How to Retire Early in 8 Steps

Ask most people when they're going to retire and they'll say 65 without even thinking about it. It's the default. But more and more folks I talk to have an early retirement number rattling around in their head. 54. 50. Sometimes 45. I get the appeal completely. The hard part isn't wanting it. The hard part is the math.

Here's the thing nobody tells you at the start. Retiring ten or fifteen years before the usual finish line means your money has to stretch across 40 years instead of 25. You're locked out of Medicare and Social Security for a good while. And if the market takes a nosedive in your first few years out, it can quietly unravel a plan that looked airtight on the spreadsheet.

But I've got good news, and I really believe this: early retirement isn't a lottery ticket. It's an engineering problem. You hit a high savings rate, you pick a withdrawal rate you can actually defend, and you build the bridges that carry you safely to 59½, then 65, then beyond. That's it. So let's walk through the eight steps, updated for the rules and numbers that actually matter in 2026.

- Estimate your retirement spending — start with 80% of current income, then model the go-go, slow-go, and no-go spending curve across your retirement decades.

- Determine your retirement length — plan for 40+ years if you're retiring in your 50s, not 25–30 like a traditional retiree.

- Calculate your target savings goal — the 33x rule (3% withdrawal) is the early-retiree benchmark; 25x (4%) is the traditional floor.

- Set your savings rate for financial independence — saving 50% of take-home gets you there in ~17 years; 65%+ in about 10.

- Maximize tax-advantaged accounts: 401(k), IRA, and HSA — know your 2026 limits, the new super catch-up, and the SECURE 2.0 Roth mandate.

- Invest for compound growth and portfolio sustainability — equities are non-negotiable over a 40-year horizon; find an allocation you can hold through downturns.

- Map out taxes, health care, and Medicare bridges — Rule of 55, 72(t) SEPP, and the Roth conversion ladder are your tools before 59½; MAGI management is your tool before 65.

- Decide when to claim Social Security — waiting from 62 to 70 can increase your monthly check by ~77%.

Step 1: Estimate Your Retirement Spending

Start simple. Assume you'll spend about 80% of what you earn before you retire. Money folks call this the income replacement ratio, and the logic is that some costs just vanish once you stop working. Payroll taxes go away. The money you were socking into savings? You don't need to set that aside anymore. So if you're pulling in $100,000 today, pencil in roughly $80,000 a year once you're out.

Now, treat that 80% like a rough sketch, not the gospel truth. Michael Finke, who teaches personal financial planning over at Texas Tech, flat out calls the rule "imprecise." He warns that it "encourages people to save an amount of money that may not be needed." And he's right, because real spending in retirement almost never holds flat. It moves in a curve.

Advisors describe the spending curve with three phases:

- Go-Go Years (early retirement): Spending peaks — travel, bucket-list experiences, everything you put off while working.

- Slow-Go Years (mid-70s): Activity and expenses taper as pace of life naturally slows.

- No-Go Years (80s+): Spending creeps back up, mostly driven by health care costs.

Some planners model this as an 80–70–60 glide path instead of a single flat income-replacement number.

For those of us who want out early, this step is your biggest lever. Every single dollar you trim from your future budget shrinks the pile you need to build. And keep one eye on lifestyle creep, because it's sneaky. Those raises and bonuses that quietly puff up your spending in your 40s? That's the exact same money that could've bought you an earlier exit. Planning for a leaner life on purpose is one of the fastest ways to pull your retirement date forward.

Step 2: Determine Your Retirement Length

Your money has to outlive you. So be honest with yourself about the timeline, and plan for the long tail instead of the average. If you make it to 65, the median life expectancy lands somewhere in the mid-80s. But a real chunk of retirees sail well into their 90s, and if you're married, the odds that at least one of you hangs around that long go up even more. Build your plan around beating the average. Because honestly, beating the average is the outcome you're rooting for.

Traditional Retiree (age 67)

Portfolio needs to cover 25–30 years. Retires with Medicare already in reach and Social Security close behind.

Early Retiree (age 54)

Portfolio needs to cover 40+ years. Faces a decade-plus gap before Medicare and must self-fund years before Social Security makes sense to claim.

That extra decade and a half changes nearly every assumption that comes next, starting with how much you can safely pull out each year.

Step 3: Calculate Your Target Savings Goal

This is where early retirement math splits off hard from the standard playbook. Pay attention here.

You've probably heard of the 4% rule. It came out of the Trinity Study, and it was built for a 30-year retirement. Stretch your horizon to 40 years and that safe number drops. Some recent Morningstar research puts the highest sustainable starting withdrawal rate for a 40-year stretch at roughly 3.1%. That's exactly why early-retirement planners lean on the 33x rule.

