How to Retire in Your 50s: 6 Essential Early Retirement Planning Strategies

Only 6% of Americans successfully retire in their 50s between ages 50 and 54. Another 11% manage it between 55 and 59. Add those up and you've got roughly one in six people who actually leave work in their 50s.

That's a pretty exclusive club.

Early retirement in your 50s requires different math than traditional retirement planning:

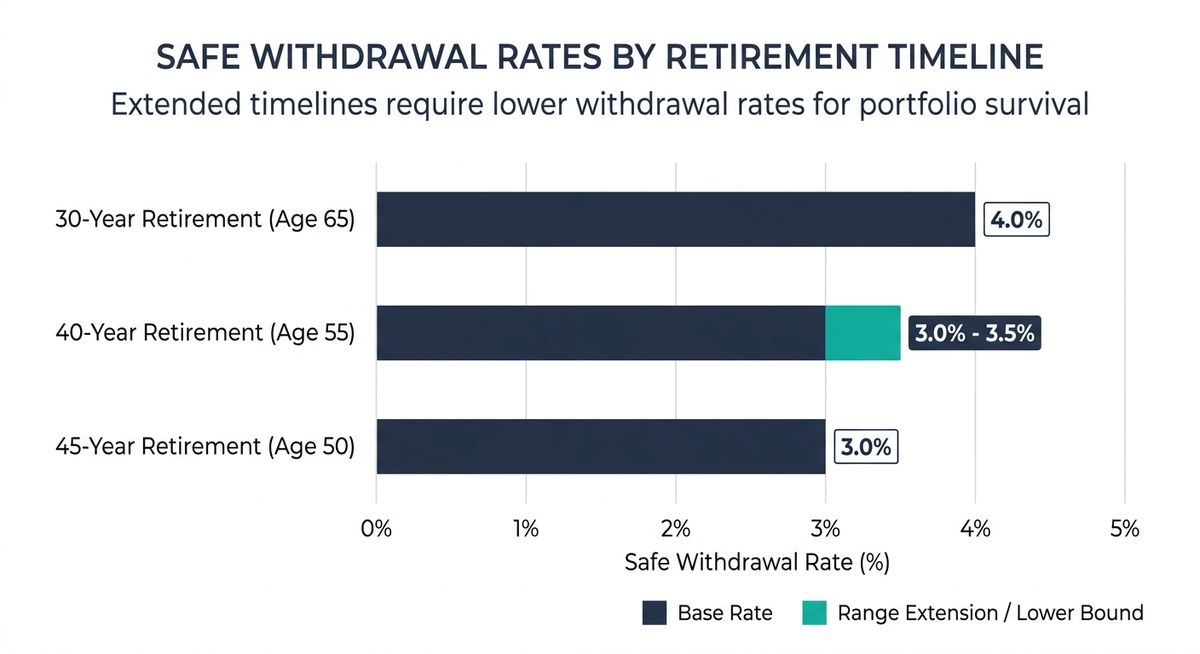

- Lower withdrawal rates: Plan for 3-3.5% instead of 4% to survive 40+ year timelines

- Healthcare is critical: A decade without Medicare requires strategic income planning around ACA subsidies

- Flexibility beats perfection: Ability to adjust spending and earn bridge income matters more than a huge portfolio

- Tax sequencing wins big: The order you withdraw from accounts can save six figures over retirement

Bottom line: Success comes from quality planning that accounts for the unique challenges of a 35-45 year retirement.

And here's the thing. The majority who don't make it aren't always broke. A lot of them saved plenty. They just planned for a version of retirement that doesn't exist when you're 55.

Think about it. Traditional retirement advice assumes you'll start collecting Social Security within a few years. It assumes Medicare will handle your health costs. It assumes your portfolio only needs to last about 30 years. Retire in your 50s, and literally none of that applies.

You're looking at a 35- to 45-year retirement. A decade or more without employer health insurance. A tax landscape that will absolutely punish you if you're not paying attention. And a psychological shift that catches people off guard more than any market crash ever could.

My friend David put it well when he left his corporate job at 54: "I spent two years planning the money part. I spent zero time planning the 'what do I do on a Tuesday' part."

Here are six moves that separate the people who actually retire in their 50s from those who just daydream about it at their desks.

1. Stop Trusting Your "Retirement Number"

You've probably seen some version of this advice. Multiply your annual expenses by 25, and that's your magic number. If you spend $60,000 a year, you need $1.5 million. Simple. Clean. Done.

Except it's not done. Not even close.

