The New Retirement Playbook: What the 2026 Data Says, and What to Do About It

For most of the last century, retirement had a shape everybody knew by heart. You worked until some fixed age, they handed you a gold watch and maybe a sheet cake, and you walked out the door on a Friday afternoon for good. Monday you were a retiree. That shape is coming apart at the seams.

- 72% of Americans now expect to retire exactly when and how they want, up five points in a year, but confidence splits sharply by generation and gender.

- A written plan changes everything: 83% of planners feel highly confident versus just 38% of people without one.

- The "bridge years" before Social Security and RMDs are your best window for Roth conversions and catch-up contributions, including a new $11,250 "super catch-up" for ages 60-63.

- Healthcare will cost more than you think: roughly $172,500 for a single retiree and $345,000 for a couple, before long-term care.

- 31.9 million old 401(k)s sit forgotten from past jobs, holding an estimated $2.1 trillion combined.

Action: Write your plan down, use the 2026 catch-up limits, and model your specific numbers before year-end.

Fidelity just put out its 2026 State of Retirement Planning Study, run by a research outfit called Big Village, and they talked to 2,015 American investors about all this. What they found is a clean break from the old model. Retirement isn't a single date on a calendar anymore. It's a transition now. It's gradual, it's negotiable, and more and more people are designing it on their own terms. Get this: 72% of Americans now expect to retire exactly when and how they want. That's up five points in a single year.

And that optimism is real. I believe it. But it's also fragile, it's spread around unevenly, and for the folks standing closest to the door, it's often floating way above the actual nuts and bolts of pulling it off. So let me walk you through what the numbers really say, and what your 2026 retirement planning should look like before this year runs out.

Retirement Became a Dimmer Switch, Not a Light Switch

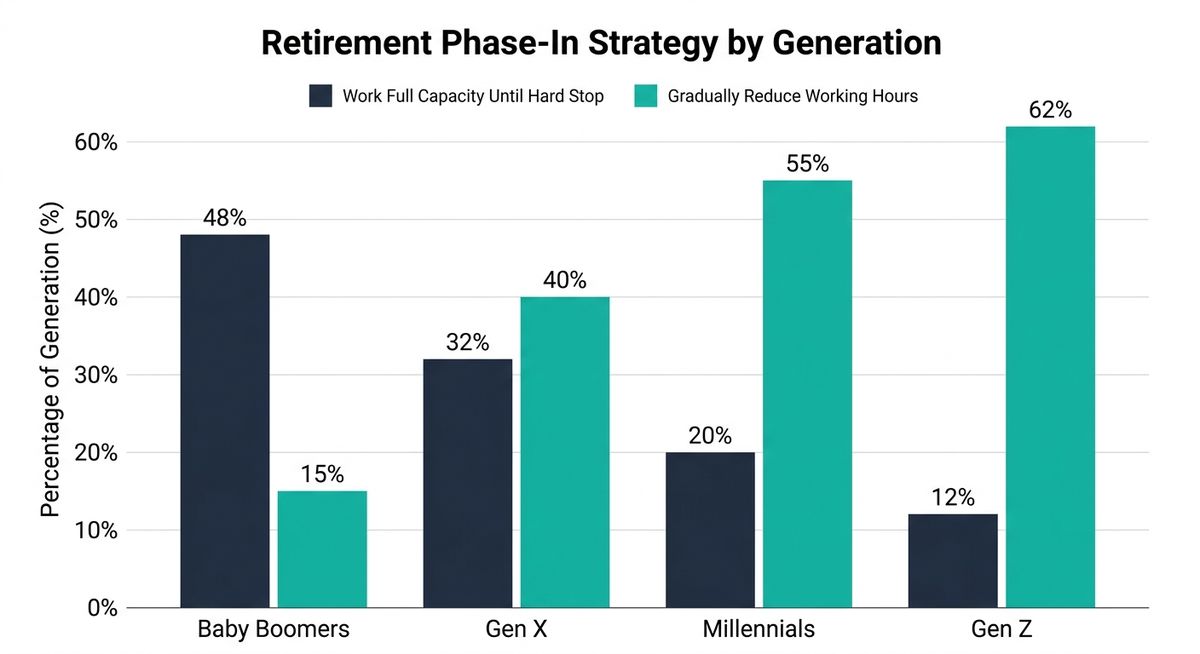

The loudest signal in this whole study is that people have stopped thinking of retirement as a hard stop. Roughly six in ten now plan a phased retirement: a gradual, multi-stage exit instead of a clean break. Only about a quarter still have no target age in mind, and a small slice, 6%, have decided they're just never going to retire at all.

