Why Most Retirees Die With Too Much Money: The Retirement Spending Confidence Crisis

Here's a number that stopped me cold the first time I saw it. The average 65-year-old couple withdraws just over 2% of their portfolio each year in retirement. That's roughly half of what most financial plans say is safe.

Think about that for a second.

The Employee Benefit Research Institute found that the wealthiest retirees spent down only 11.8% of their non-housing assets over the first 20 years of retirement. And about one-third of all retirees actually increased their wealth after they stopped working.

They saved for decades. They built a portfolio designed to fund 30 years of living. And then they barely touched it.

- Most retirees drastically underspend: Average withdrawal rates are only 2%, vs. the 4%+ that research shows is safe

- Psychological barriers run deep: 64% of Americans fear running out of money more than dying

- Dynamic strategies unlock 20-30% more income: Guardrails and ratcheting approaches safely increase spending

- The goal isn't dying rich: Your retirement plan should give you permission to spend, not just protection from risk

Action: Calculate your funded status to see if you have permission to spend more in retirement.

This isn't a success story. It's a planning failure hiding in plain sight—a crisis of retirement spending confidence that leaves money on the table while life passes by.

The Accumulation Trap

For 30 or 40 years, every financial message you heard pointed in one direction: save more. Max out the 401(k). Build the emergency fund. Watch the balance grow. That discipline got you to retirement. Good on you, seriously. But it also trained your brain to treat spending as the enemy and saving as the only safe behavior.

Then retirement arrives, and the rules flip overnight. The account that was supposed to grow is now supposed to shrink. And almost nobody makes that psychological switch cleanly. I've seen it with my own family. I've seen it with friends. It's remarkably common.

Research Insight

Michael Finke's research reveals that risk-averse retirees systematically underspend to avoid the possibility of cutting back in their 90s—leading to decades of unnecessary frugality.

Michael Finke, one of the leading researchers on retirement spending behavior, has studied this extensively. His finding is fascinating and a little heartbreaking. Risk-averse retirees spend less early in retirement to avoid the possibility of having to cut back in their 90s. The result is systematic underspending across the board. Not because the money isn't there, but because the fear of needing it someday overrides the permission to use it today.

And how deep does this fear run? An Allianz study found that 64% of Americans are more worried about running out of money than they are about dying. Read that again. People would literally rather die than go broke.

So they hoard. They clip coupons on a $2 million portfolio. They skip the trip to Italy. They drive the old car another year. And the portfolio keeps growing while their health, energy, and capacity for enjoyment quietly decline.

That's the part that gets me.

Why the 4% Rule Creates Unnecessary Fear

Bill Bengen introduced the 4% rule back in 1994 as a floor. The worst-case safe withdrawal rate across the ugliest periods in market history. It was never meant to be a spending target. But that's exactly what it became.

Here's what most people miss. According to research from Michael Kitces, a 4% withdrawal rate has a 96% probability of leaving you with more than your starting principal after 30 years. Not just surviving. Growing. The median outcome? You finish with 2.8 times what you started with. In the best historical scenarios, retirees ended with more than 9 times their original balance.

Nine times. Let that sink in.

The 4% Rule Update

Even Bill Bengen himself updated the number. In 2025, he raised his safe withdrawal rate from 4% to 4.7%, citing greater portfolio diversification opportunities. He told CNBC that early retirees using the original 4% rule "may be cheating themselves," recommending closer to 5.25% to 5.5% for today's retirees.

The truth is, the 4% rule is fundamentally broken in 2026 as both a floor and a ceiling for modern retirement planning.

So if you retired with $2 million and have been withdrawing $80,000 a year (4%), you were probably already being too conservative. And if you've been withdrawing $40,000 (2%), like the average retiree? You're likely leaving hundreds of thousands of dollars in unlived experiences on the table.

Let me put that in real terms. A retiree with a $2 million portfolio who withdraws 2% instead of 4% gives up $40,000 per year in spending. Over 20 years, that's $800,000 in trips not taken, dinners not shared, gifts not given, and experiences not had. That's not prudence. That's loss.

Ready to run your own numbers?

See how your retirement plan stacks up with ReadyAimRetire's free retirement calculator.

