Financial Independence at 55: Twin Brothers' Wealth Gap Story

Julian and Adrian shared everything growing up. Same womb. Same bedroom. Same college dorm room. Eventually, the same engineering degree from State University. They even got hired at the same company on the same day in 1994 — but only one achieved financial independence by 55.

Identical twins with identical careers and incomes ended up with vastly different retirement outcomes:

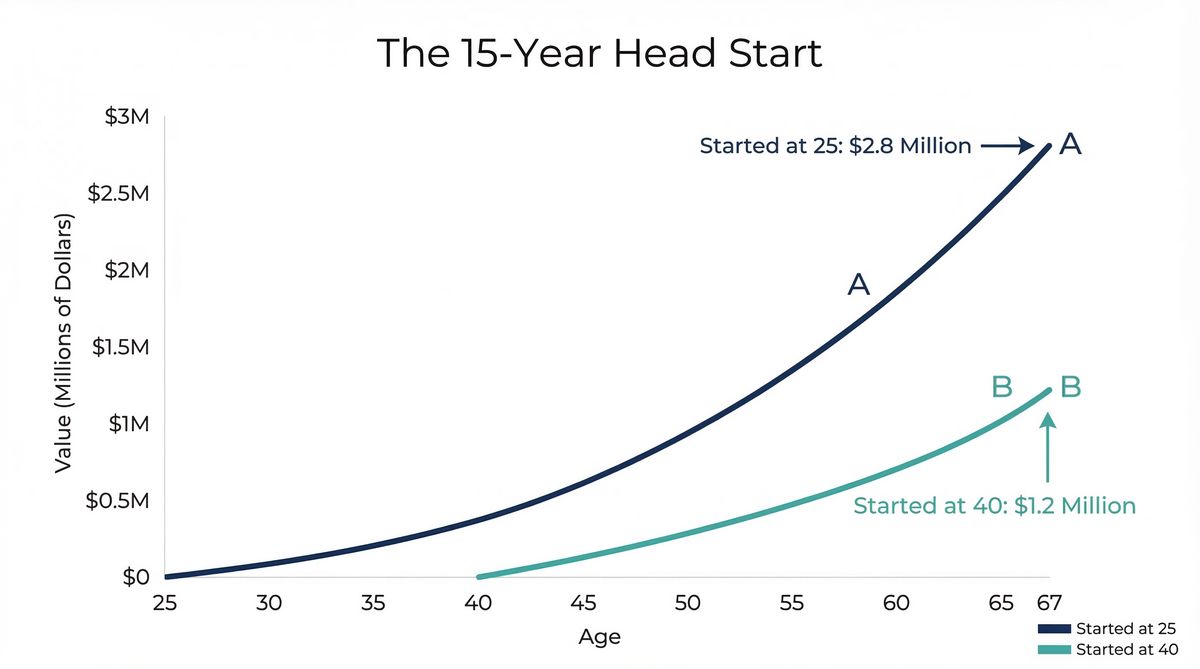

- Julian: Started saving at 25, retired at 55 with $2.8 million

- Adrian: Started saving at 40, working until 70+ with $1.2 million

- The difference: $1.6 million gap from a 15-year delay

Bottom line: Time beats timing, and compound interest is ruthless to late starters.

Julian and Adrian started their careers on the same day in 1994, fresh out of college at 22 years old. Both started at $45,000. Both got the same raises, the same promotions, the same opportunities. By their 40th birthday, both were earning $85,000.

Fast-forward thirty years. Julian achieved financial independence and retired at 55, planning his third Mediterranean cruise. Meanwhile, Adrian just applied for a part-time consulting gig because his mortgage payment's keeping him up at night.

Same DNA. Same opportunities. Same income trajectory. Completely different endings — a perfect case study of how retirement planning decisions create America's growing wealth gap.

Here's the kicker: the only difference between them was a single decision Julian made at 25 that Adrian didn't make until 40.

I've seen this story play out dozens of times, and it never gets less shocking.

How Early Retirement Planning Created a $1.6 Million Wealth Gap

When the company's HR rep explained the 401(k) match during orientation, Julian thought it sounded like free money. "Why wouldn't I want free money?" he asked Adrian over lunch.

Adrian had other priorities. His student loans were eating up $400 a month. His car was making that grinding noise again. And honestly, retirement planning felt about as relevant as planning for his funeral.

"I'll start when I get my life together," Adrian said. "Maybe when I hit 40 and start feeling mortal."

Julian shrugged and signed up anyway. Fifteen percent of his salary, including the company match. It felt like a lot, but he figured he'd adjust.

Adrian waited 15 years.

Big mistake.

