Living Paycheck to Paycheck at $100K: Why High Earners Can't Save for Retirement (And How to Break the Cycle)

36% of Americans earning six figures live paycheck to paycheck with zero retirement savings. Here's why traditional retirement advice fails high earners — and the unconventional strategies that actually work to break the cycle.

High earners struggle to save because:

- Lifestyle inflation eats raises faster than you can save them

- Professional infrastructure is expensive (degrees, housing near jobs, reliable transport)

- Traditional advice assumes surplus income that doesn't exist

Solution: Start with micro-investments ($25/month), hijack half of all future raises for savings, and automate everything to remove decision fatigue.

The High Earner No Savings Problem Nobody Talks About

My friend Sarah earns $110K as a marketing manager down in Austin. Should be living the dream, right? Wrong. She's got maybe 200 bucks left at the end of each month, and her retirement savings account? Yeah, that's sitting at a big fat zero.

And here's the kicker – she's not some financial disaster case. She's actually pretty smart about money.

But 36% of people making six figures live paycheck to paycheck. More than one in three! That means if you're at a dinner party with high earners, at least one person at that table is secretly broke. And they're probably ordering the most expensive wine to hide it.

This isn't just hitting the folks making minimum wage anymore. It's crushing an entire generation of people who did everything "right" – got the degree, landed the corporate job, and are still going to work until they die.

Why High Income Earners Live Paycheck to Paycheck: The Math

Let me break down Sarah's situation because it's probably yours too.

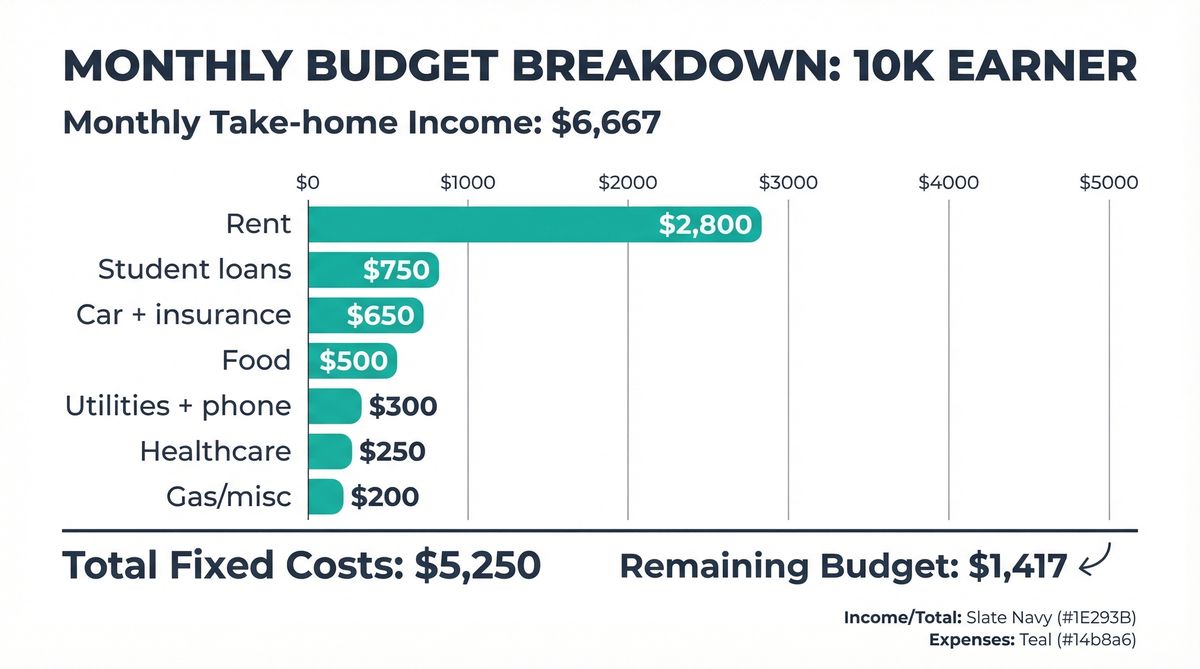

Her $110K becomes about 80 grand after Uncle Sam and health insurance take their cut. That's $6,667 a month, which sounds like decent bread until you see where it goes:

| Expense | Monthly Cost | Notes |

|---|---|---|

| Rent | $1,800 | One-bedroom in Austin |

| Student loans | $650 | MBA debt |

| Car + insurance | $550 | Can't Uber to client meetings |

| Food | $600 | Groceries + occasional dining |

| Utilities + phone | $200 | Basic necessities |

| Healthcare out-of-pocket | $150 | Even with "good" insurance |

| Gas and miscellaneous | $300 | Random life expenses |

| Total Fixed Costs | $4,250 | Remaining: $2,417 |

That's $4,250 in stuff she can't really avoid. She's got $2,417 left for clothes, entertainment, travel, and oh yeah – that thing called retirement.

Spoiler alert: it never gets saved.

The problem isn't that Sarah's blowing money on designer handbags. It's that being a "successful professional" in America got incredibly expensive while nobody was paying attention.

