break even calculation leaves out: COLA compounding (your larger base benefit grows faster with inflation adjustments), the tax implications of higher income in retirement, spousal and survivor benefit impacts, and the insurance value of guaranteed income you can't outlive.

The SSA didn't remove its calculator because the math was wrong. They removed it because retirement calculators often miss critical variables, and people were making permanent decisions based on partial information. Tools like ReadyAimRetire can help you model these scenarios with your own numbers, including how Social Security timing affects your overall retirement plan.

Five Factors That Break-Even Analysis Misses

1. You're Probably Going to Live Longer Than You Think

More than one in three 65-year-olds today will live past 90. If that sounds surprising, you're not alone. Studies show most people underestimate their own life expectancy by five to seven years.

"My friend Karen in California turned 89 last year. She tells me all the time she never expected to make it past 80. Her mom said the same thing and lived to 94. We're all pretty bad at predicting this stuff."

Social Security is the only retirement income stream that's guaranteed for life and adjusted for inflation. That makes it longevity insurance, not a bet on when you'll die. The longer you live, the more valuable a higher monthly benefit becomes. And unlike your 401(k), you literally cannot outlive it. That's a big deal.

2. Your Spouse's Future Depends on Your Claiming Decision

This one gets overlooked constantly, and it shouldn't.

When a married person dies, the surviving spouse receives the higher of the two Social Security benefits. Not both. The higher one.

Critical for Married Couples

If the higher-earning spouse claims at 62, they've permanently capped the survivor benefit their widow or widower will live on. Potentially for decades.

Consider David, with a $3,200 FRA benefit. If he claims at 62 ($2,240/month) and dies at 82, his wife Linda receives $2,240 for the rest of her life. If he waits until 70 ($3,968/month) and dies at 82, Linda receives $3,968 per month. If Linda lives to 92, that difference totals over $207,000.

For married couples, the higher earner's claiming decision is really a decision about two lifetimes. Not one.

3. The Tax Torpedo Nobody Warns You About

Here's a scenario that catches retirees completely off guard. You're 72, taking required minimum distributions that many retirees handle incorrectly from your IRA, collecting Social Security, and maybe receiving a small pension. Each income source seems modest on its own. But combined, they push your "provisional income" past $34,000 (single) or $44,000 (married filing jointly), triggering taxes on up to 85% of your Social Security benefits.

I know. It's a lot to keep track of.

A higher Social Security benefit from delaying can actually increase your tax burden in certain income ranges. On the flip side, claiming early and drawing down retirement accounts sooner might create a lower-tax window during your 60s. There's no universal answer here, but ignoring the tax interaction is a mistake. This is where a few hours with a tax-savvy financial planner pays for itself many times over.

And it doesn't stop at income taxes, either. Higher combined income can trigger IRMAA surcharges on your Medicare premiums, based on income from two years prior. The connection between Social Security timing and Medicare costs is real, and almost nobody talks about it.

4. The Earnings Test Isn't What You Think

If you claim at 62 while still working and earn more than $24,480 in 2026, Social Security withholds $1 for every $2 you earn above that limit. A lot of people see this as a penalty. Or worse, money lost forever.

It's neither. When you reach your full retirement age, the SSA recalculates your benefit to credit you for every dollar that was withheld. Your monthly check goes up permanently.

The Earnings Test Catch

While your withheld months get credited back at FRA, you've still locked in the early-claiming reduction. You're getting a slightly higher version of a permanently reduced benefit. If you're still earning substantial income at 62, claiming early is almost always a losing move. For many pre-retirees, a part-time retirement bridge strategy makes more financial sense.

5. The "Claim Early and Invest" Strategy Has a Wealth Requirement

You've probably seen this argument floating around: claim at 62, invest the money in stocks, and come out ahead. Vanguard ran simulations on this strategy and found that it can produce slightly higher median wealth. But primarily for investors with very large portfolios who can absorb sustained market downturns without running out of money.

For the vast majority of Americans without that kind of cushion, this strategy is risky. A market downturn in your early 60s (sequence-of-returns risk) can devastate a portfolio you're simultaneously drawing down. Meanwhile, the 8% guaranteed annual increase from delaying Social Security past your FRA is a return that no market investment can match for certainty.

"That 8% guaranteed return. I keep coming back to it. Where else are you going to find that?"

Real People, Real Decisions

Let me walk through a few scenarios because I think they make the picture a lot clearer than abstract math.

Maria, 61, Single

- Health Good

- Savings $400K

- FRA Benefit $2,000

- Decision Wait until 70

Why: Her mother lived to 91. If Maria lives to 90, delaying nets her roughly $125,000 more in lifetime benefits. She has savings to bridge the gap.

Tom, 62, Health Issues

- Health Poor

- Life Expectancy ~75

- FRA Benefit $1,800

- Decision Claim now

Why: He'd collect approximately $197,000 over 13 years. Waiting to 67 would require living past 79 just to break even.

Janet, 62, Still Working

- Earnings $65,000/year

- FRA Benefit $2,200

- Decision Wait until 70

Why: The earnings test would withhold nearly all her benefits, and she'd lock in a permanent 30% reduction for checks she's barely receiving.

David & Linda, Married

- David's FRA $3,200

- Linda's FRA $1,800

- Strategy Split approach

Why: Linda claims at 62 ($1,260), David delays to 70 ($3,968). Maximizes survivor benefit worth over $200,000 compared to both claiming early.

Model Your Own Scenario

Every retirement situation is unique, and what works for Maria might not work for Tom or Janet. You can explore how these different claiming strategies work with your specific numbers and timeline at ReadyAimRetire.com.

