The Silent Retirement Killer: How Bad Market Timing in Your First 5 Years Can Destroy 30 Years of Savings

Two retirees. Same portfolio. Same withdrawal rate. Completely different outcomes. Here's the risk nobody talks about enough — and how to make sure it doesn't wreck your retirement.

- Sequence of returns risk means bad market returns in your first 5 years of retirement can destroy your portfolio — even if long-term averages are fine.

- The "fragile decade" (5 years before through 10 years after retirement) is when your portfolio is most vulnerable.

- Going ultra-conservative actually increases your risk of running out of money.

- Seven strategies — from cash buffers to guardrail withdrawals — can protect you.

Bottom line: Build flexibility into your plan before you need it. Hope isn't a strategy.

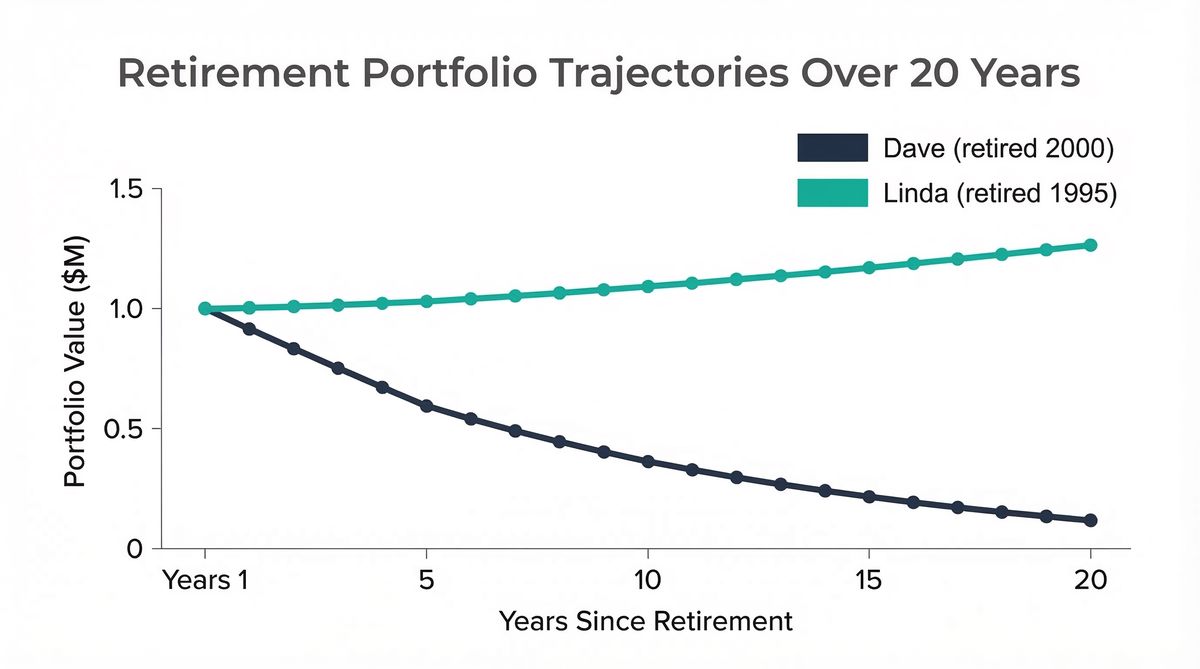

Let me tell you about Dave and Linda.

Both retired with exactly $1 million. Both planned to pull out $40,000 per year (classic 4% rule). Both of their portfolios averaged 6% annual returns over 30 years.

Same money. Same plan. Same average returns.

Dave's portfolio was basically toast by year 20.

Linda still had over $1.2 million left.

🔴 Dave's Path

- Starting Portfolio $1,000,000

- Retired January 2000

- Withdrawal Rate 4% ($40k/yr)

- Average Return 6%/year

- Result at Year 20 Nearly broke

🟢 Linda's Path

- Starting Portfolio $1,000,000

- Retired 1995

- Withdrawal Rate 4% ($40k/yr)

- Average Return 6%/year

- Result at Year 20 $1.2M+

What the hell happened? Dave retired in January 2000, right before the dot-com crash. Linda retired in 1995, riding the tail end of a bull market. The average return over their retirement was identical — but the order those returns showed up destroyed Dave and saved Linda.