That formula is built on the 4% rule, which was designed for a 30-year retirement starting at 65. Stretch that timeline to 40 or 45 years, and the safe withdrawal rate drops to roughly 3% to 3.5%. Suddenly your $1.5 million target becomes $1.7 million to $2 million.

But even that adjusted number hides problems. It assumes your spending stays flat. And it won't.

Healthcare costs have consistently risen at roughly double the rate of general inflation, averaging around 4.5% to 5% per year over the past three decades compared to about 2.5% for overall consumer prices. At just 3% overall inflation, $60,000 in annual spending requires roughly $145,000 to buy the same goods 30 years later. Medical costs will outpace even that.

Research Reality Check

University researchers analyzed 36 widely used retirement calculators and found that more than two-thirds produced overly optimistic projections. The core problem? They assume flat market returns, understate healthcare costs, and use life expectancy figures that don't account for the fact that a healthy 55-year-old has genuinely solid odds of living into their 90s.

As detailed in Why the 4% Rule is Broken in 2026 (And the New Formula That Actually Works), a single retirement number gives you false confidence. What you actually need is a spending plan that accounts for different phases. Higher spending in your early, active years. Lower spending in your mid-70s. And potentially much higher spending again if long-term care enters the picture. You need a realistic healthcare cost trajectory. And you need a withdrawal rate your portfolio can survive for four decades, not three.

Action Steps: Recalculate Your Number

- Replace your single target: Calculate needs at both 3.5% and 3% withdrawal rates

- Build in healthcare inflation: Use 5% annually for medical costs, not 3%

- Embrace the discomfort: If these numbers feel uncomfortable, use that as useful planning information

2. Close the Healthcare Gap Before It Closes Your Options

This is the risk that derails more early retirements than market crashes. I've seen it happen. Retire at 55, and you face a full decade without Medicare. That's 10 years of finding and funding your own health insurance.

And as of 2026, the math just got significantly worse.

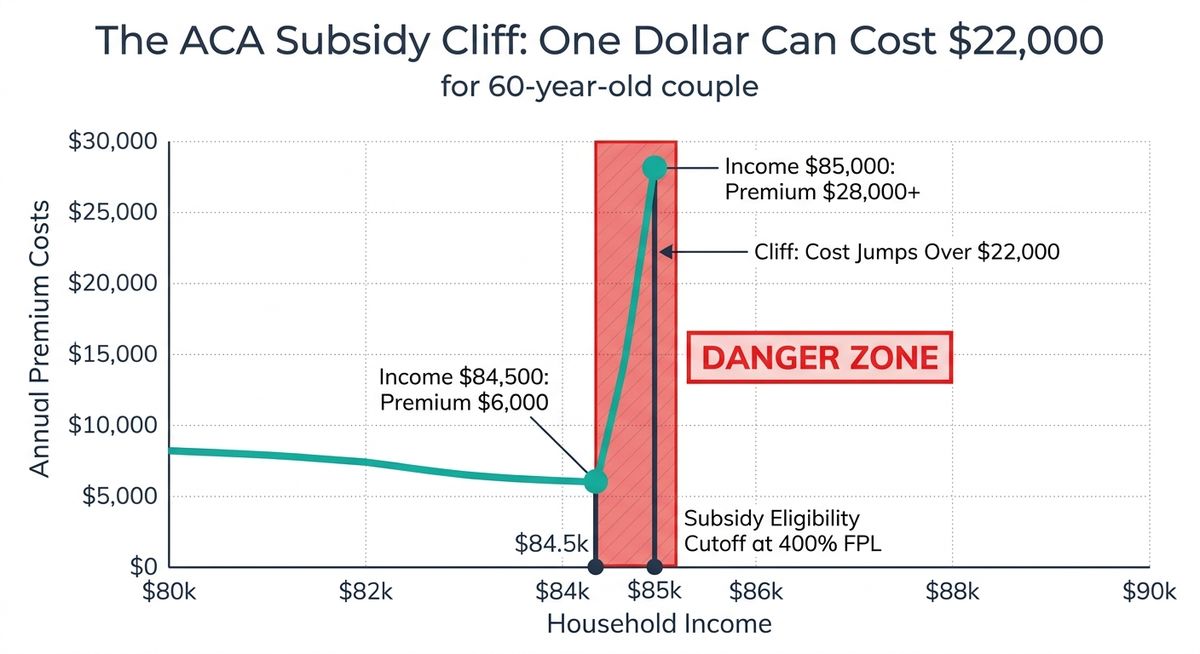

The enhanced ACA subsidies that kept marketplace premiums manageable expired at the end of 2025. The subsidy cliff at 400% of the federal poverty level ($62,600 for an individual, $84,600 for a couple) is back in full force. And this isn't some edge case for early retirees. According to KFF, 51% of ACA enrollees with incomes above that cliff are between ages 50 and 64. This is the central demographic. This is you, if you're reading this article.