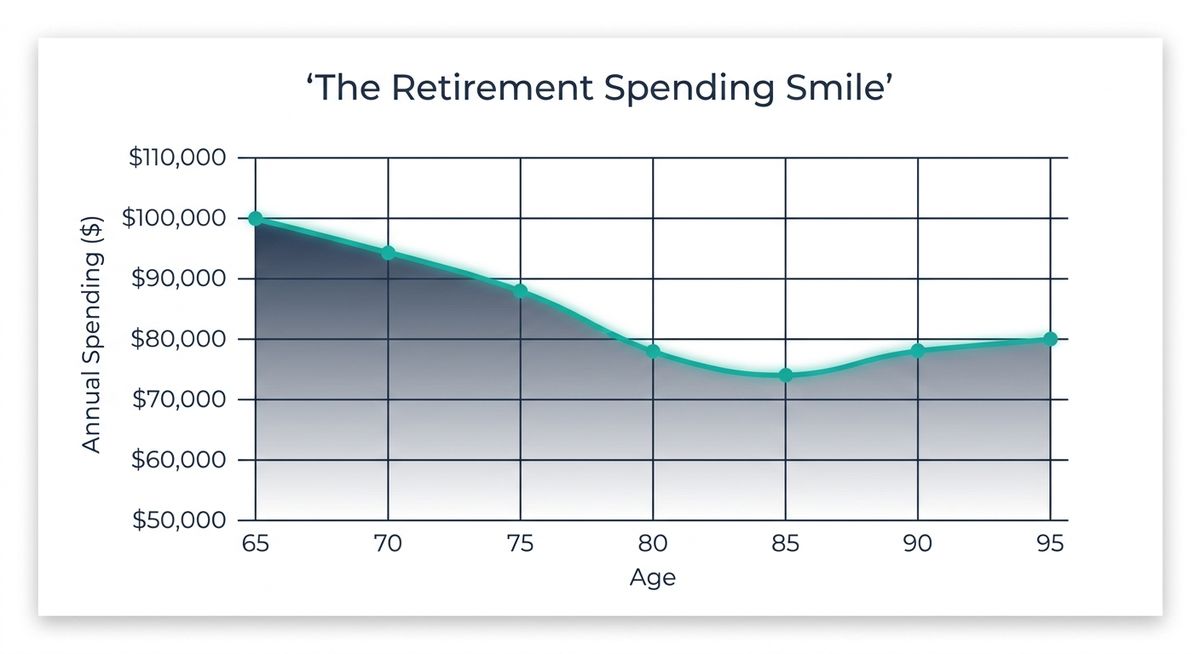

The Retirement Spending Smile

There's another layer here that makes overly cautious planning even more costly. David Blanchett's research on the "retirement spending smile" shows that real spending doesn't stay flat through retirement. It drops.

A retiree spending $100,000 a year at age 65 typically hits a trough of about $74,000 (in real, inflation-adjusted terms) by age 84. That's a 26% decline. Discretionary spending on travel, dining, hobbies, and entertainment falls steadily through your 60s and 70s as energy and mobility naturally decrease. Healthcare costs create a modest uptick in the late 80s and beyond, but the net effect is still a significant real spending decline.

Here's why this matters so much. It means retirees who plan for constant, inflation-adjusted spending over 30 years are almost certainly overfunding their later years at the expense of their early, most active ones. The first five years of retirement are when you're healthiest and most capable of enjoying your money—exactly the years most retirees spend the least.

I think about my friend Stephany in Chicago, who's always telling me about the retired Americans she meets traveling. The ones who finally made it at 78 or 80 and can barely walk the around. They had the money at 65. They just didn't give themselves permission to go.

Your Plan Should Give You Permission, Not Just Protection

Most retirement plans are built around a single question: "Will I run out of money?" That's necessary. But it's not sufficient.

A great retirement plan should answer two questions:

- When am I in danger?

- When am I safe to spend more?

If your plan only answers the first question, you'll default to fear. You'll underspend. And you'll join the growing ranks of retirees who become, as the saying goes, the richest person in the graveyard.

Understanding Funded Status

Funded status is borrowed from pension fund management. You divide your total assets by the total cost of funding your retirement goals. A ratio above 1.0 means you're fully funded. A ratio of 1.4 means you have a 40% surplus—a concrete signal you have permission to spend more.

This is where funded status becomes really powerful. It's borrowed from pension fund management, and the concept is simple. You divide your total assets by the total cost of funding your retirement goals (including longevity, healthcare, and legacy). A ratio above 1.0 means you're fully funded. A ratio of 1.4 means you have a 40% surplus.

Wade Pfau and other researchers have written about applying this framework to individual retirement plans. It strips away the complexity of Monte Carlo simulations and gives you a single, intuitive number. When your funded ratio is well above 1.0, that's a concrete signal. You have permission to spend more, reduce risk, or both. Tools like ReadyAimRetire can help you calculate your personal funded ratio and see exactly when you have permission to spend more.