The Compound Interest Math Behind Financial Independence

Here's what happened to their money while they were living their identical lives:

Julian's Financial Independence Journey

- Started Saving Age 25

- Initial Rate 15% of $45K

- At 40 15% of $85K

- Total Years Saving 42 years

- Portfolio at 67 $2.8 million

Adrian's Retirement Planning (Late Start)

- Started Saving Age 40

- Initial Rate 15% of $85K

- Continued 15% as salary grew

- Total Years Saving 27 years

- Portfolio at 67 $1.2 million

Both invested in the same target-date funds. Both earned about 7% annually over the long haul. Both saved exactly 15% of their income from the moment they started.

The result? Julian had $1.6 million more than Adrian — a devastating wealth gap created purely by timing.

The Power of Starting Early

Adrian's 15-year delay cost him more money than most people make in their entire careers — despite eventually saving at the exact same rate.

Why Financial Independence Requires Early Action

You've probably heard about compound interest before. Einstein may not have actually called it the eighth wonder of the world, but the math behind financial independence is genuinely mind-bending.

Here's what most people don't grasp: compound interest isn't just powerful for retirement planning. It's ruthless.

Every dollar Julian invested at 25 had 42 years to grow. Every dollar Adrian invested at 40 had 27 years. That 15-year gap doesn't sound catastrophic — until you run the numbers with our retirement timeline calculator.

By the time Julian hit 40, his money was earning more each year than Adrian was contributing. While Adrian was finally getting serious about retirement, Julian's portfolio was already making money faster than Adrian could save it.

Think about that for a second. Julian's money was literally outpacing Adrian's efforts.

Sobering Statistics

According to Federal Reserve data, only 40% of non-retirees believe their retirement planning is "on track." The other 60%? They're essentially Adrian, thinking they'll catch up later. The math doesn't care about good intentions.

The 4% Rule: Julian's Path to Early Retirement

Julian realized he could achieve financial independence when he ran the numbers at 50. His portfolio had hit $1.8 million. Using The 4% Rule — a guideline suggesting you can safely withdraw 4% of your portfolio annually — he could draw $72,000 per year.

The 4% Rule Explained

The 4% Rule: A rule of thumb used to determine how much a retiree should withdraw from a retirement account each year. It seeks to provide a steady income stream while maintaining an adequate account balance over a 30-year retirement.

That was more than enough to cover his paid-off house, his health insurance, and the lifestyle he'd grown accustomed to. He worked five more years because he enjoyed the projects, then walked away with $2.2 million at 55.

Want to see if you're on track for financial independence? Check your chance of success with different withdrawal rates and retirement ages.

Adrian ran his numbers at the same time and nearly threw up.

He had $320,000. His house still had 15 years left on the mortgage. His 4% withdrawal rate would give him about $1,067 per month.

He'd been planning to retire at 62. The spreadsheet told him he'd be working until 70. Maybe longer.

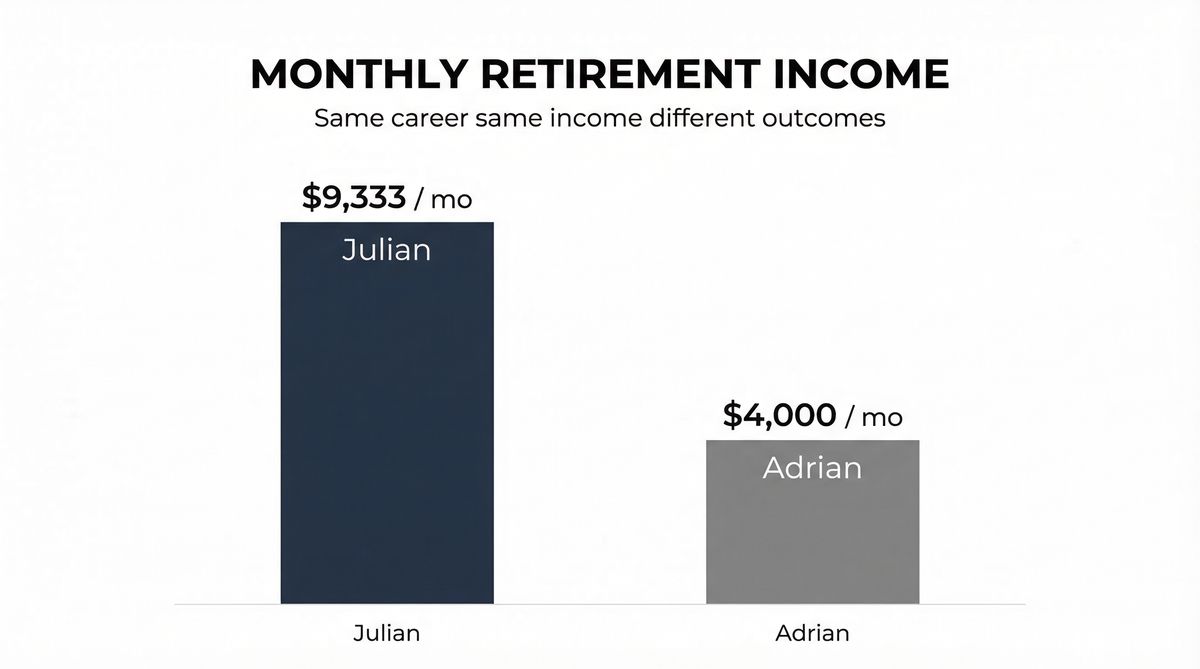

The Monthly Reality of the Wealth Gap

| Brother | Portfolio Value | 4% Annual Withdrawal | Monthly Income |

|---|---|---|---|

| Julian | $2.8 million | $112,000 | $9,333 |

| Adrian | $1.2 million | $48,000 | $4,000 |

That $5,333 monthly difference explains everything. It's the difference between booking cruises and clipping coupons. Between helping your kids with down payments and asking them for help with yours. Between financial independence and financial anxiety.

