The Inflation-Proof Retirement: How to Build a Portfolio That Actually Keeps Up with Rising Costs

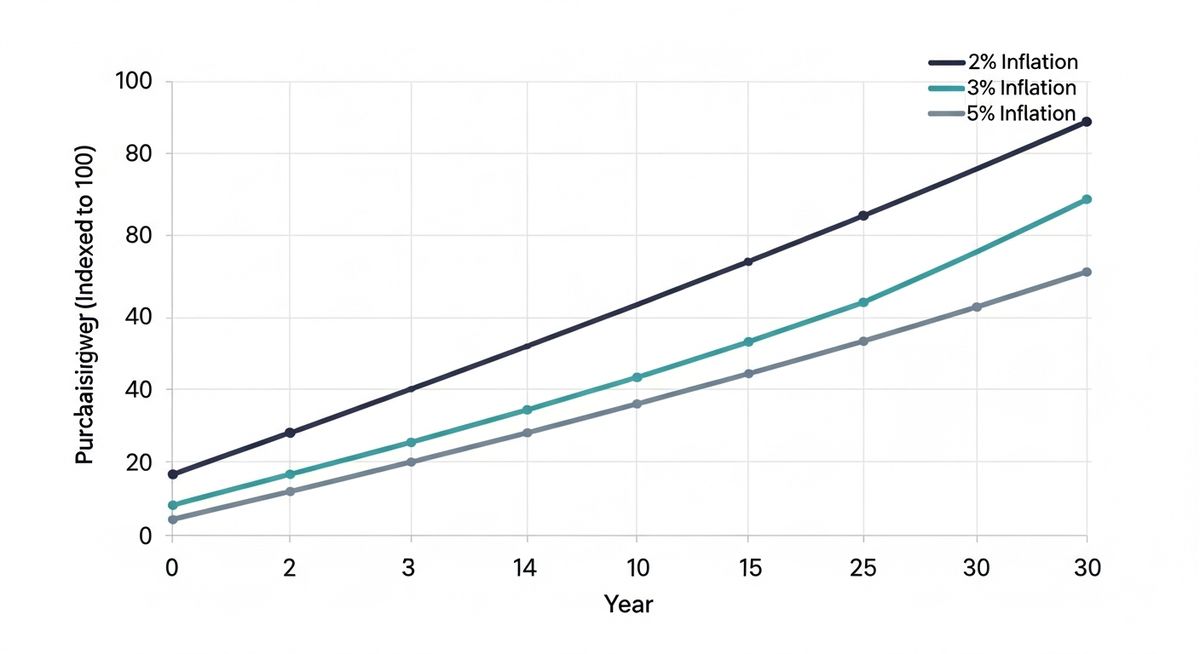

Inflation is the silent retirement killer. While you're focused on growing your nest egg, rising prices are quietly eroding its purchasing power. A $1 million portfolio that seems sufficient today will feel like $400,000 in 30 years if inflation averages just 3%. Here's how to fight back with a portfolio that actually keeps up.

Inflation protection requires more than just "stocks for the long haul." Here's your action plan:

- Diversify beyond traditional 60/40: Add TIPS, REITs, commodities, and international exposure

- Focus on real returns: Target 7% nominal returns to achieve 4% after 3% inflation

- Rebalance quarterly: Inflation hedges perform differently across economic cycles

- Start now: Inflation compounding works against you—every year of delay costs more

Bottom line: A 60-year-old needs 25-30% inflation-hedged assets to maintain purchasing power through retirement.

The Inflation Math That Keeps Financial Planners Up at Night

Here's the brutal reality: 3% annual inflation doubles your cost of living every 23 years. That morning coffee that costs $4 today will cost $8 when you're 23 years deeper into retirement. Your grocery bill, healthcare costs, utilities—everything doubles.

The Real Impact

Inflation at 3% annually: A retiree spending $60,000 today will need $120,000 to maintain the same lifestyle in 23 years. Their million-dollar portfolio needs to grow to $2 million just to break even—and that's before accounting for withdrawals.

Traditional retirement planning assumes you'll spend less as you age. Wrong. Healthcare costs rise faster than general inflation. Many retirees spend more in their 70s than their 60s, not less.

