How Much Do I Need to Retire? The Best Rules of Thumb, Explained

Here's a little secret the financial industry would rather you didn't catch on to: almost every retirement "rule of thumb" is the same small pile of arithmetic wearing a different shirt. The 4% rule, the 25x rule, the Rule of 300 — those aren't three ideas. They're one idea, told three ways. And once you see that, the whole thing gets a lot less scary and a whole lot more useful.

There's a catch, though, and honestly it's the most interesting retirement story of 2025 and 2026. The guy who invented the 4% rule just bumped up his own number. Morningstar landed lower. And a third well-respected researcher thinks both of them are still being too generous. On a $1 million portfolio, the gap between these folks is about $17,000 a year. That's roughly $1,400 a month of actual lifestyle. Same money. Same retiree. Totally different advice.

So let's do two things together. First, I'll walk you through the rules in plain English, sorted by the job each one is actually doing. Then I'll show you exactly where they fall apart, so you treat them like a quick first draft instead of gospel.

- The 4% rule, 25x rule, and Rule of 300 are all the same math — just expressed differently.

- Save 15% of gross income starting in your mid-20s, but push it higher if you start late or want to retire early.

- Target 25x your annual expenses for a standard retirement; 33x if you're exiting before 62.

- Subtract Social Security before you apply your multiplier — this alone can cut your target by hundreds of thousands.

- Expert withdrawal rate guidance currently ranges from 3% (Pfau) to 4.7% (Bengen) — a $17,000/year gap on a $1M portfolio.

- Flexible spending strategies can justify starting withdrawal rates of 5% or higher.

The four jobs a retirement rule of thumb can do

Every formula you've ever heard is really just answering one of four questions:

- How much should I save while I'm working? (the inputs)

- How big does my nest egg need to be? (the target)

- How much am I actually going to spend? (the budget)

- How much can I safely pull out each year? (the outflow)

Group them this way and the fog lifts. Let's take them one at a time.

Job 1: How much to save (the 15% rule)

The old-school baseline is dead simple. Save 15% of your gross income every year, start in your mid-20s, and you should land in a comfortable retirement somewhere in your late 60s. Fidelity, who made this number famous, is refreshingly upfront about the fine print: that 15% assumes you start at 25, you keep more than half your money in stocks over your lifetime, and you retire at 67.

Read that one more time, because it's the trapdoor hiding under nearly every rule of thumb. They almost all assume you retire at 67. Start saving at 35 instead of 25, or decide you want to be done at 55, and suddenly 15% doesn't cut it anymore.

So if you got a late start, or you want to bow out early, think of 15% as your floor, not your finish line. For every five years you knock off the back end, nudge that savings rate up a few points.

Job 2: How big the nest egg should be (the target rules)

This is the part most people actually care about, and there are two rival camps here.

The income camp: the 10x salary rule

Fidelity popularized this one too. It says aim to have 10 times your final pre-retirement salary banked by age 67. To keep you honest along the way, it breaks down into milestones across your career:

Fidelity savings milestones by age

- Age 30: 1× your salary

- Age 40: 3× your salary

- Age 50: 6× your salary

- Age 60: 8× your salary

- Age 67: 10× your salary

These are genuinely handy for a 30-second gut check. If you're 40 and pulling in $100,000, you want roughly $300,000 sitting there. Behind the pace? Good. Now you know to fix it today, not at 65 when there's no runway left.

The expense camp: the 25x rule

If you're not planning to wait around until 67, building your target off your salary stops making sense. So the expense rules ignore your paycheck completely and look at what you actually spend. Take your expected annual expenses, multiply by 25. Need $60,000 a year to live your life? Your target is $1.5 million.

Three Rules. One Truth.

That 25 isn't pulled out of thin air. It's the 4% rule flipped on its head — 1 ÷ 0.04 = 25. And the Rule of 300, which says multiply your desired monthly income by 300? Same equation, third costume. Because 25 years × 12 months = 300. So $5,000/month × 300 = $1.5 million — the exact same answer as $60,000/year × 25.

For the early-exit crowd: the 33x rule

If you want to retire before 62, your portfolio has to last 40 or 50 years instead of 30. That longer haul needs a bigger cushion, so you multiply your annual expenses by 33 (which lines up with a safer 3% withdrawal rate). Spend $60,000 a year and your target jumps from $1.5 million at 25x to nearly $2 million at 33x. That extra $480,000 or so is simply what it costs to buy your money one or two more decades of survival.

When the target rules openly disagree

Now watch what happens when you run a real human being through both camps. Picture my buddy David, 45 years old, earns $120,000, spends $70,000.

| Rule Applied | Calculation | Retirement Target |

|---|---|---|

| 10x Salary Rule | 10 × $120,000 salary | $1.2M |

| 25x Expense Rule | 25 × $70,000 annual spending | $1.75M |

| 25x After Social Security | 25 × $40,000 gap (after ~$30K/yr SS) | $1.0M |

Same David. Targets ranging from $1.0 million to $1.75 million. That's a $750,000 spread. The income rule and the expense rule are not interchangeable, even though plenty of blogs love to line them up side by side like they are. The 10x rule is a stand-in for your gross income — dollars you stop earning and stop saving the day you walk out the door. The 25x rule is built from your actual spending — the dollars you genuinely live on. They're answering different questions, and the expense rules (once you fold in Social Security) tend to land closer to real life.