This is sequence of returns risk, and it's the retirement killer that'll mess you up worse than almost anything else. But hardly anyone plans for it properly.

What Is This Sequence Thing, Anyway?

Definition

Sequence of Returns Risk: The danger that the order of investment returns — not just the average — will permanently damage a retirement portfolio. Early losses combined with ongoing withdrawals create a compounding hole that even strong later returns can't fill.

Here's the deal with averages: they're trouble

If your portfolio tanks 30% in year one, you don't just lose 30% of your money. You lose 30% of the money that was supposed to grow for the next 29 years. And you're still pulling money out of that beaten-up portfolio to buy groceries. You're basically digging yourself deeper into a hole.

When the market eventually bounces back — and it always does — you've got way fewer shares left to participate in that recovery. The math gets really ugly, really fast.

Think about it this way. You've got $1 million and lose 20%. Now you're down to $800k. Then you pull out $40k for living expenses, dropping to $760k. To get back to $1 million, you don't need a 20% gain — you need a 32% gain. And every year you keep withdrawing, the hole gets deeper.

| Event | Portfolio Value | Gain Needed to Recover |

|---|---|---|

| Starting balance | $1,000,000 | — |

| After 20% market drop | $800,000 | 25% |

| After $40k withdrawal | $760,000 | 32% |

| After another 10% drop + withdrawal | $644,000 | 55% |

My pal Marcus is a retirement researcher, and he's shown me study after study that proves this: the majority of times retirees run out of money, it's because they got hammered in the first five years. Not the middle, not the end, but right at the beginning.

The timing of bad returns matters way more than the returns themselves. That's messed up, but it's reality.

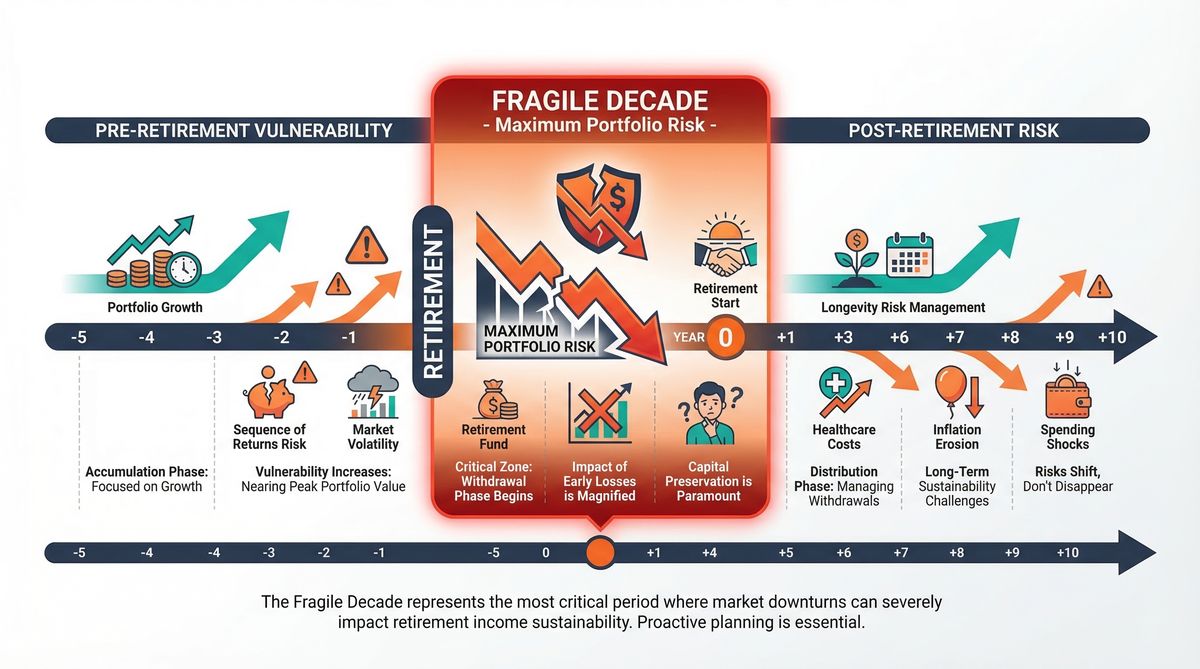

The Fragile Decade: When You're Most Vulnerable

Retirement geeks have this term called the "fragile decade" — roughly five years before you retire through ten years after.