Imagine a retiree with a funded ratio of 1.4 who's still only withdrawing dividends and interest. Their advisor runs the numbers and shows them: "You could spend $20,000 more per year, your funded ratio would still be above 1.0 at age 95, and your legacy goal is fully covered." That number isn't just math. It's a permission slip.

I love that framing. Because so many people I talk to don't need more money. They need permission.

Dynamic Withdrawal Strategies That Give You Raises (and Protection)

Static withdrawal rules treat your spending like a fixed contract. You pick a number at retirement and adjust for inflation forever, regardless of what the market does. That's simple, but it's wasteful in good times and dangerous in bad ones.

Dynamic withdrawal strategies solve this by adjusting your spending based on how your portfolio is actually performing. Two approaches really stand out—and both can help you increase your retirement income safely.

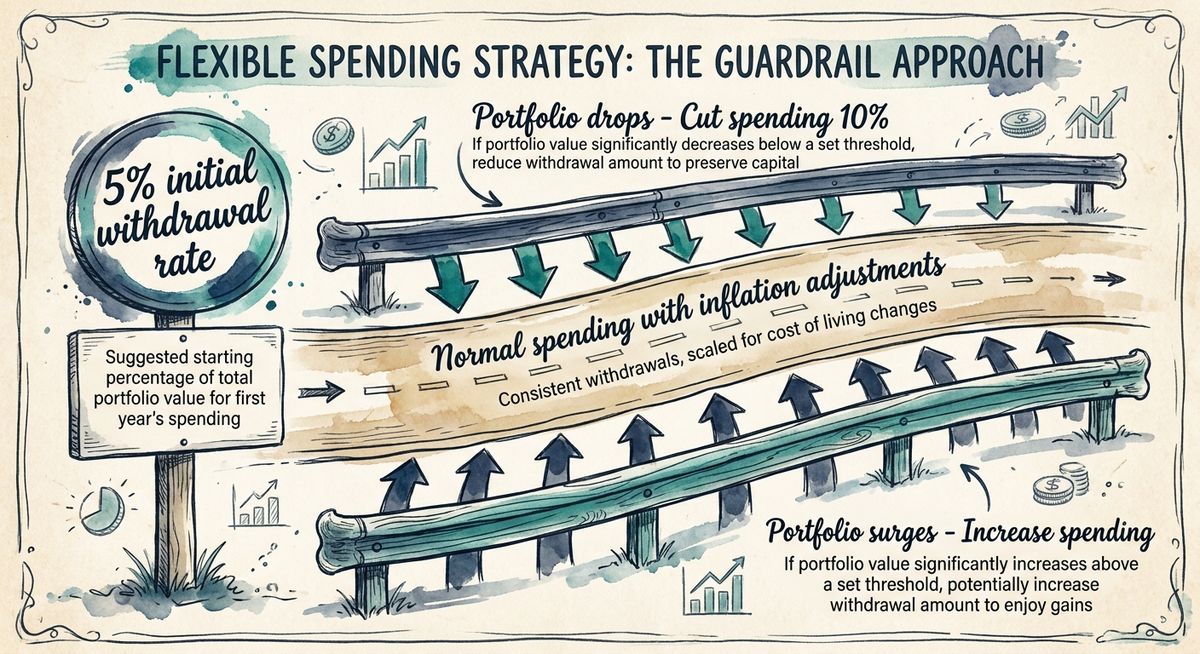

Guyton-Klinger Guardrails

The guardrails approach sets an initial withdrawal rate (often around 5%, significantly higher than the 4% rule) with built-in speed bumps. If your portfolio drops enough that your effective withdrawal rate climbs above an upper guardrail, you cut spending by 10%. If markets surge and your rate falls below a lower guardrail, you give yourself a raise.

According to Morningstar's research, a guardrails-based dynamic withdrawal approach supports a starting rate of 5.2%. That's roughly 30% more retirement income than traditional fixed approaches. Over a full retirement, the cumulative difference in spending is enormous.

The Kitces Ratcheting Strategy

My man Michael Kitces proposed something even more psychologically satisfying. A strategy where you get spending raises but never take cuts. Yes, you read that right.

Here's how it works. You start at the traditional 4% withdrawal rate. Every three years, you check your portfolio. If it's grown to more than 50% above its starting value, you give yourself a 10% spending raise on top of your normal inflation adjustments. Once a raise is given, it's permanent. You never cut back.