That Social Security piece deserves a spotlight, because most multiplier rules quietly pretend it doesn't exist. Social Security replaces only about 40% of pre-retirement income for an average earner, and the average retired-worker benefit is roughly $2,071 a month in 2026. It's not going to carry you on its own. But for a lot of households it does real, meaningful heavy lifting that the raw 10x and 25x numbers act like isn't even there.

Which camp you fall into depends entirely on your own numbers. Running your own projections on ReadyAimRetire is a fast way to see how Social Security and your real spending shift the target for your specific situation — not a hypothetical like David.

Run My Retirement Numbers Free →

Job 3: How much you'll spend (the 80% rule, and why it's usually wrong)

The classic budgeting shortcut says you'll need about 80% of your pre-retirement gross income to keep your lifestyle, because a bunch of costs just evaporate: payroll taxes, the commute, and the very act of saving for retirement all stop the day you clock out for good.

It's a fine place to start and a lousy place to stop. The real data shows most retirees spend 70% or less, with the actual observed range running anywhere from 54% all the way up to 87%. And here's the part that really got me. J.P. Morgan dug into real-life Chase customer data and found that replacement need actually moves the opposite direction from income.

Lower Earner ($30K/yr)

- Income Replacement Needed ~104%

- Reason Wasn't saving much — SS and portfolio must do all the work

- Rule of thumb fit 80% understates the need

Higher Earner ($300K/yr)

- Income Replacement Needed ~55%

- Reason High savings rate + taxes both vanish at retirement

- Rule of thumb fit 80% overstates the need

So the one-size-fits-all 80% number is too high, especially for high earners. If you're a strong saver in a high tax bracket, your true replacement ratio is probably closer to 55% or 60%, which can shrink your target in a big way.

The Retirement Spending Smile

Researcher David Blanchett found that real spending doesn't hold steady through retirement — it drifts down as people move from active "go-go" years into slower "slow-go" and "no-go" years. A household starting at $100,000 a year can watch real spending fall to around $74,146 by age 84. Because every multiplier rule assumes flat, inflation-adjusted spending forever, Blanchett warns the rules "will lead individuals to over-save for retirement." Sit with that for a second. The rules might be telling you to grind for years longer than you actually need to.

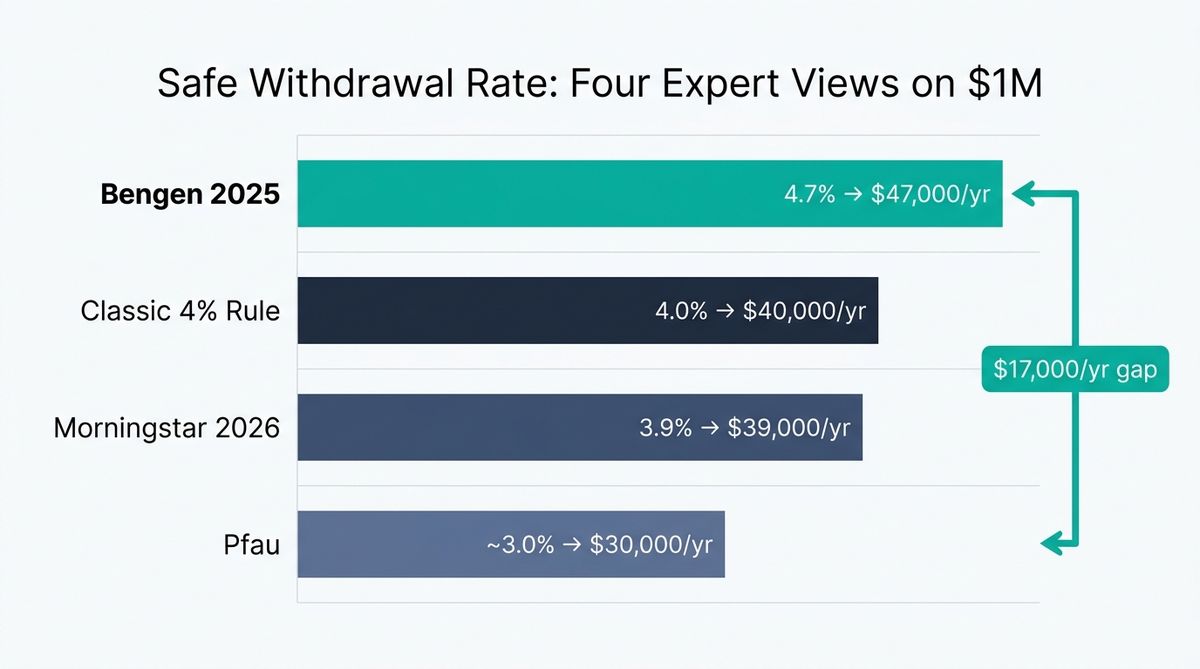

Job 4: How much to withdraw (and the safe withdrawal rate fight of 2026)

Finally, the outflow. This is the headline act.

