Modern Safe Withdrawal Rates: Why the 4 Percent Rule Is Officially Dead in 2026

So here's something wild. Bill Bengen, the guy who literally invented the 4 percent rule, doesn't even use it anymore. He now says 4.7% is the real safe withdrawal rate. Morningstar's team says it's actually 3.9%. And a 2025 study out of Santa Clara University argues that no fixed withdrawal rate is universally safe. Period.

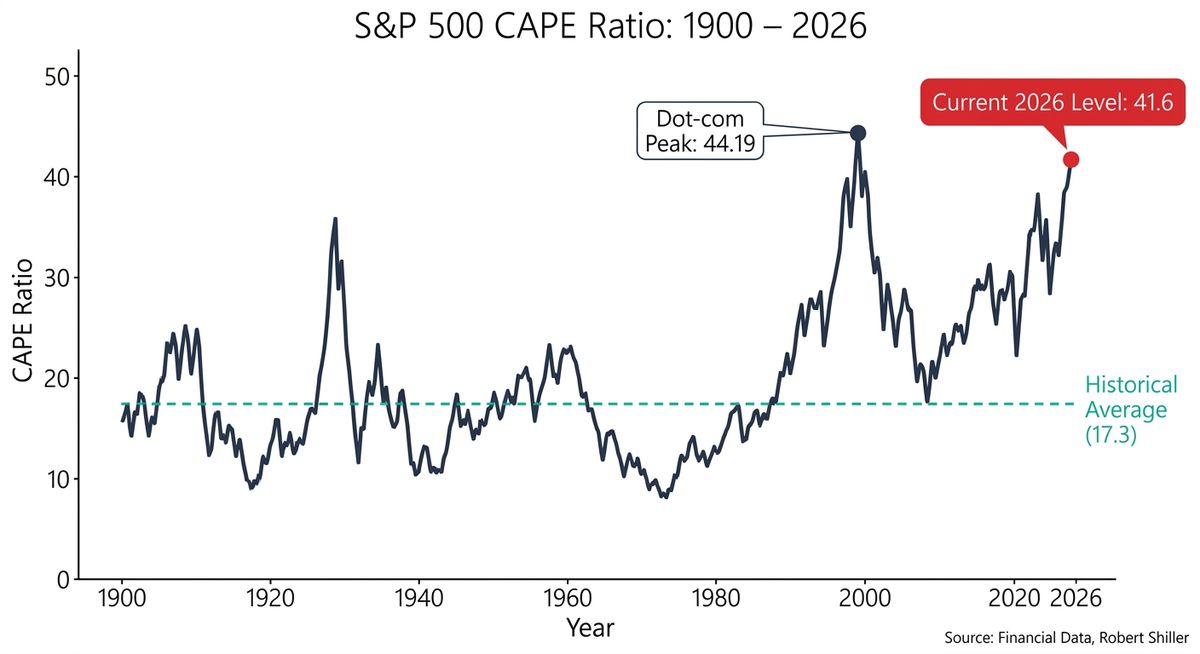

- Current market conditions: S&P 500 CAPE ratio at 41.6 (second highest ever) makes fixed withdrawal rates dangerous

- Expert disagreement: Bengen now recommends 4.7%, Morningstar says 3.9%, Santa Clara research suggests no fixed rate is safe

- Better approach: Dynamic guardrail strategies starting at 5%+ with flexible adjustments based on portfolio performance

- Floor-and-upside framework: Combine TIPS for essential expenses with equity growth for discretionary spending

- Action step: Calculate your CAPE-adjusted starting rate using Big ERN's formula: 1.75% + 0.5 × (1/CAPE)

Action: Stop chasing a magic number and embrace modern retirement withdrawal strategies that adapt to market conditions.

Think about that for a second. The people who built this framework can't agree on whether their own rule is too conservative or too aggressive. So what's a regular person with a million-dollar portfolio supposed to do?

I'll tell you what: stop chasing a magic number and embrace modern retirement withdrawal strategies.

The 4 percent rule was a solid starting point back in 1994. But in 2026, with the S&P 500's CAPE ratio sitting at 41.6 (basically the second highest it's ever been, right behind the dot-com peak of 44.19), a set-it-and-forget-it withdrawal strategy isn't just outdated. It's a coin flip with your retirement.

The good news? There are better approaches. Let me walk you through them.

The 4 Percent Rule Was Never Meant to Be a Rule

Back in 1994, financial planner William Bengen did something pretty brilliant. He analyzed every 30-year retirement period going all the way back to 1926. He found that a retiree who withdrew 4% of their portfolio in year one, then adjusted that dollar amount for inflation each year, never ran out of money. He called this the "SAFEMAX," the worst-case safe withdrawal rate.