A 3% withdrawal rate is simply the inverse of 33: 1 ÷ 0.03 = 33.3. Save 33 times your annual expenses, draw 3% a year, and historically the plan's success rate approaches 100% — even across 60-year stretches. It's the early-retiree alternative to the traditional 25x (4%) benchmark.

Let's run your number. Say you spend $75,000 a year. Your target is $75,000 × 33 = $2.475 million.

Now I owe you an honest caveat, because this is a live debate. William Bengen, the guy who actually created the 4% rule, bumped his own "safe" rate up to 4.7% in 2025 using a more diversified portfolio. In December 2025 he went further, saying early retirees who anchor on ultra-cautious rates "may be cheating themselves" out of a richer life by oversaving and working too long. So watch what this one assumption does to your number:

| Withdrawal Rate | Savings Multiple | Target (at $75,000/yr spending) |

|---|---|---|

| 3.0% — conservative | 33x | $2,475,000 |

| 4.0% — traditional Trinity | 25x | $1,875,000 |

| 4.7% — Bengen 2025 revised | ~21x | ~$1,600,000 |

The gap between the cautious end and the aggressive end is nearly $900,000 — several years of your working life right there. The conservative 3% is guarding against something real called sequence-of-returns risk: the danger that a crash early in retirement forces you to sell assets at a loss you never claw back. That risk is genuine, and it's the actual reason early retirees take less. But 3% is not settled science. Pick your spot on the spectrum based on how much room you've got to cut spending in a bad year.

Run Your Own Numbers

You can test all three withdrawal rate scenarios against your actual spending at ReadyAimRetire.com to see exactly how each shifts your savings target and retirement timeline.

For comparison, a standard retirement at 67 only targets 10x to 12x your salary with a 4% to 5% withdrawal rate. Fidelity's milestones — 1x salary saved by 30, 3x by 40, 6x by 50, 10x by 67 — assume that gentler path. Bump your exit to 62 and the target climbs toward 14x. Retire at 54 and it climbs a whole lot higher. The earlier you stop, the more multiples you need. Simple as that.

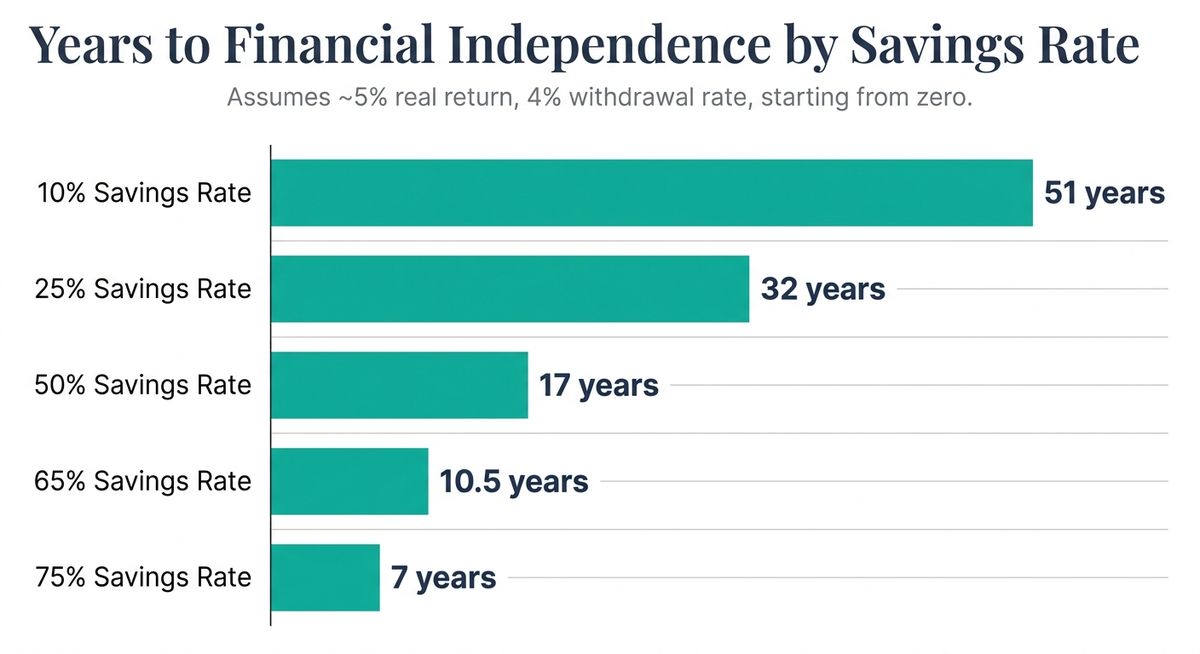

Step 4: Decide Your Annual Savings Rate for Financial Independence

Okay, here's the single most important number in this whole thing. And it's not your income. It's your savings rate.