Look at how folks actually plan to step back, and the dimmer-switch idea really comes into focus:

- 34% plan to slowly cut their working hours before they officially retire.

- 30% want to shed responsibilities at their current job to ease their way out.

- 18% plan to slide into freelance, contract, or consulting work.

- 32% still pick the old-school route, running at full speed right up until the day they stop.

Your generation shapes a lot of this. Baby Boomers are holding tight to the old script, with about half of them planning to go full-bore until a hard finish line. Younger folks want to downshift way earlier. And that gap matters if you're a pre-retiree, because the slow phase-out that a lot of Boomers now wish they'd set up is exactly the option a Gen Xer still has time to build.

So why is the timeline stretching out and going soft? Because the bills you have right now are fighting for the same dollars your retirement needs. The rising cost of living was the one drag that hit every single age group, named by about half of everybody and by 56% of Gen X, higher than any other generation. Paying off personal debt peaked with Gen X too, at 36%. This is the sandwich generation's whole life in a nutshell: a mortgage, some debt, aging parents, and grown kids who still need help, all tugging at the same account at the same time.

The Takeaway

Here's the takeaway if you're within ten years of retiring. A phased exit is the mainstream plan now, not some backup you settle for. If you want the option to drop to 30 hours at 60 while hanging onto your work health coverage until Medicare kicks in at 65, that doesn't just happen. You have to design it on purpose, and honestly, you want to talk it over with your employer before you need it, not the week you're trying to walk.

The Confidence Gap Nobody Really Wants to Talk About

Averages have a way of hiding the best story in the room. That shiny 72% number splinters the second you start breaking it apart.

Gen X, the folks now standing at the very front of the retirement line, are the least confident of the bunch. Only 63% believe they'll retire on their own terms, against 78% of Millennials and 75% of Gen Z. The people closest to the finish line feel the least sure they'll actually cross it. Kind of backwards, right?

The people closest to the finish line feel the least sure they'll actually cross it.

The gender gap is even wider. In the full 2026 study, 81% of men feel confident they'll retire when and how they want, next to just 63% of women. That's an 18-point canyon, and the press coverage of the study backs it up. The roots of it are structural, not personal. Women do roughly 2.5 times more unpaid caregiving, and a five-year break to take care of family can knock about 25% off your retirement savings. So if you're a woman who stepped back from work for your kids or your parents, you're not imagining that setback. It's real. And I've got some specific catch-up moves further down that are built for exactly this spot.

Now here's the single most useful thing in the entire study, so lean in for this one. Confidence isn't really about how much you make. It tracks almost perfectly with one thing: whether you actually wrote the plan down.

Among Americans with a written retirement plan, 83% feel highly confident. Without one? Just 38%. More than double. And the effect follows you right into retirement. Among people already retired, 81% of those who used a plan say they've got enough money to last comfortably for life. For the folks who didn't plan, that number drops to 45%. That's a 36-point gap in plain old financial security, separating the people who wrote it down from the people who just wung it.

The Plan Beats the Paycheck

83% of Americans with a written retirement plan feel highly confident, versus just 38% without one. That gap holds up in retirement too: 81% of retirees who planned say their money will last a lifetime, against 45% of those who didn't.

And people clearly believe in this stuff. 74% say they've got a plan to hit their goals, and 90% agree that planning has to keep going during retirement, not stop at the door. But believing and doing are two different animals. 31% of people who know their target retirement age have no idea how much money they'll actually have when they get there. Knowing the "when" without the "how much" is the blind spot this study drags out into the daylight. Closing that gap doesn't take a finance degree. You can run these numbers for your own situation at ReadyAimRetire.com and see where you'd actually land, which turns "I have a plan" into a plan with real figures behind it.

Ready to run your own numbers?

See how your retirement plan stacks up with ReadyAimRetire's free retirement calculator.

Try It Free →The Bridge Years: Your Highest-Leverage Window

The stretch between leaving your main job and switching on Social Security or facing your Required Minimum Distributions has a name that planners love: the bridge years. Your income is low for a little while, and that low income is exactly what makes this the best window you'll ever get for smart tax moves. And 2026 hands you some specific tools to work with.

Start with the higher ceilings. For 2026, the 401(k), 403(b), and 457 employee deferral limit climbs to $24,500, and the IRA limit goes to $7,500. If you're 50 or older, the standard 401(k) catch-up tacks on another $8,000, bringing your total to $32,500.