Why these specific years?

Because your portfolio is at its peak size during this period. You've been saving for decades. Your 401(k) is the biggest it's ever been. And ironically, that's exactly when it's most dangerous.

The Fragile Decade

A 30% crash when you have $50k invested costs you $15k. That same crash when you have $1.2 million costs you $360k — literally four or five years of retirement income, gone in months.

The fragile decade cuts both ways:

Before retirement: If the market crashes in the five years before you retire, your portfolio might not have time to recover. You could end up working longer, taking a part-time gig, or living on rice and beans instead of the retirement you planned.

After retirement: If the market crashes in your first ten years of retirement, you're pulling money out of a sinking ship. Each withdrawal makes the decline worse. It's a death spiral that a lot of retirees never escape.

The good news? After about 10–15 years of retirement, this sequence risk mostly goes away. By then, your portfolio has either made it through the storm or it hasn't. If you survived the fragile decade, you're probably gonna be fine.

The question is how to get through those first crucial years without getting wrecked.

History's Worst-Case Scenarios

To understand how bad this can get, let me walk you through some real-world nightmares.

The 1973–1974 Retiree

Picture this: you retire at the start of 1973, ready to enjoy your golden years. Then you walk straight into one of the worst market and inflation combinations in history. The S&P 500 fell about 48% over the next two years. But that wasn't even the worst part — inflation ran about 22% over that same period.

In real terms (what your money could actually buy), retirees lost close to 60% of their purchasing power in just two years. Even the ones who didn't panic-sell faced years of trying to dig out of that hole while everything kept getting more expensive.

The 2000 Retiree

This one hits close to home because I know people who lived through it. If you retired on January 1, 2000 with $1 million in the S&P 500, pulling out 4% ($40k) with inflation adjustments each year, you walked right into the dot-com crash.

Your portfolio tanked, started to recover, then got slammed again by the 2008 financial crisis. By 2009, you were down to about $380k — barely a third of what you started with. Even though the market eventually recovered, your portfolio never did.

Let that sink in. The S&P 500's long-term returns were totally fine over the full period. But the sequence — crash, partial recovery, crash again — while you're withdrawing the whole time? Absolutely devastating.

The Brutal Recovery Math

Here's why early losses are so hard to come back from: after a 20% drop, if you're withdrawing 4% (adjusted for inflation) while earning an average 6% return, your portfolio might never fully recover. The withdrawals keep pulling money out while your shrunken portfolio struggles to generate enough growth. Each year, the gap gets wider.

A portfolio that would've lasted 30+ years without the early crash might fall short by a decade or more. This is why retirement market timing matters so much, and why getting hit early can permanently screw up your financial future.

The Counter-Intuitive Truth About "Playing It Safe"

Here's where things get really interesting — and where most retirement advice falls apart.

You'd think a conservative portfolio would protect you from this sequence risk. More bonds, fewer stocks, less volatility, less risk... right?

Nope.

Research from retirement experts Wade Pfau and Michael Kitces found something that blows most people's minds: in historical simulations, super conservative portfolios (20% stocks, 80% bonds) actually had a higher failure rate than aggressive ones (80% stocks, 20% bonds) when you're withdrawing money every year.

The conservative retiree doesn't blow up in spectacular fashion. They just quietly run out of money because their portfolio never grew enough to sustain decades of withdrawals. It's the silent killer hiding inside the "safe" strategy.

It makes sense when you think about it. Yeah, a conservative portfolio has less ups and downs. But it also generates way lower returns over time. When you're pulling money out every year, you need your portfolio to grow — not just sit there. A portfolio that barely keeps up with inflation while you're withdrawing from it is just a slow-motion train wreck.

