The Inherited IRA Time Bomb: What the 10-Year Rule Actually Costs You (and How to Cut the Bill in Half)

If you inherited an IRA after 2019 and haven't been making withdrawals, you could owe a 25% excise tax plus a six-figure income tax bill when the clock runs out. Here's how to avoid both.

If you inherited an IRA after 2019, the old "stretch" rules are gone. You have 10 years to empty the account, but how you withdraw matters enormously:

- Wrong approach: Wait until year 10, face 35-37% tax brackets, owe $270,000+ in taxes on a $500K account

- Smart approach: Use bracket-filling strategy, stay in 22% bracket, pay $165,000 in taxes on the same account

- Critical deadline: IRS penalty waivers ended in 2024 - annual RMDs now required if original owner had started theirs

Action: Calculate your RBD status and create a year-by-year withdrawal schedule before December 31, 2026.

Your parent saved diligently for decades. They maxed out contributions, weathered market downturns, and built a retirement account worth hundreds of thousands of dollars. Then they passed it on to you.

What they couldn't pass on was a warning: the IRS changed the rules, gave you a few years of silence, and is now ready to collect. If you inherited an IRA after 2019 and haven't been making withdrawals, you could owe a 25% excise tax on what you should have taken out, plus a six-figure income tax bill when the clock runs out.

Here's how to avoid both.

The Rule That Changed Everything

Before 2020, inheriting an IRA was straightforward. You could "stretch" distributions over your entire life expectancy, taking small annual withdrawals that kept taxes low for decades. A 50-year-old who inherited a $500,000 IRA might withdraw $15,000 a year, letting the rest grow tax-deferred for another 30+ years.

The SECURE Act killed the stretch IRA for most beneficiaries. Starting with deaths after December 31, 2019, non-spouse beneficiaries must empty the inherited account within 10 years. No exceptions (unless you qualify for a narrow list of exemptions we'll cover later).

The Scale of This Change

Nearly $20 trillion sits in tax-deferred retirement accounts held by Baby Boomers and the Silent Generation. Boomer deaths are expected to climb from 2.6 million per year now to 4 million per year by 2037. Every one of those deaths can trigger a new 10-year countdown for the beneficiary.

That 10-year inherited IRA rule affects millions of Americans. If you inherited in 2020, your deadline is December 31, 2030. If you inherited in 2022, it's December 31, 2032. The math is simple. What isn't simple is how to withdraw the money.

The Fork in the Road Most People Don't Know About

Here's where the inherited IRA rules get complicated, and where most people (and most online guides) get it wrong.