And then the financial planning industry ran with it like it was carved in stone.

What Is SAFEMAX?

SAFEMAX is the highest withdrawal rate that would have worked in the worst historical 30-year period. Bengen's original study found this to be 4.15% (rounded to 4%) using a portfolio of 50% S&P 500 stocks and 50% intermediate-term Treasury bonds.

But here's the thing. Bengen himself has spent three decades updating his own work. His 2025 book A Richer Retirement bumps the SAFEMAX up to 4.7%. How? By expanding beyond the original two-fund portfolio (S&P 500 plus intermediate-term Treasuries) to include mid-cap, small-cap, micro-cap, and international equities. He told CNBC in December 2025 that most retirees today should actually draw closer to 5.0% to 5.5%, and that the historical average safe withdrawal rate across all periods was roughly 7%.

Meanwhile, Morningstar's 2025 State of Retirement Income report (authored by Christine Benz, Jeffrey Ptak, and John Rekenthaler) sets the base-case safe withdrawal rate for 2026 at 3.9%. That's up from 3.7% in 2025, thanks to better bond yields, but still below the famous 4% threshold.

So which is it? 3.9% or 4.7%?

Honestly? Both. It depends on your assumptions. Morningstar uses a 90% success probability, a conservative 30-50% equity allocation, and forward-looking capital market estimates. Bengen uses historical backtesting with a broadly diversified portfolio and demands 100% success against actual past returns. They're answering slightly different questions with different data. And that's exactly the problem with treating any single number as a rule.

Why 2026 Is Especially Dangerous for Static Withdrawal Rates

The S&P 500's Shiller CAPE ratio stood at 41.6 in May 2026. The long-run average is 17.3. The only time valuations were higher was during the dot-com bubble. I don't love making dramatic comparisons, but that one kind of makes itself.

This matters a lot for retirees because of something called sequence-of-returns risk. When you're pulling money out of a portfolio, early losses hurt way more than later ones. You're selling shares at depressed prices to fund your withdrawals, which leaves fewer shares to participate in any recovery. It's like trying to fill a bathtub while someone keeps pulling the drain plug.

Sequence of Returns Risk

The sequence of returns risk can destroy 30 years of savings if you hit bad market timing in your first five years of retirement. When starting withdrawals at high valuations, even a moderate bear market can trigger a portfolio death spiral.

Karsten "Big ERN" Jeske (whose 62-part Safe Withdrawal Rate Series is probably the most thorough public analysis of retirement spending out there) has shown that when the CAPE exceeds 30, the failure probability for a 4% withdrawal rate jumps from 3-4% to 15-20%. That's not a rounding error. That's one-in-five odds of running out of money. I don't know about you, but I wouldn't board a plane with those odds.

Let me paint you a picture. A 65-year-old retires in January 2026 with $1,000,000. She withdraws $40,000 in year one using the classic 4 percent rule, adjusting for inflation each year. If the first five years deliver returns similar to 2000-2004 (a reasonable comparison given current CAPE levels), the portfolio could drop to roughly $650,000 by year five. But her inflation-adjusted withdrawals have climbed to about $44,000. That means her effective withdrawal rate has ballooned to 6.8%. The portfolio has entered a death spiral. Withdrawals are too large relative to what's left, and recovery becomes almost mathematically impossible.

Big ERN's CAPE-based formula gives us a sobering reality check. His approach: 1.75% + 0.5 × (1/CAPE). At a CAPE of 41.6, that yields a starting safe withdrawal rate of approximately 2.95%. On a $1 million portfolio, that's $29,500 per year. More than $10,000 less than the 4% rule would suggest.

Ready to stress-test your retirement plan?

See how different withdrawal rates and market conditions affect your portfolio over time with ReadyAimRetire's free calculator.

Run Your Numbers →Edward McQuarrie, a finance professor at Santa Clara University, published research in 2025 that goes even further. He found that "any substantial withdrawal rate that can be supported on one set of historical data can fail if small reductions in return are made to the record, or small increases in inflation added to the record." His conclusion? To achieve near-certain success with a fixed rate, you'd need to cut withdrawals to around 2%. That leaves most retirees with an impractically small income.

The problem isn't the specific percentage. It's the rigidity.

Dynamic Guardrails: The Strategy That Actually Works

OK so if fixed withdrawal rates are broken, what do we use instead? The retirement planning world has pretty much converged on one answer: dynamic withdrawal strategies that adjust spending based on how your portfolio is actually doing.

The most widely cited framework is the Guyton-Klinger guardrails approach. I love it because it's simple enough to explain over coffee. Here's how it works:

- Set a starting withdrawal rate (typically 5.0-5.5%, higher than the static 4% rule because the flexibility gives you a safety margin).