Standard planning tells you to save 15%. Early retirement asks for a lot more. The relationship between your savings rate and how soon you hit financial independence is brutal — but it's also kind of beautiful in how clear it is:

| Savings Rate (of take-home pay) | Years to Financial Independence |

|---|---|

| 10% | ~51 years |

| 25% | ~32 years |

| 50% | ~17 years |

| 65% | ~10.5 years |

| 75% | ~7 years |

| Assumes ~5% real return, 4% withdrawal rate, starting from zero. | |

"There's only one factor that really matters: your savings rate." — Mr. Money Mustache

The reason is mechanical, not magic. A high savings rate does two jobs at once. It shrinks the lifestyle you have to fund, and it grows the pile that funds it. Picture two workers, one making $80,000 and one making $250,000, both saving 70% of their take-home pay. They reach financial independence in roughly the same 8.5 years. Your income sets the ceiling on how fast you can save. But the rate sets the timeline.

Count every channel you've got. Your workplace 401(k), your IRAs, a health savings account, taxable brokerage accounts, and your full employer match — free money and an instant return you should never leave sitting on the table. And if you're over 50, stack in catch-up contributions to push hard through the final stretch.

Ready to run your own numbers?

See how your savings rate stacks up with ReadyAimRetire's free retirement calculator.

Try It Free →Step 5: Maximize Tax-Advantaged Accounts: 401(k), IRA, and HSA

Think of taxes as a slow leak in the bucket. Plug the leak and you free up cash to save. Fill your tax-advantaged accounts in a smart order, and know your 2026 limits cold:

| Account | 2026 Limit | Catch-Up (age 50+) | Super Catch-Up (ages 60–63) |

|---|---|---|---|

| 401(k) / 403(b) / 457 | $24,500 | +$8,000 | +$11,250 |

| IRA (traditional or Roth) | $7,500 | +$1,100 | n/a |

| HSA (self-only) | $4,400 | +$1,000 (age 55+) | n/a |

| HSA (family) | $8,750 | +$1,000 (age 55+) | n/a |

Traditional 401(k), IRA, and HSA contributions knock down your taxable income right now. Roth accounts grow tax-free and come out tax-free down the road. Two 2026 wrinkles are worth circling. First, the "super catch-up" for ages 60 to 63 lets you add an extra $11,250 into your workplace plan — a serious late-stage tool. Second, under SECURE 2.0, high earners (roughly $145,000 or more in prior-year wages) must now make catch-up contributions as Roth dollars instead of pre-tax.

The health savings account is the only account that's triple tax-advantaged: deductible going in, tax-free growth, and tax-free withdrawals for medical costs. The stealth IRA move: pay your current medical bills out of pocket, save the receipts, and let the HSA compound for decades. You can reimburse yourself tax-free at any future point. After age 65, the HSA functions exactly like a traditional IRA for any purpose at all.

Once those accounts are full, keep going in a plain taxable brokerage account. For early retirees this is essential — it's money you can actually reach before 59½ without jumping through any of the hoops in Step 7.

Step 6: Invest for Compound Growth and Portfolio Sustainability

A 40-year retirement has a quiet enemy lurking in the background: inflation. Bengen calls it the retiree's "greatest enemy," and over four decades even modest inflation can cut your buying power in half. Cash and bonds on their own just can't outrun it.

Which makes stocks non-negotiable. You need the compound growth that equities deliver, both to reach your number and to hold onto it across the decades. The balancing act is lining up your stomach for market swings against the returns your timeline actually demands.

"A portfolio that's too timid to grow is its own kind of risk."

Notice this: Bengen's revised 4.7% figure assumes a diversified mix of roughly 55% stocks, 40% bonds, and 5% Treasury bills. So "growth-oriented" does not mean "all stocks." Find an allocation you can hold through a downturn without panic-selling, because the investor who stays put is the one who actually captures the long-run returns. My buddy David learned that the hard way in 2008, sold at the bottom, and still talks about it. Don't be 2008 David.

Step 7: Map Out Taxes, Health Care, and Medicare Bridges

This is the step the generic articles get wrong, and it's where early retirement is genuinely won or lost. Leaving work before the standard milestone ages opens two gaps: getting at your money without a penalty, and getting health insurance before Medicare kicks in at 65. Let's take them one at a time.

Reaching Your Money Before 59½

You've got three main tools.