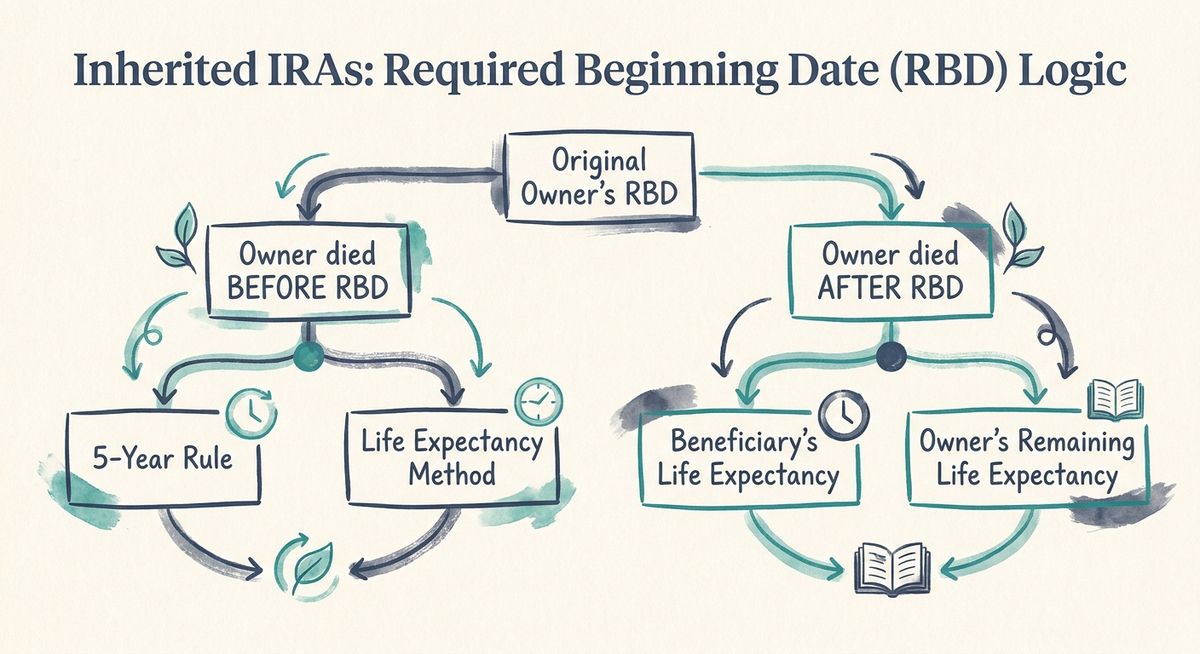

The IRS doesn't treat all inherited IRAs the same. Everything depends on a single question: Had the original owner already started taking Required Minimum Distributions when they died?

Definition: Required Beginning Date (RBD)

Required Beginning Date is April 1 of the year after the owner turns the RMD age (73 for those born 1951-1959, 75 for those born 1960 or later, and earlier ages for older generations).

Owner Died BEFORE RBD

- Annual RMDs Required NO

- Withdrawal Flexibility Maximum

- Strategy Options Any timing

- Only Requirement Empty by year 10

Owner Died ON/AFTER RBD

- Annual RMDs Required YES (years 1-9)

- Withdrawal Flexibility Limited

- Strategy Options RMD + planning

- Requirements Annual + year 10 empty

This distinction is the single most important factor in your inherited IRA tax strategy, and it's the one most beneficiaries have never heard of.

The Four-Year Grace Period Is Over

The IRS spent years figuring out the details of these inherited IRA RMD requirements. Final regulations didn't land until July 2024. During that fog, the IRS waived the 25% excise tax on missed annual RMDs for tax years 2021 through 2024.

That grace period created a dangerous false sense of security.

Take Tom. He inherited his mother's $400,000 traditional IRA in 2021. She was 78, well past her RBD. Tom heard about the 10-year rule but took nothing in 2021, 2022, 2023, or 2024. Why would he? The IRS kept waiving the penalty.

Starting in 2025, that waiver is gone. Tom now owes an annual RMD based on his life expectancy factor, and he needs to take it every year through year 9. By 2031 (his year 10), whatever remains must come out in full. If his account has grown to $500,000 while he took nothing, he's looking at enormous distributions crammed into the final years and a tax bill that could exceed six figures.

Penalty for Missing RMDs

25% excise tax on the amount you should have withdrawn but didn't. You can reduce that to 10% if you correct the mistake within two years (by taking the missed distribution and filing Form 5329). Some beneficiaries have gotten the penalty waived entirely by providing a "reasonable explanation" to the IRS.