Here's what the cliff looks like in practice. An average 60-year-old faces ACA premiums of roughly $1,244 per month without subsidies. For a couple both around 60 earning $85,000 (just $400 above the cliff), annual premiums can exceed $28,000. A couple earning $84,500 might pay closer to $6,000.

Read that again. One dollar of income across that threshold can cost you over $22,000 in healthcare premiums.

I'll be honest, the first time I saw those numbers I thought there had to be a typo. There wasn't.

Below the ACA Cliff

- Income (Couple, Age 60) $84,500

- Annual Premium ~$6,000

- Monthly Cost $500

- Effective Healthcare Rate 7.1%

Above the ACA Cliff

- Income (Couple, Age 60) $85,000

- Annual Premium ~$28,000

- Monthly Cost $2,333

- Effective Healthcare Rate 32.9%

For those considering part-time work as a bridge strategy, maintaining employer health benefits can be worth the equivalent of $20,000+ in annual value. Fidelity estimates that a 65-year-old retiring in 2025 needs approximately $172,500 just for medical expenses in retirement. And that figure starts at Medicare eligibility. It doesn't include the decade before you qualify.

Healthcare Strategy Essentials

- Learn your thresholds: Understand ACA subsidy limits and how MAGI affects premium credits

- Plan withdrawals around healthcare: Build annual withdrawal strategy to stay below the cliff

- Consider bridge employment: Part-time work with health benefits can be worth $20k+ annually

3. Build Flexibility Into Your Early Retirement Strategy

Most retirement planning focuses on accumulation. Save more. Invest better. Hit your number. But research on early retirees who actually succeed points to a different advantage that matters more than portfolio size.

Flexibility.

The ability to reduce spending by 10% to 15% during a market downturn. The willingness to earn bridge income through part-time work or consulting. The option to relocate to a lower-cost area. These capabilities can be worth the equivalent of hundreds of thousands of dollars in additional savings.

Real-World Example: Rosa's Barcelona Move

My friend Rosa left her marketing career at 53 without what most advisors would call "enough." But she had options. She could freelance, relocate (London to Barcelona, cutting costs nearly in half), and adjust spending based on portfolio performance. That flexibility was worth more than another $300,000 in savings.

Consider the "Barista FIRE" approach explored in The different flavors of FIRE. A 52-year-old tech worker with $1.2 million saved (about 80% of their full retirement number) shifts to part-time consulting at $45,000 a year. The consulting income covers living expenses. Their portfolio grows untouched. They potentially maintain access to employer health benefits. And they reach full financial independence by 57, all while already living a semi-retired life.

That's not a consolation prize. That's a strategy.

Dynamic withdrawal strategies reinforce this too. Instead of withdrawing a fixed 3.5% every year regardless of market conditions, "guardrail" methods set upper and lower boundaries. Say, 5% in good years and 3% in bad ones. You spend more when your portfolio is thriving and pull back when it's stressed. Research consistently shows these flexible approaches outperform rigid withdrawal rates over long time horizons.

Build Your Flexibility Levers

- Geographic flexibility: Research lower-cost areas you'd genuinely enjoy living

- Income flexibility: Develop consulting or part-time work options in your field

- Spending flexibility: Identify which expenses you can cut 15% without major lifestyle impact

- Withdrawal flexibility: Use guardrail strategies instead of fixed percentages

4. Sequence Your Income Sources (The Order Matters More Than the Amount)

Most people think about retirement income as a pool. Social Security plus savings plus maybe a pension. But when you retire in your 50s, the *sequence* of which accounts you draw from, and when, can save or cost you six figures over a 30-year retirement.

Here's why. The years between 55 and your mid-60s are likely your lowest-income years. You're not collecting Social Security yet. You may not have Required Minimum Distributions forcing money out of tax-deferred accounts. This creates a rare window for tax-bracket arbitrage that disappears once those income sources kick in.

It's like finding a coupon that expires. Use it or lose it.