This doesn't mean you should go 100% stocks. But it does mean that freaking out and going ultra-conservative as you approach retirement might actually increase your risk, not decrease it.

The real answer isn't choosing between aggressive and conservative. It's building a withdrawal strategy that deals with sequence risk head-on.

7 Ways to Bulletproof Your Retirement Against Sequence Risk

This is where most retirement articles stop — they scare the hell out of you and then leave you hanging. I think you deserve actual solutions. Here are seven concrete strategies, from simple to sophisticated. You don't need all of them. Pick the ones that make sense for your situation.

1. The Cash Buffer Strategy

What it is: Keep 1–3 years of living expenses in cash or short-term bonds, totally separate from your investment portfolio.

How it works: When the market drops, you live off your cash stash instead of selling investments at a loss. This gives your portfolio time to recover without you bleeding it dry with withdrawals.

Example: If you spend $60k per year, keep $120k–$180k in a high-yield savings account or short-term Treasury bills. When the market's up, you refill the buffer. When it's down, you spend from the buffer and leave your investments alone to recover.

The trade-off: Cash earns less than investments long-term. You're giving up some growth for stability. For most retirees, that's a worthwhile trade.

2. The Bucket Strategy

What it is: Split your portfolio into three "buckets" based on when you'll need the money.

How it works:

- Bucket 1 (Years 1–3): Cash and short-term bonds. This is your spending money. Safe, liquid, boring as hell.

- Bucket 2 (Years 4–10): Intermediate bonds and conservative stuff. Moderate growth, moderate stability.

- Bucket 3 (Years 10+): Stocks and growth investments. This money has a decade or more to ride out the volatility.

Why it works: You never have to sell stocks during a crash because your near-term spending comes from Bucket 1. By the time you need Bucket 3, it's had years to grow. You periodically refill Bucket 1 from Bucket 2, and Bucket 2 from Bucket 3 — but only when markets are doing well.

3. Guardrail Withdrawals

What it is: A flexible withdrawal strategy where you adjust your spending based on how the market's doing. This is one of the most powerful tools against sequence risk.

How it works: Set an initial withdrawal rate (say 4%). Then set up guardrails:

- Bad year guardrail: If your portfolio drops more than 10% from where you started, cut your withdrawal by 5–10%. So if you were pulling out $40k, you'd drop to $36k–$38k.

- Good year guardrail: If your portfolio grows more than 20% above where you started, increase your withdrawal by 5–10%. $40k becomes $42k–$44k.

Why it works: Small, temporary spending cuts have a huge impact on whether your portfolio survives. Cutting spending by even 10% during down markets dramatically reduces the "selling at a loss" problem. And you get to enjoy more money during good years.

Real talk: Yeah, this means tightening your belt sometimes. But the alternative — running out of money entirely — is way worse. Most retirees can find 10% to trim when they need to. Skip the European vacation for a year. Eat out twice a week instead of four times. It's temporary.

4. The Rising Equity Glide Path

What it is: Start retirement with fewer stocks and increase them over time — the opposite of what most people do.

How it works: Begin retirement with about 30–40% stocks and 60–70% bonds. Over the first 10–15 years, gradually shift to 60% stocks and 40% bonds.

Why This Works

The rising equity glide path puts your portfolio in its most defensive position right when it's most vulnerable — during the fragile decade. The heavy bond allocation absorbs early retirement market shocks. Then, as sequence risk fades (after year 10–15), you shift into stocks to capture the growth you'll need for the remaining decades. Research by Pfau and Kitces consistently shows this produces better outcomes than the traditional approach of steadily reducing stocks over time.

5. Build a Guaranteed Income Floor

What it is: Use Social Security, pensions, and/or annuities to cover your non-negotiable monthly expenses.

How it works: Figure out your baseline expenses — housing, food, healthcare, utilities. The stuff you can't cut. Then arrange guaranteed income sources (Social Security, pensions, maybe a simple income annuity) to cover that amount.

Why it works: If your guaranteed income covers your essentials, your portfolio only needs to fund your discretionary spending — travel, hobbies, gifts, entertainment. That changes everything. A market crash doesn't threaten your ability to eat or keep the lights on. It just means you might skip the cruise this year.