The most overlooked gift for late-stage savers is the SECURE 2.0 "super catch-up." If you're between 60 and 63, your 401(k) catch-up jumps to $11,250, which lets you shovel roughly $35,750 into your workplace plan in one year. This is a narrow four-year turbo window built precisely for the people in the final sprint, and most savers have no clue it even exists.

| 2026 Limit | Amount |

|---|---|

| 401(k) / 403(b) / 457 employee deferral | $24,500 |

| IRA contribution limit | $7,500 |

| Standard catch-up (age 50+) | +$8,000 ($32,500 total) |

| "Super catch-up" (ages 60-63) | +$11,250 ($35,750 total) |

Watch Your Step: The Roth Catch-Up Mandate

One change trips up high earners, so watch your step here. Starting January 1, 2026, the Roth catch-up mandate says anyone who made more than $150,000 from their employer the year before has to make catch-up contributions on a Roth (after-tax) basis instead of pre-tax. If you're a high earner who was counting on that pre-tax deduction, don't worry, the money still goes in. But the tax treatment flipped. Plan your cash flow around it.

Then there are the conversions. With the RMD age now sitting at 73 (for folks born 1951 through 1959, moving up to 75 in 2033), those low-income bridge years before RMDs kick in are prime territory for Roth conversions. That just means moving money out of your tax-deferred accounts and paying the tax now, while your bracket is low, so you dodge bigger forced withdrawals later. And savers are already on it: 38% now prioritize tax-advantaged accounts, 34% set up their savings to grab the full employer match, and 15% have already done proactive Roth conversions.

Picture my friend Diane, a Gen Xer at 58. She drops to 30 hours at 60 to keep her health insurance, uses that 60-to-63 super catch-up to load up her last real working years, then runs small Roth conversions in the quiet low-income stretch before 73. She's not doing anything fancy or exotic. She's just stacking the 2026 tools in the right order. That's it. But her stacking order won't fit every account mix or tax bracket. Every retirement plan is different, and ReadyAimRetire lets you test how these bridge-year strategies work with your specific numbers before you commit to them.

The Healthcare Number That Should Reshape Your Whole Plan

Eight in ten Americans (80%) expect healthcare to cost a small fortune in retirement. They're right to sweat it, and most of them are still lowballing the number.

Fidelity's separate 2025 estimate figures a single 65-year-old retiring today will need roughly $172,500 (after tax) to cover healthcare across retirement, and about $345,000 for a couple. Now, that's a modeled projection, not a survey answer, and it leaves out long-term care completely, which means your real exposure runs even higher. Roughly 70% of people over 65 will need some kind of long-term care, and a private nursing-home room now runs a median of about $11,294 a month. Let that one sink in.

Single Retiree, Age 65

- Lifetime Healthcare Cost ~$172,500

- After-Tax Dollars Yes

- Long-Term Care Not Included

Retired Couple, Both 65

- Lifetime Healthcare Cost ~$345,000

- After-Tax Dollars Yes

- Long-Term Care Not Included

Savers are putting up a fight, though. The study found 40% are bumping up their baseline retirement contributions, 27% plan to buy Medigap coverage, and 22% are putting money into long-term care insurance so one medical event doesn't force them to sell off the whole portfolio. A growing group likes the hybrid life-and-long-term-care policies that take away the old "use it or lose it" gamble.

The sharpest single move here is the Health Savings Account, and 25% of savers are already feeding one. An HSA is the only triple-tax-advantaged account in the whole tax code. It's deductible going in, it grows tax-free, and it comes out tax-free for qualified medical costs. For 2026 the family limit rises to $8,750, plus a $1,000 catch-up once you hit 55. The "stealth IRA" play is dead simple: max the account, pay your current medical bills out of pocket, save every single receipt, and let that balance compound for decades. A couple in their late 50s who runs this can build a dedicated, tax-free stash aimed right at that $345,000 number.

The HSA "Stealth IRA" Play

Max out your HSA, pay medical bills out of pocket, and save every receipt. Left alone to compound for decades, that balance becomes a dedicated, triple-tax-free stash aimed right at your future healthcare number.

One warning for the bridge years, and this is where people stub their toe. Medicare's income-related surcharges, called IRMAA, kick in at a modified adjusted gross income of $109,000 for singles and $218,000 for couples, with the standard Part B premium already climbing to $202.90 a month in 2026.

The IRMAA Look-Back Trap

Here's the catch: IRMAA looks back two years at your income. So a big, badly-timed Roth conversion can shove you over a surcharge cliff and spike your premiums two years down the road. That's exactly why conversions belong in the low-income window, and why knowing your accounts pays off. 66% of respondents understand that IRAs and 401(k)s play different roles, and that kind of know-how is what keeps savers on the right side of these cliffs.