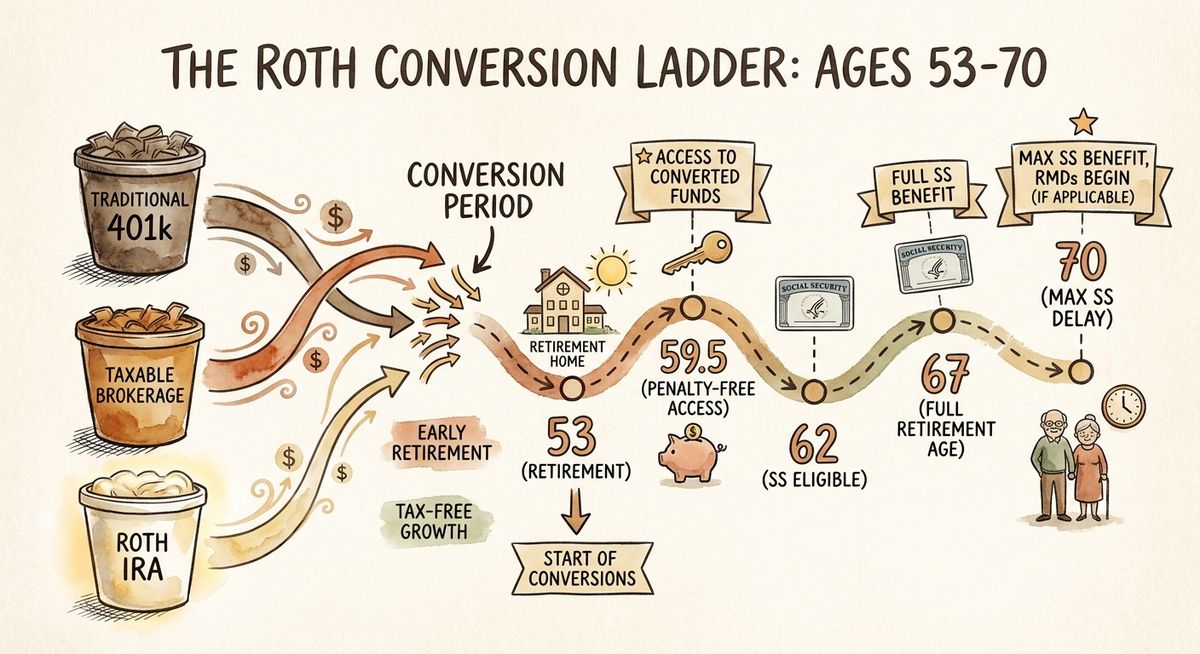

The Roth conversion ladder is a prime example detailed in Roth Conversion Strategies: When and How to Convert for Maximum Benefit. Say you retire at 53 with $800,000 in a traditional 401(k), $300,000 in a taxable brokerage account, and $100,000 in a Roth IRA. During years 53 to 58, you live off the taxable account and existing Roth contributions while converting roughly $50,000 per year from the traditional 401(k) to a Roth IRA. You pay taxes on those conversions, but at the 12% bracket instead of the 22% or 24% bracket you'd face once Social Security and RMDs stack up later.

Each conversion starts its own five-year clock. By 59½, the age-based penalty exception kicks in and all converted funds become available penalty-free. Your remaining traditional balance is significantly smaller, reducing future RMDs at age 75. And you've locked in historically low tax rates on money that will now grow and be withdrawn tax-free.

Pretty cool, right?

The Three-Dimensional Puzzle

Income sequencing isn't just a tax strategy. Those Roth conversions increase your MAGI. Convert too much, and you blow past the ACA subsidy cliff. Convert too much after 63, and you trigger IRMAA surcharges on Medicare premiums two years later. Healthcare costs, tax brackets, and account access rules all constrain each other.

Social Security fits into this sequence too. As covered in When Should You Claim Social Security? The Age-by-Age Breakdown, claiming at 62 reduces your benefit by 30% permanently (for those with a full retirement age of 67, which includes anyone born in 1960 or later). Every year you delay past your full retirement age, up to 70, increases your benefit by 8%. The "bridge strategy" of funding expenses from other sources while letting Social Security grow is one of the highest-return, lowest-risk moves available to an early retiree.

An 8% guaranteed return. I'll take that over just about anything else on the table.

Income Sequencing Roadmap

- Map your timeline: Chart income sources year by year from retirement through age 75

- Identify conversion windows: Find years with penalty-free access and low tax brackets

- Coordinate with healthcare: Balance conversions with ACA subsidy thresholds

- Maximize Social Security: Use bridge strategy to delay claiming for 8% annual increases

5. Build Your Identity Before You Leave Your Job Title

Here's the part no spreadsheet can solve.