Beyond the 60/40 Portfolio: Assets That Fight Inflation

The traditional 60% stocks, 40% bonds portfolio was built for a low-inflation world. When inflation heats up, bonds get crushed and growth stocks often stumble. You need assets that benefit from rising prices.

Treasury Inflation-Protected Securities (TIPS)

TIPS are the only investment guaranteed by the U.S. government to keep pace with inflation. The principal adjusts upward with the Consumer Price Index, ensuring your purchasing power stays intact.

TIPS Sweet Spot

Allocate 10-15% of your portfolio to TIPS. They won't make you rich, but they'll preserve wealth when everything else is getting hammered by inflation.

Real Estate Investment Trusts (REITs)

Real estate historically outpaces inflation because property values and rents rise with costs. REITs give you real estate exposure without the hassle of being a landlord.

Equity REITs

- Own Properties Directly

- Income Source Rent collection

- Inflation Hedge Excellent

- Target Allocation 8-12%

Mortgage REITs

- Own Properties Mortgages

- Income Source Interest payments

- Inflation Hedge Poor

- Target Allocation 2-3%

Dividend Growth Stocks

Companies that consistently raise dividends tend to have pricing power—they can pass inflation costs to customers. Think Coca-Cola, Johnson & Johnson, Procter & Gamble.

The best inflation hedge isn't gold or commodities—it's owning pieces of businesses that can raise their prices.

| Company | Years of Dividend Increases | Current Yield | Avg. Annual Increase |

|---|---|---|---|

| Johnson & Johnson | 61 years | 2.9% | 6.1% |

| Coca-Cola | 60 years | 3.1% | 3.8% |

| Procter & Gamble | 66 years | 2.5% | 4.2% |

| McDonald's | 46 years | 2.2% | 7.9% |

International Exposure

U.S. inflation isn't global inflation. When the dollar weakens (often during inflationary periods), international investments provide natural currency hedging. Emerging markets often perform well during commodity booms.

Commodities and Natural Resources

When prices rise, someone's making more money selling raw materials. Energy companies, mining stocks, and commodity funds directly benefit from higher prices.

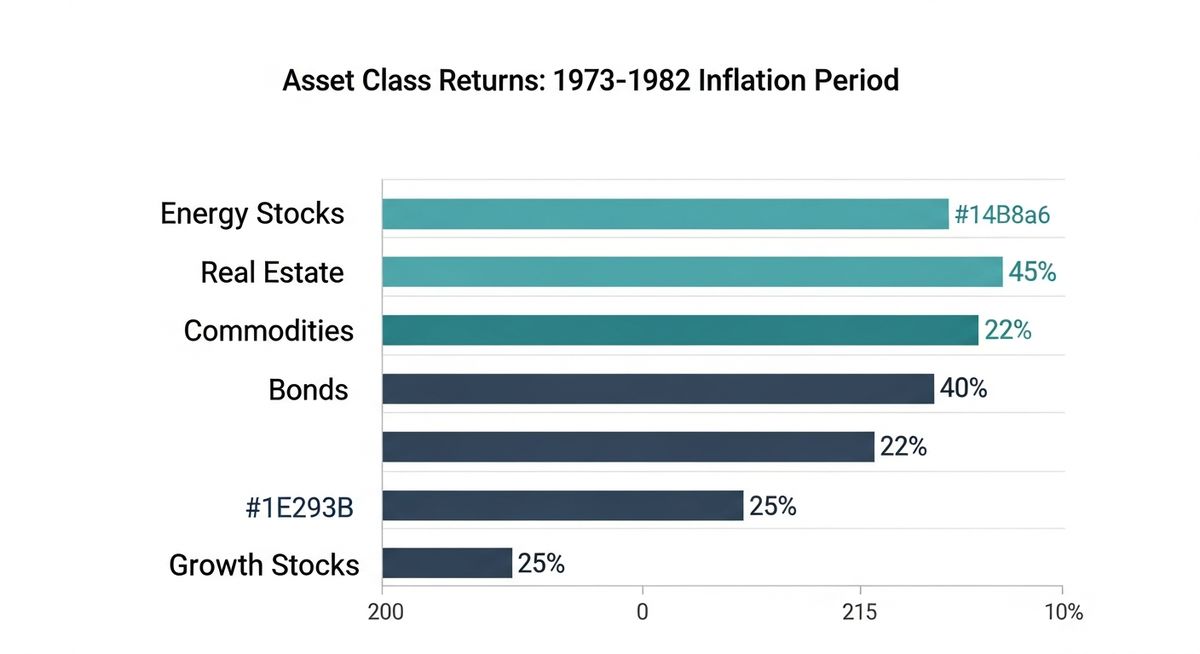

The 1970s Playbook: Lessons from the Last Major Inflation

The last time America faced persistent inflation was the 1970s. From 1973-1982, inflation averaged over 8% annually. Here's what worked and what didn't:

What Worked in the 1970s

Energy stocks: Oil companies saw massive profits as energy prices soared. Real estate: Property values rose with inflation while mortgage payments stayed fixed. Gold and commodities: Hard assets preserved purchasing power. Foreign stocks: International diversification helped as the dollar weakened.

What Failed in the 1970s

Bonds: Long-term Treasury bonds lost 40% of their purchasing power. Growth stocks: High-multiple stocks got crushed as interest rates rose. Cash: Money market rates couldn't keep up with inflation peaks.

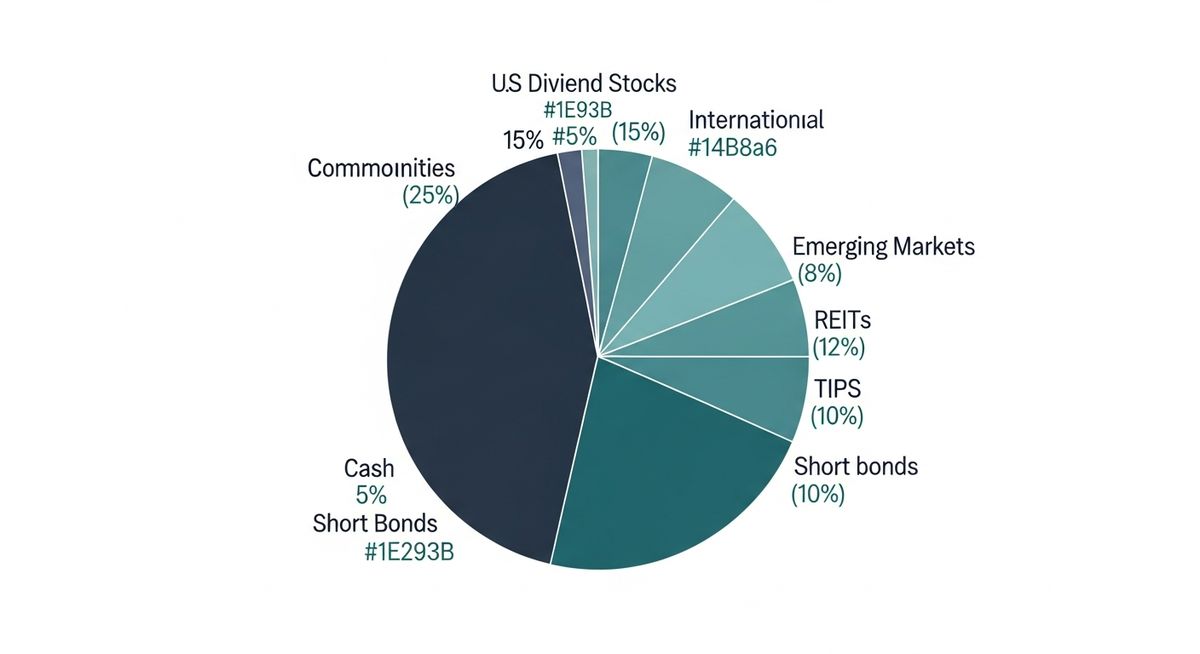

Sample Inflation-Resistant Portfolio for a 60-Year-Old Retiree

Here's a practical allocation that balances growth, income, and inflation protection for someone entering retirement:

| Asset Class | Allocation | Purpose | Inflation Protection |

|---|---|---|---|

| U.S. Dividend Growth | 25% | Income + Growth | High |

| International Developed | 15% | Diversification | Medium |

| Emerging Markets | 8% | Growth + Currency | High |

| REITs | 12% | Real Estate Exposure | High |

| TIPS | 15% | Inflation Insurance | Perfect |

| Commodities/Energy | 10% | Hard Asset Exposure | High |

| Short-term Bonds | 10% | Liquidity | Low |

| Cash/Money Market | 5% | Emergency Fund | None |

Expected Portfolio Performance

This allocation targets 6-7% annual returns with significantly better inflation protection than traditional portfolios. During high-inflation periods, the inflation-resistant components should offset losses in traditional assets.