Ready to run your own numbers?

See how your retirement plan stacks up with ReadyAimRetire's free retirement calculator.

Try It Free →Stop Leaving Money Scattered Across Old Jobs

The modern career basically guarantees a mess. The average American now works for 6 different employers over a lifetime, and every time you leave, you tend to leave a 401(k) sitting behind. The study found that 23%, nearly one in four savers, are currently holding money spread across a bunch of accounts from past jobs.

And the scale of this at the national level is honestly hard to believe. As of 2026, there are an estimated 31.9 million forgotten 401(k) accounts holding roughly $2.1 trillion, which pencils out to about $66,000 each. Leave a balance sitting there un-consolidated over the decades, and it can quietly cost a saver six figures in lost compounding and doubled-up fees. That's real money you already earned, just gathering dust.

$2.1 Trillion, Forgotten

31.9 million old 401(k) accounts are sitting un-consolidated nationwide, averaging about $66,000 each. Left alone over the decades, that kind of balance can quietly cost a saver six figures in lost compounding and doubled-up fees.

Folks are cleaning house, though: 32% have rolled old balances into their current workplace plan, and 21% have pulled everything into a personal IRA. Both are fine, and the choice comes with real trade-offs. An IRA usually gives you a lot more investment choice. Keeping the 401(k) hangs onto creditor protection, loan access, and, for high earners, backdoor Roth eligibility by sidestepping the pro-rata rule. And here's a genuinely new tool: SECURE 2.0 launched the DOL Retirement Savings Lost and Found database at lostandfound.dol.gov, so that account you lost track of from some job in your twenties might actually be searchable now.

Picture my man David with four old 401(k)s floating around. He rolls three into an IRA so he's in control, keeps one in his current plan to protect his backdoor-Roth eligibility, then searches the Lost and Found and turns up a fifth account he'd completely forgotten he had. Consolidation isn't just tidying up your junk drawer. It streamlines your asset allocation, it makes tax coordination way simpler, and it makes managing RMDs a whole lot easier once your hours start bouncing around.

The Playbook, Boiled Down to This Year's Retirement Planning Checklist

The income data tells the same story as everything else: spread it out. Retirement income now leans on three roughly equal legs, workplace plans (45%), Social Security (44%), and personal savings (41%), with brokerage accounts, pensions, and IRAs backing them up. The generational split is worth a look. Boomers still lean hard on the safety net, with 76% naming Social Security a top-three source, while younger workers anchor on employer plans. No single leg carries the whole weight anymore, and that's exactly why your strategy matters more than any one account.

Confidence follows planning. Planning follows action. So let's turn this whole paradigm shift into some concrete moves before December rolls around. Start by modeling your retirement at ReadyAimRetire so the plan you write down is backed by actual projections instead of guesswork:

🎯 Your 2026 Retirement Planning Checklist

- Write the plan down. This is the 83%-versus-38% move, the highest-return thing in the entire study. A plan on paper beats a plan in your head every time.

- Design your phased retirement on purpose. If you want reduced hours while keeping your work health coverage to 65, bring it up with your employer now, not the week you're heading for the exit.

- Use the 2026 catch-ups. Load that $8,000 catch-up at 50-plus, and the $11,250 super catch-up if you're 60 to 63. If you make over $150,000, plan around the Roth catch-up mandate.

- Run Roth conversions in the bridge years, sized to stay under the $109,000 single / $218,000 joint IRMAA thresholds.

- Treat your HSA like a stealth IRA, and stress-test your plan against that $172,500-per-person healthcare number, long-term care included.

- Consolidate your old accounts, and go search the DOL Lost and Found for anything you left behind.

Four in ten Americans still worry they can't afford to retire, and I'm not going to pretend that fear isn't real. It is. But the deeper message in this study is that calling your own shots isn't reserved for the wealthy anymore. It belongs to the planners. Retirement planning stopped being about hitting a certain age. It became a strategy you build, and 2026 is the year to build yours.

Thanks for reading if you've made it this far. Now go write your plan down. Peace!

Sources: 2026 State of Retirement Planning Study (Big Village for Fidelity Investments, 2,015 U.S. adults ages 18 to 79, fielded December 2 to 8, 2025); Fidelity 2025 Retiree Health Care Cost Estimate; IRS Notice 2025-67 (2026 retirement-plan limits); IRS Rev. Proc. 2025-19 (2026 HSA limits); 2026 Medicare Part B and IRMAA figures (CMS); Capitalize 2026 forgotten-account analysis. Contribution limits, healthcare, and long-term-care figures are current estimates and projections, not survey findings.