Traditional 4% Rule

- Withdrawal Rate Fixed 4%

- Adjustments Inflation only

- Spending Changes No raises, no cuts

- Approach Conservative but static

Kitces Ratcheting

- Withdrawal Rate Start 4%, get raises

- Adjustments 10% raise after 50% growth

- Spending Changes Raises are permanent

- Approach Higher lifetime spending

Kitces' analysis shows this approach "dominates" the traditional 4% rule, generating equivalent or better spending in every historical scenario while maintaining the same safety floor. The key insight is that because you only ratchet up after a 50% portfolio increase, the surplus is large enough that even a subsequent bear market won't threaten the plan.

For the retiree who started with $2 million and is withdrawing $80,000 per year, a ratchet after six years of strong returns might bump that to $88,000 (plus cumulative inflation adjustments). That's the trip to Italy. That's the kitchen renovation. That's saying yes instead of "maybe next year."

And that feels good.

You can model both guardrails and ratcheting strategies with your own portfolio at ReadyAimRetire.com to see which approach fits your risk tolerance and spending goals.

However, there's one major risk to consider: sequence of returns risk in your early retirement years. Bad market timing in your first five years can destroy decades of careful planning, which is why dynamic strategies build in these guardrails.

Why Guaranteed Income Changes Spending Behavior

Research from Blanchett and Finke (2025) uncovered something striking about how retirees mentally categorize their money. Retirees spend roughly 80% of their guaranteed, lifetime income sources (Social Security, pensions, annuities) but only about 50% of their portfolio savings.

This isn't rational, right? A dollar is a dollar regardless of where it comes from. But our brains don't work that way. Money from Social Security feels like a paycheck, safe to spend. Money from a brokerage account feels like a safety net, dangerous to touch.

Behavioral Finance Finding

Retirees with 60% to 80% of wealth in guaranteed income spend 42% more than those with less than 20% guaranteed. Each dollar converted to guaranteed income produces roughly twice the equivalent spending.

The practical implication is significant. Retirees with 60% to 80% of their wealth in guaranteed income spend 42% more than those with less than 20% in guaranteed income. Each dollar converted to guaranteed income produces roughly twice the equivalent spending. For retirees who are sitting on large portfolios but still can't bring themselves to spend, converting a portion to annuity income isn't just a financial decision. It's a behavioral unlock.

I think that's really interesting. Sometimes the best financial move isn't about optimizing returns. It's about working with your own psychology instead of against it.

What This Means for You

If you're approaching retirement or already in it, here are the questions worth sitting with.

Check your funded status. What's your total asset picture relative to what you actually need? If you're well above 1.0, that's data, not a feeling. Use it.

Reconsider static withdrawal rules. The 4% rule was a floor, not a ceiling. If you've been using it as your spending target, you've likely been underspending for years. Dynamic approaches like guardrails or the ratcheting strategy can safely unlock 20% to 30% more lifetime spending.

Audit your first five years. Sequence-of-returns risk is real and concentrated in the early years of retirement. If you're past that window and your portfolio has held up (or grown), the biggest risk to your plan has already passed. Act like it.

Know exactly how much you need. Whether you're planning to retire at 55, 60, 65, or 70, understanding your true number gives you the confidence to spend appropriately.

Think about what you're optimizing for. Bill Perkins, author of Die With Zero, frames it well. If you die with money left over, it represents years you spent working for free, earning wealth you never got to use. The roughly $90 trillion "Great Wealth Transfer" expected over the next two decades is, in many cases, money that could have funded richer lives for the people who earned it.

Get a second opinion from your future self. At 85, will you wish you had a larger portfolio? Or will you wish you had taken that trip, hosted that gathering, or been more generous when you had the health to enjoy it?

Start by running your own retirement projections at ReadyAimRetire.com to see where you stand today and test different spending scenarios with your actual numbers.

I think most of us know the answer to that one.

The Goal Isn't to Die Rich

The retirement planning industry has spent decades perfecting the answer to one question: "How do I avoid running out of money?" That question matters. But for most retirees, it's already answered. Their plans are working. Their portfolios are growing. Their risk of ruin is vanishingly small.

The question they actually need answered is different. "When is it safe to spend more?"

If your retirement plan can't answer that, it's only doing half its job. Sustainable retirement income isn't just about protection. It's about permission. It's about actually living the years you worked so hard to fund.

Because the goal was never to die with the largest portfolio possible.

The goal was to maximize your life.

Thanks for reading!

🎯 Your Next Steps

- Calculate your funded status - Use ReadyAimRetire's free calculator to see if you're over-saving

- Model dynamic withdrawal strategies - Test guardrails and ratcheting approaches with your numbers

- Review your first 5 years - If you're past early retirement sequence risk, adjust accordingly

- Consider guaranteed income - Explore converting part of your portfolio to annuity income for psychological comfort