Implementation Strategy: How to Transition Your Portfolio

Don't overhaul everything at once. Inflation hedging is about balance, not panic. Here's how to gradually build inflation resistance:

Phase 1: Foundation (Months 1-3)

- Add TIPS allocation: Start with 10% in a TIPS fund or individual securities

- Increase REIT exposure: Add 8-10% in a broad REIT index fund

- Review dividend stocks: Shift from growth to dividend-focused funds

Phase 2: Diversification (Months 4-6)

- Add international exposure: Boost developed and emerging market allocations

- Consider commodities: Add 5-8% in commodity funds or energy stocks

- Reduce bond duration: Shift to shorter-term bonds or floating-rate funds

Phase 3: Fine-tuning (Months 7-12)

- Quarterly rebalancing: Maintain target allocations as markets move

- Tax-loss harvesting: Use market volatility to optimize tax efficiency

- Monitor and adjust: Track real returns vs. nominal returns

Monitoring Your Inflation Protection

Success isn't measured by portfolio growth alone—it's about maintaining purchasing power. Track these key metrics quarterly:

| Metric | Target | Why It Matters |

|---|---|---|

| Real Return | 4%+ annually | Grows wealth after inflation |

| Income Growth | Matches CPI | Maintains spending power |

| Correlation to Inflation | Positive | Portfolio rises with prices |

| Maximum Drawdown | <20% | Preserves principal |

Red Flag Indicators

When to adjust: If your real returns (after inflation) turn negative for two consecutive quarters, if income from your portfolio isn't growing with inflation, or if inflation expectations are rising faster than your portfolio's inflation-sensitive allocations.

The goal isn't to time inflation perfectly—it's to build a portfolio that thrives regardless of whether inflation runs 2% or 8%.

Common Inflation-Hedging Mistakes to Avoid

Mistake #1: Going All-In on Gold

Gold gets hyped as the ultimate inflation hedge, but it's volatile and produces no income. A 5% allocation is plenty—more is speculation, not protection.

Mistake #2: Abandoning Stocks Entirely

Some retirees panic-sell stocks during inflationary periods. Big mistake. Quality companies with pricing power often emerge stronger. The key is choosing the right stocks.

Mistake #3: Chasing Last Year's Winners

Inflation hedges rotate in performance. Energy might lead one year, REITs the next. Maintain diversification rather than chasing hot sectors.

Mistake #4: Ignoring International Markets

U.S.-only portfolios miss opportunities. When the dollar weakens (common during inflation), international stocks provide natural hedging.

Mistake #5: Forgetting About Taxes

TIPS generate phantom income that's taxable. REITs often distribute non-qualified dividends. Use tax-advantaged accounts wisely.

🎯 Your Inflation-Proofing Action Plan

- Assess current portfolio: Calculate your inflation-hedge allocation. If it's under 25%, you're vulnerable to sustained inflation.

- Start with TIPS: Add 10-15% TIPS allocation immediately. Use I Bonds for amounts under $10,000 annually.

- Add real estate exposure: Target 8-12% in REITs through diversified index funds.

- Review your bond allocation: Shift to shorter duration or floating-rate bonds if rates are rising.

- Implement quarterly reviews: Track real returns vs. nominal returns. Rebalance if allocations drift 5%+ from targets.

- Consider professional help: Complex inflation hedging benefits from professional portfolio management, especially for accounts over $500,000.

Final Thoughts: Building Wealth That Lasts

Inflation protection isn't about predicting the future—it's about preparing for multiple scenarios. The portfolio allocation outlined here won't be perfect in every environment, but it's designed to preserve purchasing power across different inflationary cycles.

Remember: time is your enemy when fighting inflation. Every year you delay making these adjustments, inflation compounds against you. The 60-year-old who starts inflation-proofing today will be far better positioned than the one who waits until age 70 when inflation is already eating away at their fixed income.

Start building your inflation-resistant portfolio today. Your future self will thank you when that morning coffee still feels affordable at age 85.