Use our retirement budget planner to calculate what your retirement lifestyle will actually cost.

Both brothers saved exactly the same percentage of their income once they started. Adrian didn't save less — he just started later.

The Hidden Costs of Delayed Retirement Planning

Adrian's story reveals America's growing wealth gap in retirement preparation. Federal Reserve data shows that 25% of non-retired adults have no retirement savings at all. Another 25% have some, but nowhere near what they need for financial independence.

Even worse, 8% of non-retirees tapped their retirement savings in 2021 due to hardship. When life hits you hard and your 401(k) looks like the only available cash, compound interest becomes compound loss.

Julian never touched his retirement money. Not during the 2008 recession when his home value cratered. Not when he needed a new roof. Not when his daughter wanted to go to private college.

"That money's radioactive. Touch it and everything dies."

How Lifestyle Inflation Prevents Financial Independence

Here's something that might surprise you: Adrian actually out-earned Julian over their careers. After Julian achieved financial independence and retired, Adrian kept getting promoted. He's now a VP making $140,000 per year.

But income without retirement planning is just expensive lifestyle inflation.

Bureau of Labor Statistics data reveals the trap: in 2022, household spending grew 9% while income grew only 7.5%. Most of us are really good at finding ways to spend extra money. We're terrible at automatically saving for financial independence.

The Fidelity Finding

People who increase their savings rate by just 1% early in their careers can add 3% more to their retirement income. But most people do the opposite — they increase their spending rate as their income grows.

Your Path to Financial Independence Starts Now

If you're reading this and you're under 40, you can still achieve financial independence like Julian. You can still capture most of the magic of compound interest for your retirement planning. Even if you're 35 and haven't started, you're looking at about 30 years until traditional retirement age. That's still enough time for compound interest to work its magic.

If you're over 40, you're in Adrian's position. The math's working against you now, but you can still change what happens next in your retirement planning. You might not achieve financial independence at 55 like Julian, but you can avoid working until you're 75.

The Fidelity Guideline

Save 15% of your income for retirement, starting as young as possible. If your employer offers a match, that counts toward your 15%. If not, you need to make up the difference.

Starting late? You'll probably need to save 20% or more to catch up and avoid the wealth gap. The good news? Once you're over 50, the IRS lets you contribute extra "catch-up" amounts to your 401(k) and IRA.

The bad news? It's still not enough to fully make up for lost time in your retirement planning.

Financial Independence vs. Financial Stress

Julian and Adrian's story isn't really about money. It's about freedom and the growing wealth gap in America.

Julian spends his days reading, traveling, and volunteering at the local animal shelter. He takes his grandkids to baseball games on Tuesday afternoons. He learns languages on Duolingo because he can. Financial independence gave him choices.

Adrian spends his days in meetings, worrying about the next round of layoffs, and calculating how many more years he needs to work. He loves his grandkids just as much, but he sees them on weekends when he's exhausted.

Money isn't everything, but financial stress is poison. It affects your health, your relationships, and your ability to be generous with others.

Financial independence isn't about being rich. It's about having choices.

The Simple Truth About Retirement Planning

The difference between Julian and Adrian comes down to one insight: your money works harder than you do when you start retirement planning early.

Julian understood this at 25. Adrian learned it at 40. That 15-year gap cost Adrian his early financial independence, his peace of mind, and about $1.6 million — a devastating personal wealth gap.

But here's what's interesting: both twins are smart, successful people. Adrian's problem wasn't lack of intelligence or discipline. It was lack of urgency about retirement planning that felt distant and abstract.

Retirement planning isn't exciting. It's not immediate. It doesn't solve today's problems. But it's the difference between spending your sixties choosing what to do with your time and spending them hoping you can keep up with the bills.

🎯 Your Next Steps to Financial Independence

- Calculate your current savings rate: Are you saving 15% of your income for retirement planning?

- Max out any employer match: This is free money with immediate returns toward financial independence.

- Automate everything: Make saving as easy as spending — set up automatic transfers.

- Increase gradually: Even 1% more per year adds up dramatically over time thanks to compound interest.

- If you're behind, don't panic — but don't wait: The second-best time to start is now.

Because time's the one investment return you can never get back for financial independence. Julian figured that out early. Adrian learned it the hard way.

Don't be Adrian.