The Hidden Costs of Lifestyle Inflation for High Earners

Every financial advisor wants to talk about your Starbucks habit. But when you're making 75-150K, your problems aren't caused by overpriced coffee.

They're caused by all the expensive s*** you need just to keep your job:

Housing Costs Eat High Earner Salaries

You've gotta live where the jobs are. Sarah could move to some small town and pay $800 for a house. She could also say goodbye to marketing jobs that pay six figures. Those gigs are all in expensive cities where rent eats half your paycheck.

Professional Infrastructure Has a Price Tag

Looking professional costs money. You need a reliable car, decent clothes, and often some fancy degree. Sarah's MBA cost her 85K, but it also got her that 110K job. Catch-22, much?

Time Becomes Money for High Earners

Time becomes money. Make more, work more, buy convenience. DoorDash and cleaning services aren't luxuries when you're pulling 50-hour weeks – they're survival tactics.

Social Pressure Drives Spending

Your social circle gets pricier. When everyone around you is booking weekend getaways and talking about their stock portfolios, there's this quiet pressure to keep up. Nobody wants to be the broke friend.

Definition: Lifestyle Inflation

Lifestyle inflation (also called "hedonic adaptation") is the tendency for expenses to rise along with income. It happens so gradually you don't notice until your financial pants don't fit anymore. Some of it's required to maintain your income level. The rest is just expensive habits that sneak up on you.

Why Traditional Retirement Advice Fails High Earners

Traditional retirement advice assumes you've got extra cash floating around. "Pay yourself first!" "Max out your 401k!" "Build that emergency fund!"

Great tips. Completely useless if you're already spending every dollar you make.

The entire retirement industry is basically built for people who've already figured out how to have leftover money. It's like someone giving you a detailed workout plan when you can't afford a gym membership.

The Advice Gap

Most retirement guidance assumes you have a spending problem, not an income-allocation problem. High earners need strategies that work within existing financial constraints, not lectures about cutting lattes.

Millions of high earners are stuck in this weird spot – too "rich" for assistance programs, too broke to follow traditional wealth advice.

And here's the Federal Reserve reality check: 43% of workers have less than ten grand saved for retirement. These aren't all minimum-wage folks. A ton of them are middle-class earners who should theoretically have their s*** together.

How Time Works Against High Earners With No Savings

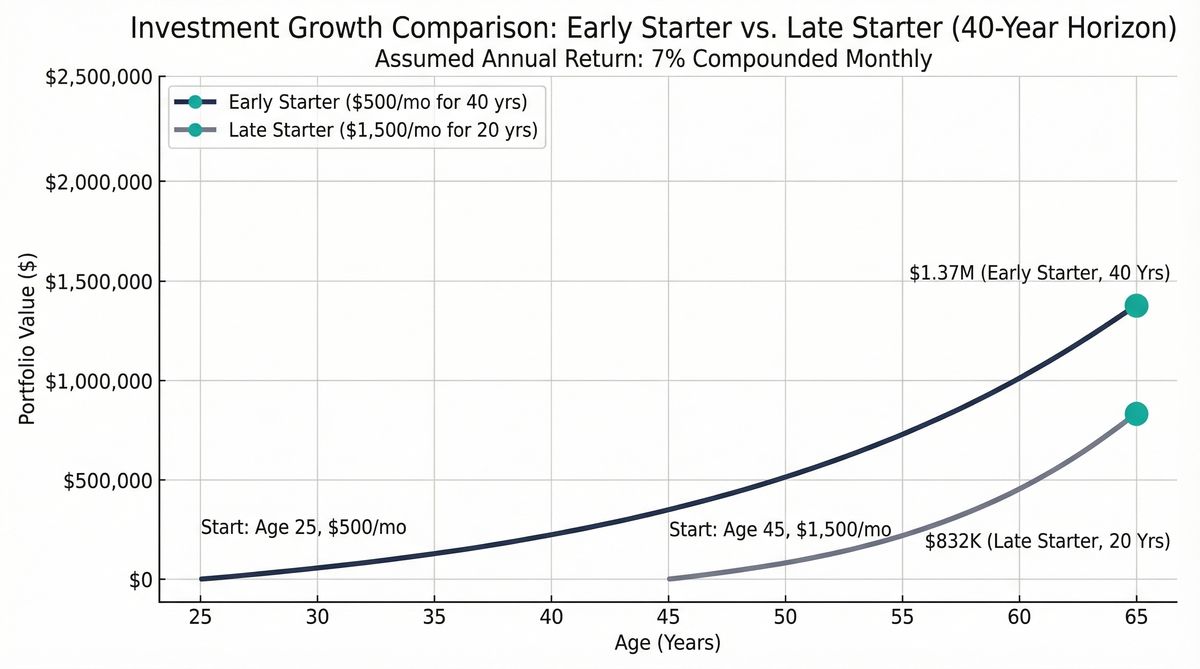

While high earners are struggling to save their first thousand bucks, compound interest is out here playing favorites.