- Define an upper guardrail (your withdrawal rate ceiling, typically 20% above your starting rate).

- Define a lower guardrail (your withdrawal rate floor, typically 20% below your starting rate).

- Adjust when guardrails are breached. If your current withdrawal rate exceeds the upper guardrail, cut spending by 10%. If it drops below the lower guardrail, give yourself a 10% raise.

A 10-Year Guardrails Walkthrough

Let's see this in action with a $1,000,000 portfolio and a 5% starting withdrawal ($50,000). Upper guardrail: 6%. Lower guardrail: 4%.

| Year | Portfolio Value | Withdrawal | Effective Rate | Guardrail Hit? | Action |

|---|---|---|---|---|---|

| 1 | $1,000,000 | $50,000 | 5.0% | No | None |

| 2 | $960,000 | $51,000 | 5.3% | No | None |

| 3 | $800,000 | $52,020 | 6.5% | Upper | Cut 10% to $46,818 |

| 4 | $780,000 | $47,754 | 6.1% | Upper | Cut 10% to $42,979 |

| 5 | $830,000 | $43,838 | 5.3% | No | None |

| 6 | $920,000 | $44,715 | 4.9% | No | None |

| 7 | $1,050,000 | $45,610 | 4.3% | No | None |

| 8 | $1,180,000 | $46,522 | 3.9% | Lower | Raise 10% to $51,174 |

| 9 | $1,220,000 | $52,197 | 4.3% | No | None |

| 10 | $1,300,000 | $53,241 | 4.1% | No | None |

Look at what happened there. This retiree started with $50,000 in income, which is 25% more than the 4% rule would have allowed. They had to tighten their belt for a couple of rough years. But by year 10, they ended up with both higher spending AND a larger portfolio. That's the power of flexibility.

The Kitces Upgrade: Risk-Based Guardrails

Now, the traditional Guyton-Klinger model does have a flaw. Michael Kitces and his research team (specifically Derek Tharp and Justin Fitzpatrick) identified it: the spending cuts can be really painful. Their analysis shows that Guyton-Klinger guardrails produced a 28% spending cut during the 2008 financial crisis, a 36% cut during the dot-com bust, and a staggering 54% cumulative cut during the 1965-1975 stagflation era.

Imagine cutting your retirement income by more than half. That's not a plan. That's a crisis.

The alternative, developed by Tharp and Fitzpatrick on the Kitces platform, uses probability-of-success thresholds rather than simple percentage bands. You start withdrawals when the Monte Carlo probability of success is around 80%. You only increase spending when the probability hits 100%. And you only cut spending when it drops below 25%. This approach produced just a 3% spending cut during the 2008 crisis, compared to Guyton-Klinger's 28%.

The practical difference is huge. Risk-based guardrails protect your lifestyle during market stress while still giving you permission to spend more when conditions are favorable. You get to live your life, not just survive it.