Key move: Delaying Social Security to age 70 increases your benefit by about 77% compared to claiming at 62. That bigger guaranteed check provides a larger income floor that no market crash can touch.

6. Dynamic Asset Allocation

What it is: Actively shift your portfolio mix based on market valuations, not just a fixed calendar schedule.

How it works: When stock market valuations are historically high (measured by metrics like the CAPE ratio), reduce your stock exposure. When valuations are low (after a crash), increase it.

Why it works: It's basically a disciplined way of buying low and selling high. You're reducing exposure when the risk of a correction is highest and increasing it when the potential for recovery is greatest.

Caution: This requires discipline and some market knowledge. It's not day-trading nonsense — it's more like adjusting your sails based on weather conditions. If this feels too hands-on, strategies 1–5 might be better fits.

7. Part-Time Income Bridge

What it is: Earn even a little money during the first 3–5 years of retirement.

How it works: Consulting, part-time work, freelancing — anything that covers even a portion of your annual spending reduces what you need to withdraw from your portfolio.

Why it works: If you spend $60k per year and earn $20k from part-time work, you only need to withdraw $40k from your portfolio. That's a 33% reduction in withdrawal pressure during the most critical years. Even two or three years of reduced withdrawals can dramatically improve your portfolio's survival rate.

Bonus: A lot of retirees find that some form of work — on their own terms — actually makes retirement more fulfilling, not less. My client Elena retired from corporate law and now teaches yoga three days a week. She makes a few thousand a year and loves it way more than her old job.

Your "Oh Crap" Playbook: Market Crashes Right After You Retire

Okay, so you've retired and the market drops 25% in your first year. Don't panic. Here's your playbook:

Right Away

- Switch to spending from your cash buffer (you did set one up, right?)

- Check your guardrail rules and reduce withdrawals accordingly

- Do NOT sell stocks. Seriously. Do not sell.

Within the First Month

- Calculate your guaranteed income floor (Social Security, pension) and make sure it covers essentials

- Figure out what discretionary spending you can temporarily cut

- Think about whether part-time income makes sense for the next year or two

Over the Next 6–12 Months

- If you're using a bucket strategy, let Bucket 3 (stocks) ride the recovery

- Rebalance — which in a down market means buying stocks with bond money

- Stick to your rising equity glide path plan and don't panic

What NOT to Do

- Don't panic-sell into a falling market

- Don't abandon your strategy for whatever the TV talking heads are saying

- Don't assume the worst case is permanent — most bear markets recover within 2–4 years

- Don't make permanent lifestyle changes based on temporary market conditions

The retirees who survive bad early market crashes aren't the ones with the best crystal balls. They're the ones with the best plans.

The Bottom Line

Sequence of returns risk is real, it's dangerous, and it's totally manageable — if you plan for it.

The worst thing you can do is ignore it and hope you get lucky with retirement timing. Hope isn't a strategy. It's wishful thinking.

The best thing you can do is build flexibility into your retirement plan before you need it. A cash buffer. A bucket system. Guardrail rules you've agreed to ahead of time. A guaranteed income floor. These aren't rocket science. They're just intentional planning.

At Ready Aim Retire, we build tools that help you stress-test your portfolio against exactly these scenarios. Because we think everyone deserves to know — before they retire — whether their plan can survive a rough first five years.

You've spent decades saving for this. Don't let bad market timing in the first few years undo all that work.

You got this!

🎯 Your Sequence Risk Action Plan

- 5+ years from retirement: Start building a 1–3 year cash buffer. Begin shifting toward a defensive allocation for the fragile decade.

- Within 5 years of retirement: Set up your bucket system. Establish guardrail withdrawal rules in writing. Max out Social Security by planning to delay to 70 if possible.

- Just retired: Stress-test your portfolio against worst-case scenarios. Know your guaranteed income floor. Have your "Oh Crap" playbook ready before you need it.

- Everyone: Run your own worst-case scenarios with our planning tools. Know your numbers before you retire — not after.

Stress-Test Your Retirement Plan →