Early Starter

- Starting Age 25

- Monthly Investment $500

- Years Investing 40

- Total at 65 $1.37M

Late Starter

- Starting Age 45

- Monthly Investment $1,500

- Years Investing 20

- Total at 65 $732K

Someone who starts investing $500 a month at 25 ends up with more retirement money than someone who starts investing $1,500 a month at 45. Same total contributions, but the early bird wins by hundreds of thousands.

Sarah's 34. Every year she waits costs her about $50K in final retirement wealth. Not exactly a problem you can solve later.

How to Break the Paycheck to Paycheck Cycle: Strategies for High Earners

Good news – high earners have some advantages once they stop trying to follow advice written for people with different problems.

Start Stupidly Small to Break the High Earner No Savings Pattern

Forget maxing out retirement accounts. Start with $25 a month. I'm serious.

You're not trying to get rich immediately. You're trying to prove to yourself that you can save money without your world ending.

Set up an automatic transfer the day after payday. Make it so small you won't miss it. After three months of successfully saving 25 bucks, bump it to 50.

Behavioral Psychology Hack

This isn't about the money – it's about rewiring your brain to believe saving is possible. Research shows that starting any positive financial behavior, no matter how small, dramatically increases the likelihood of expanding that behavior.

Hijack Your Raises to Prevent Lifestyle Inflation

This is the secret sauce for high earners: when you get a raise, immediately hijack half of it for savings.

Sarah gets a $10K raise? Her take-home jumps about $583 a month. Instead of inflating her entire lifestyle, she sends $300 to retirement and keeps $283 for fun stuff.

She still feels richer, but she doesn't blow all the new money on lifestyle upgrades. Rich people call this "lifestyle stabilization" – keeping your expenses steady while your income grows.

Solve Housing to Break the Paycheck to Paycheck Cycle

Sarah's biggest expense is rent at 27% of her income. Time to think outside the box:

House hacking: Buy a duplex, live in one side, rent out the other. Done right, her housing costs drop to maybe $800-1000 while building equity. That frees up $800+ monthly for retirement.

Geographic arbitrage: Work remote and move somewhere cheaper. Austin salary, Oklahoma City rent = automatic raise of 30-40%.

Both require some lifestyle adjustment, but they can free up enough cash to actually max out a 401k.

Build Strategic Side Income for High Earners

Key word: smart. Don't drive for Uber. Build on what you already know.

Sarah could consult for small businesses on marketing. Uses her existing skills and network. More importantly, she can charge more as she gets better at it.

This isn't about working 80 hours forever. It's about creating a temporary income boost to catch up on retirement, then scaling back to your day job.

Automate Everything to Prevent Decision Fatigue

Willpower is overrated. Don't rely on yourself to save whatever's "left over" each month.

Set up your direct deposit to automatically split between checking and retirement accounts. Make saving happen before you see the money.

When saving is automatic, you adapt your spending to what remains instead of trying to save from leftovers.

Real Talk About Breaking the High Income Paycheck to Paycheck Trap

No magic bullets here. If you're a high earner living paycheck to paycheck, fixing it requires some uncomfortable changes.

Maybe you downsize your place. Maybe you drive an older car for a while. Maybe you skip some social stuff while building financial stability.

These aren't forever sacrifices. But they're necessary ones.

Because the alternative is working until you're 75 with nothing saved.

The Employee Benefit Research Institute says workers who hit 65 with less than 50K have a 90% chance of going broke before they die. That's not a retirement plan – that's a horror movie.

Small Moves, Big Results for High Earner Retirement Planning

Here's what trips people up: you don't need to save a fortune to avoid being broke in retirement.

If Sarah starts saving just $300 a month at 34, she'll have about $330K at 65 (assuming 7% returns). Not rich, but not eating cat food either.

Bump that to $500 monthly by age 40, and she's looking at $450K. Still not yacht money, but enough to actually retire.

These numbers don't require dramatic lifestyle surgery – just consistent, automated saving starting now.

🎯 Your Action Plan to Break the Cycle

- This week: Set up a $25/month automatic transfer to a retirement account. Make it happen the day after payday.

- Next raise: Immediately redirect 50% of any income increase to savings before lifestyle inflation kicks in.

- This month: Audit your biggest expense (probably housing) and research one unconventional way to reduce it.

- Long-term: Build strategic side income that leverages your existing skills and network.

How to Break the Paycheck to Paycheck Cycle: The Bottom Line

High earners living paycheck to paycheck aren't failures. They're people who believed the lie that earning more automatically fixes money problems.

Plot twist: expenses expand to fill whatever income you have. It's like some weird law of physics, but for your bank account.

Breaking the cycle means admitting that traditional retirement advice doesn't apply to your situation, then building systems that work within your constraints.

Start small. Hijack your raises. Automate everything. And stop believing your next promotion will magically solve your retirement problem.

Sarah's story doesn't have to end with working until she dies. But it does require her to save for retirement now, with the money she has, at the spending level she's already committed to.

It's not impossible. Just different from what most financial advice assumes.

Ready to break your own cycle? The tools exist. Question is whether you'll use them before time runs out.

Peace!