In a John Hancock survey, 75% of early retiires said they wished they'd saved more. But the second most common regret isn't financial at all. It's the loss of purpose, structure, and identity that work provided.

I think about this one a lot. As someone who's worked remotely from dozens of countries, I've had little previews of what unstructured time feels like. And I'll tell you, the freedom is incredible for about two weeks. Then you start wondering why you're eating lunch at 10:30 AM and watching your fourth episode of something you don't even like.

The Research on Identity Transition

A seven-year longitudinal study published in *The Gerontologist* found that retirees who proactively developed new identities showed significantly better psychological adjustment than those who tried to hold onto their professional identity or simply drifted. University of Southern California research found that retirees with moderate daily routines (not rigid schedules, not total chaos) reported 31% higher life satisfaction.

This isn't about "finding hobbies." It's about answering a question most people avoid until it's too late: if you're not a [job title] anymore, who are you?

The concept of "practice retirement" is gaining traction for good reason. Before fully leaving work, take an extended leave, a sabbatical, or shift to part-time. Use that time to test whether the life you've imagined actually feels like the life you want. Many people discover that their fantasy of "doing nothing" loses its appeal within weeks.

Identity Development Strategies

- Start early: Begin building post-work identity at least a year before leaving

- Create structure: Develop routines and commitments outside your career

- Build community: Join groups, volunteer, take on projects that connect you with others

- Test drive retirement: Take extended leave or sabbatical before fully committing

6. Stress-Test Your Plan Until It Breaks

A retirement plan that works under average conditions is a plan that fails under real ones. And real conditions are what you'll face.

Most financial planning tools run Monte Carlo simulations, randomizing market returns across thousands of scenarios to estimate your odds of success. That's a start. But it's not enough. Monte Carlo tells you how your plan handles random market variation. It doesn't tell you how it handles a healthcare emergency in year two, a parent who needs full-time care, a divorce, or a prolonged stretch of stagflation.

The 77% Rule: Why Timing Is Everything

Wade Pfau's research reveals that approximately 77% of a portfolio's final outcome is determined by returns in just the first 10 years. If a major market decline hits right after you retire, even a strong recovery may not save you.

As explained in The Silent Retirement Killer: How Bad Market Timing in Your First 5 Years Can Destroy 30 Years of Savings, two people can both retire at 55 with $1.5 million, withdraw the same amount each year, and experience identical average returns over 30 years. If Person A gets hit with a crash early and Person B gets that same crash late, Person B ends up with $2.1 million while Person A runs out of money entirely.

Same savings. Same spending. Same average returns. Completely different outcomes. That's sequence of returns risk, and it's the thing that should keep early retirees up at night (but usually doesn't, because most people don't know about it).

| Stress Test Scenario | What Breaks First? | Contingency Plan |

|---|---|---|

| 30% market drop in year 1 | Portfolio depletion by year 20 | Reduce spending 15%, delay Social Security to 70 |

| Healthcare costs double | Budget exceeded by $15k annually | Return to part-time work, relocate to lower-cost area |

| 5% inflation for 10 years | Real purchasing power cut in half | Flexible withdrawal rate, geographic arbitrage |

| Long-term care needed | $80k+ annual costs not covered | Long-term care insurance, family support plan |

Financial planners generally recommend targeting at least an 85% Monte Carlo success rate. But the better question is: what does your plan look like at 70% or 60%? What breaks first? Where does the money run out? Those failure points are where your contingency plans need to be strongest.

Stress Testing Framework

- Run specific scenarios: Test market crashes, healthcare emergencies, inflation spikes

- Find failure points: Identify what breaks first in each scenario

- Build contingencies: Decide in advance what you'll do when plans fail

- Accept lower success rates: Plan for 70-75% success, not just 85%+

The Real Difference

The gap between people who retire in their 50s and people who just dream about it isn't always the size of their portfolio. It's the quality of their planning.

The ones who succeed account for a decade without Medicare, a tax system that rewards the informed, a market that doesn't care about their timeline, and a life that needs more than financial security to feel worth living.

Early retirement planning changes the math. All of it. Make sure your plan reflects the math that actually applies to you, not the version designed for someone retiring at 65 with a pension and Medicare card in hand. Start with these six moves, pressure-test every assumption, and build in the flexibility to adapt when reality diverges from your projections.

Because it will diverge. That's not a risk. That's a guarantee. And honestly, that's exactly the point of planning.

Thanks for reading if you've made it this far. Peace!