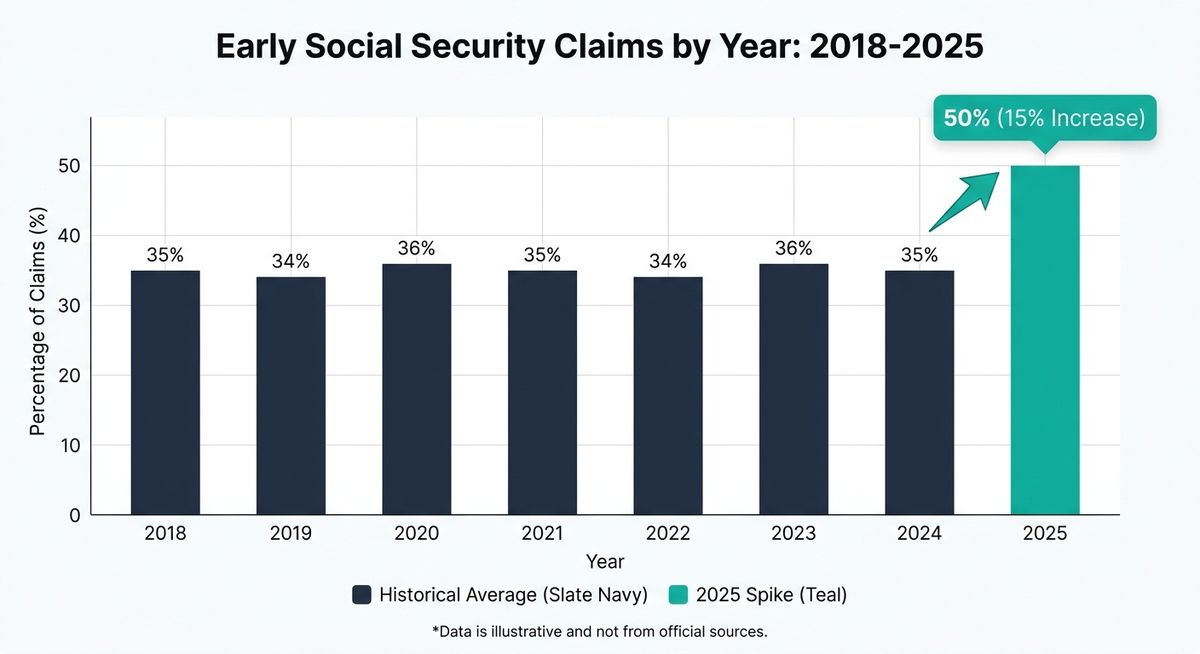

The Fear Factor: Why Hundreds of Thousands Filed Early in 2025

In fiscal year 2025, early Social Security claims surged by 15%. That's roughly five times the 12-year average growth rate. The cause wasn't a recession or a policy change. It was fear.

Headlines about SSA workforce cuts (roughly 12% of staff), regional office consolidations, and political rhetoric about the program's future convinced hundreds of thousands of Americans to grab their benefits before they "disappeared."

The Power of Framing

Researchers at Boston College's Center for Retirement Research found that participants shown "insolvency" headlines planned to claim a full year earlier than those shown neutral language describing the exact same funding shortfall. Same facts, different framing, completely different decisions.

Here's the reality. Even if the trust fund is depleted around 2034 as projected, ongoing payroll taxes would still fund about 81% of promised benefits. Social Security doesn't go to zero. It faces a funding gap that Congress has every political incentive to close, given that virtually every voter over 50 cares about this issue. And I mean every single one.

Filing early because you're worried the program might change is one of the most expensive financial mistakes a pre-retiree can make. A 62-year-old who claims five years early out of fear could forfeit $100,000 or more in lifetime benefits. That's a lot of money to leave on the table because of a headline.

A Changed Rule Worth Checking

If you worked in government or for an employer that didn't withhold Social Security taxes, pay attention. This part matters for you.

Social Security Fairness Act Update

The Social Security Fairness Act, signed January 5, 2025, repealed both the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO). More than 3.2 million people are affected, with retroactive lump-sum payments already going out. Those previously reduced by WEP are seeing average increases of about $360 per month, while those affected by GPO may see even larger adjustments.

If this applies to you, your entire claiming strategy may need revisiting. Contact the SSA or use your my Social Security account to see your updated benefit estimate.

Your Next Move: When to Claim Social Security

Forget the break-even calculator. Seriously. Instead, answer these questions honestly:

Five Questions to Guide Your Claiming Decision

- How's your health? If your family tends to live into their late 80s and 90s, delaying is almost always worth it. If you have a serious health condition that limits your life expectancy, claiming early makes sense. No judgment either way.

- Are you married? If so, coordinate. The higher earner should almost always delay as long as possible to protect the survivor benefit. This is one of those conversations that's worth having over a quiet dinner.

- Are you still working? If you earn more than $24,480 at age 62, the earnings test makes early claiming nearly pointless.

- Can you bridge the gap? If you have savings, a pension, or other income to cover expenses from 62 to 70, you're buying yourself an 8%-per-year guaranteed raise on income that lasts for life. That's a pretty great deal.

- Are you making this decision out of fear? If headlines about Social Security's future are driving your timeline, step back. The program isn't going away, and a permanent benefit reduction based on temporary anxiety is a trade you'll likely regret.

Create your free my Social Security account at ssa.gov to see your personalized benefit estimates at every claiming age. Then sit down with a fee-only financial planner who can model your specific situation, including taxes, Medicare premiums, spousal benefits, and portfolio longevity. Or start by running your own projections at ReadyAimRetire to see how different claiming ages affect your overall retirement plan. This single planning session could be worth tens of thousands of dollars over your retirement. I really believe that.

The Social Security claiming decision is permanent. Make it with a complete picture, not just a break-even spreadsheet.

Thanks for reading!