The 4% rule. Born from William Bengen's 1994 research and backed up by the famous Trinity Study, it says you can withdraw 4% of your portfolio in year one of retirement, then adjust that dollar figure for inflation every year after, with a high probability your money lasts 30 years. A $1 million portfolio hands you $40,000 in the first year. Clean, memorable, and for three solid decades it was the default answer to "how much do I need to retire?"

Then 2025 rolled around, and the agreement came apart. Here's where things stand right now on safe withdrawal rates — and no honest article should tie it up in a bow for you, because the experts haven't tied it up for themselves.

- Bengen now says 4.7%. In his August 2025 book A Richer Retirement, the rule's own inventor raised his "new default" to 4.7%, after factoring in broader diversification, market valuations (the Shiller P/E), and expected inflation. On $1 million, that's $47,000 a year. About retirees still clinging to 4%, he says flat out, "I think they're cheating themselves a little bit." He also points out that the rate which always worked historically averaged around 7.1% — the famous 4% was only ever the worst-case floor, never the typical result.

- Morningstar says 3.9% for 2026. Leaning on forward-looking return forecasts instead of historical data, Morningstar puts the safe starting rate at 3.9% for 2026, up from 3.7% in 2025 and as low as 3.3% back in 2021. On $1 million, that's $39,000.

- Wade Pfau says closer to 3%. Pointing at today's high valuations, Pfau figures the original 4% rule has only a "65% to 70% chance" of working for today's retirees — not the near-sure-thing people assume. A 3% rate means $30,000 on that same million.

Line them all up on one $1 million portfolio:

| Authority | Rate | Year-one income on $1M |

|---|---|---|

| Bengen (2025) | 4.7% | $47,000 |

| Classic 4% rule | 4.0% | $40,000 |

| Morningstar (2026) | 3.9% | $39,000 |

| Pfau | ~3.0% | $30,000 |

Same nest egg. A $17,000-a-year lifestyle gap depending on who you trust. The disagreement is mostly about method: Bengen leans on historical U.S. returns, Morningstar on forward-looking forecasts, Pfau on the warning that high starting valuations drag future returns down. Or, as the planning platform Boldin nicely put it, these rules are "helpful starting points, but dangerous endpoints." If you want to see what each of these rates actually looks like mapped against your own portfolio and timeline, ReadyAimRetire lets you model the scenarios side by side with your real numbers.

The honest upgrade path

If a single fixed percentage feels kind of unsatisfying to you, good. That's the right instinct. The most useful research points toward flexible spending instead of one rigid, inflation-adjusted check every year. Morningstar finds that retirees willing to vary their spending year to year — taking a little less after a rough stretch in the early years of retirement, a little more after a good one — can justify starting rates of 5% or even 6%.

The Guyton-Klinger "guardrails" approach turns this into actual rules that cut or raise your spending when your portfolio crosses preset thresholds, and it supports 5% to 5.5% starting rates with failure risk about the same as a static 4%.

The lesson here isn't "just pick the highest number." It's that rigidity is the whole reason the low numbers are necessary in the first place. Build in some flexibility and you basically hand yourself a raise.

Model My Withdrawal Strategy →

What to actually do with all this

Rules of thumb are a 60-second first draft of your retirement plan. They get you in the ballpark fast, which is genuinely valuable when the alternative is staring at the wall, frozen. So here's how to use them well and then move past them.

Your Retirement Planning Action Steps

- Start with an expense-based target, not an income one. Multiply your real annual spending by 25 (or 33 if you're retiring before 62). This anchors on the number that actually matters — what your life costs.

- Subtract Social Security before you multiply. Estimate your Social Security benefit, subtract it from your annual expenses, and apply the multiplier only to the gap. This one move can cut your target by hundreds of thousands of dollars.

- Right-size the 80% rule to your income. High earner and strong saver? Plan on 55% to 65% replacement, not 80%. Lower earner? Budget closer to 100%.

- Pick a withdrawal rate that matches your flexibility. If your spending is rigid, lean toward 3.5% to 4%. If you can dial it back in down markets, 4.7% or a guardrails strategy is totally defensible.

- Account for what no rule covers. None of these formulas include healthcare, long-term care, or taxes on your withdrawals — and the Medicare supplement decision alone can swing your out-of-pocket costs by $50,000 or more. Pad your number for them on purpose.

Once you've worked through these steps, the natural next move is to pull your actual numbers together in one place. ReadyAimRetire.com is built exactly for that: you can test how your savings rate, retirement age, Social Security timing, and spending assumptions interact — rather than applying each rule of thumb in isolation and hoping they add up.

The rules of thumb did their job the moment they handed you a target to react to. The real plan starts when you adjust that target for your actual retirement age, your real spending curve, Social Security, taxes, and how much flexibility you've got in you. Even the people who wrote these rules keep revising them. That's not a reason to distrust the math. It's permission to keep refining your own.

Thanks for reading if you've made it this far. Peace!