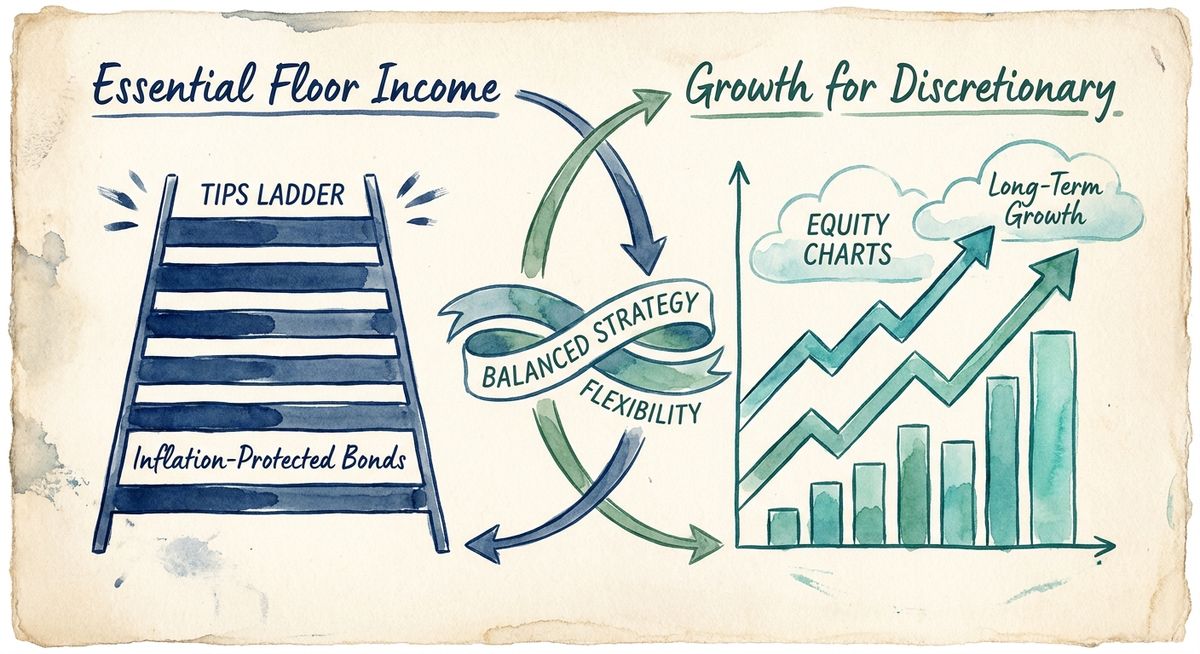

The Floor-and-Upside Framework: Building a Modern Retirement Income Plan

For folks who want to move beyond the 4 percent rule entirely, the most solid retirement spending strategy combines guaranteed income with growth potential. My friend David calls this the "sleep at night" approach, and I think that's pretty accurate.

Step 1: Build a spending floor with TIPS. Treasury Inflation-Protected Securities offer a government-guaranteed real return. As of mid-2026, a 30-year TIPS ladder can sustain approximately 4.7% in annual inflation-adjusted withdrawals based on real yields near 2.5%. On a $500,000 allocation, that's roughly $23,500 per year in purchasing-power-protected income with zero market risk. That covers your essentials.

Step 2: Invest the remainder for growth. The other $500,000 goes into a diversified equity portfolio. This money funds the fun stuff: travel, gifts, nice dinners, spoiling the grandkids. Because your essential expenses are already covered by the TIPS floor, you can ride out market volatility without panic selling. That's a game changer psychologically.

Step 3: Apply guardrails to the equity portion only. Use a dynamic spending rule on just the equity side. If markets soar, you spend more on the extras. If they crash, you scale back the discretionary stuff while your essentials stay completely untouched.

This hybrid approach eliminates the worst-case scenario (running out of money for the things you actually need) while preserving the best-case scenario (enjoying more when markets cooperate).

What About Early Retirees?

If you're planning to retire at 50 or 55, the standard 30-year analysis doesn't apply to you. A 40-50 year retirement horizon requires a more conservative starting rate, around 3.0% to 3.5% under a static model. Big ERN's research, which focuses specifically on early retirement scenarios, is the most thorough resource out there for this group.

Guardrail withdrawal strategies become even more important the earlier you retire. The longer the time horizon, the more chances for sequence-of-returns risk to show up, and the more valuable flexibility becomes. McQuarrie's research suggests that early retirees should also look into partial annuitization. Life annuities may provide an initial payout rate twice as high as a fixed withdrawal rate for the portion of spending they cover. Worth considering, especially for that essentials floor.

Test these strategies with your own retirement timeline.

See how guardrails and different withdrawal rates perform with your specific portfolio and retirement age.

Model Your Plan →Your Retirement Withdrawal Strategy Action Plan

Look, the retirement income landscape in 2026 demands more thought than just plugging 4% into a calculator and calling it a day. Here's what I'd actually do with all this information:

🎯 Action Steps for 2026

- Calculate your CAPE-adjusted starting rate: Use Big ERN's formula: 1.75% + 0.5 × (1/CAPE). At current valuations, that's roughly 2.95% for a fixed rate. If that number makes you uncomfortable, good. It should push you toward flexibility, not a higher fixed rate.

- Adopt a guardrail withdrawal strategy: Start at 5.0-5.2% with dynamic spending rules. Define your upper and lower guardrails, and commit to the adjustments before you need them. Here's the key: deciding to cut spending during a market crash is psychologically brutal. Deciding in advance, as part of a system, is totally manageable.

- Separate essential from discretionary spending: Know exactly what you need to cover housing, food, healthcare, and insurance. Consider covering that floor with TIPS, Social Security (delay to 70 if you can), or a partial annuity.

- Stress-test your plan at today's valuations: Don't assume average historical returns. With CAPE at 41.6, the next decade of equity returns will very likely fall below historical averages. Build your plan around that reality, and let the upside surprise you.

Every retirement plan is different, so test how these strategies work with your specific numbers at ReadyAimRetire.com to see which approach gives you the most confidence.

The 4 percent rule gave a generation of retirees the confidence to stop working. That was its gift. Its limitation was making people think retirement income planning could be reduced to a single number.

In 2026, the retirees who thrive will be the ones who replace that false certainty with a system that bends without breaking.

And honestly, that's not just good financial advice. That's good life advice.

Thanks for reading if you've made it this far. Peace!