Leave your job in or after the year you turn 55, and your current employer's 401(k) may let you take penalty-free withdrawals. It does not apply to IRAs — and here's the trap: rolling that 401(k) into an IRA forfeits the privilege entirely. Check your plan's rules before you move a single dollar.

To tap an IRA before 59½, IRS Section 72(t) lets you take substantially equal periodic payments without the 10% early-withdrawal penalty. The catch is rigidity. Payments must continue for five years or until you hit 59½ — whichever is longer. Break the schedule and you trigger retroactive penalties plus interest on every distribution.

Each year you convert money from a traditional account into a Roth, you pay ordinary income tax on the conversion, then wait five calendar years and withdraw that converted principal penalty-free and tax-free at any age. Convert $60,000 in 2026 and you can pull it out in 2031. Because of that five-year lag, you need a separate cushion to live on — typically taxable brokerage funds — while the first rungs of the ladder season. This is the most popular bridge in the financial independence community, and the one most "8 steps" articles skip entirely.

Bridging to Medicare at 65

Health insurance is now the most urgent and expensive piece of an early-retirement plan — and that's because of a 2026 rule change. Under current law as of mid-2026, the enhanced ACA premium tax credits have expired, which reinstates the subsidy cliff at 400% of the federal poverty level. (The House passed a multi-year extension in January 2026, but it hadn't become law as of this writing — confirm current rules before you build a plan around them.)

The Subsidy Cliff Is Real

A 60-year-old who keeps modified adjusted gross income (MAGI) at $62,000 pays roughly $6,200 a year for marketplace coverage. Let that income drift to $64,000 — just barely over the cliff — and the bill jumps to about $14,900. That's an $8,700 penalty for $2,000 of extra income.

For early retirees, this turns MAGI management into a core discipline — and it ties directly back to the Roth conversion ladder, because every conversion bumps your MAGI. Convert too aggressively and you sail past the cliff. The same discipline pays off later: big conversions in your early 60s can also inflate your Medicare Part B and D premiums via IRMAA surcharges, which look back two years at your income.

Your options to bridge the years to 65:

| Coverage Option | What to Know |

|---|---|

| COBRA | Keeps your employer plan for up to 18 months at full premium + 2% admin fee — often $600–$800/month per person |

| Spouse's employer plan | Usually the cheapest route by far, if you have access to one |

| ACA marketplace | Careful MAGI management keeps you under the subsidy cliff; COBRA only covers 18 months, so plan for 8+ more years of marketplace coverage |

| HSA | Cover premiums and out-of-pocket costs with pre-tax dollars accumulated during your working years |

Retire at 55 and you're staring down roughly 10 years of self-funded coverage. COBRA only covers the first 18 months, so the marketplace or a spouse's plan has to carry the remaining eight-plus years. Build that cost into your budget from day one. Don't let it ambush you.

Step 8: Decide When to Claim Social Security

Social Security is the last bridge, and when you claim it is worth real money. You can start as early as 62, but doing so permanently cuts your monthly benefit by about 30% compared to your full retirement age of 67. Wait past full retirement age and your benefit grows 8% a year until it tops out at 70.

Claim at 62

A $2,000 full-retirement-age benefit shrinks to about $1,400/month — a permanent 30% reduction you carry for life.

Wait Until 70

That same benefit grows to about $2,480/month — a $1,080/month swing, nearly 77% more, just for waiting eight years.

Benefits stop growing after 70, so there's no reason on earth to wait past that. For early retirees, delaying usually wins, because that bigger check is guaranteed, inflation-adjusted income you literally cannot outlive. The trick is funding the gap years in between. Plan to bridge that stretch with your own savings, or with an immediate annuity that hands you a paycheck until your delayed benefit shows up.

Your Move

Early retirement isn't one big heroic decision. It's built in the order we just walked through. Know your spending. Size your number against a withdrawal rate you can defend. Push your savings rate as high as your life allows. Shelter every dollar you can from taxes. Invest for compound growth. And engineer the bridges to 59½, 65, and your Social Security claim.

Take Action This Week

- Still working? Calculate your real savings rate from your last three pay stubs and find one expense to cut. Even trimming $500 a month compounds into years shaved off your timeline.

- Within a decade of retiring? Run your nest egg against all three withdrawal rates — 3%, 4%, and 4.7% — so you know exactly where you stand on the spectrum before you need to commit.

- Eyeing an exit before 65? Price out marketplace coverage at your target income today, before the subsidy cliff turns a carefully built plan into an expensive surprise.

Every retirement plan is different, and small changes in assumptions can shift your target by hundreds of thousands of dollars. ReadyAimRetire lets you pull all of these variables together in one place, so you can test how your specific numbers hold up across different scenarios and revisit the plan as your situation changes.