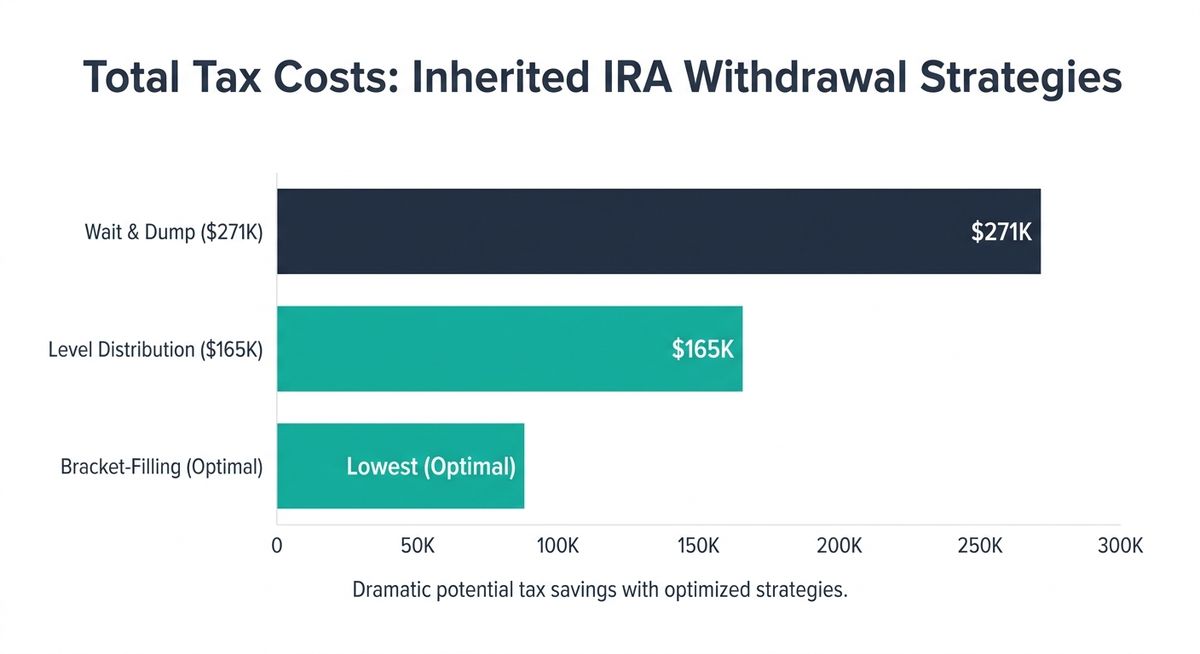

The $106,000 Question: Strategy Matters More Than You Think

The difference between the best and worst inherited IRA withdrawal strategy on a $500,000 account isn't a rounding error. It can exceed $100,000 in total taxes. Here are four approaches, ranked from worst to best.

The Worst: Wait and Dump (Year-10 Lump Sum)

This is what happens when people procrastinate or don't understand the rules. You take nothing (or the bare minimum) for nine years, then withdraw everything in year 10.

On a $500,000 inherited IRA growing at 3.5% annually, the balance reaches roughly $670,000 by year 10. Add that to your regular income, and you're looking at a massive spike. A household earning $130,000 suddenly reports $800,000 in taxable income, landing squarely in the 35-37% federal bracket.

Consider Sarah, a New Jersey resident with $210,000 in household income and a $500,000 inherited IRA. If she back-loads her withdrawals, her total tax bill (federal plus NJ state) hits $271,000.

Better: Level Distribution (Equal Annual Amounts)

Divide the balance by 10 and take equal amounts each year. For a $500,000 IRA, that's roughly $50,000 per year. Predictable and simple, this keeps you in a consistent tax bracket.

Sarah's tax bill with this approach: approximately $165,000. That's $106,000 in savings compared to the lump-sum approach. Same money, same IRA, same decade. The only difference is timing.

Best for Most: Bracket-Filling

This is the 10-year rule inherited IRA strategy that financial planners recommend most. It works like this:

- Project your income for each of the next 10 years.

- Identify the top of your target tax bracket (usually the 22% or 24% bracket).

- Each year, withdraw exactly enough from the inherited IRA to fill the gap between your other income and that bracket ceiling.

Lisa inherited her father's $500,000 IRA in 2022. He was 68 (before his RBD), so she has no annual RMD requirement, just the 10-year deadline. Lisa earns $120,000 per year filing jointly. With the $32,200 standard deduction, her taxable income is about $88,000, leaving roughly $123,000 of room in the 22% bracket (which tops out at $211,400 for married filing jointly in 2026). She can withdraw about $100,000 annually without leaving the 22% bracket.

If she'd waited until year 10, the $600,000+ balance would have pushed her deep into the 35% bracket, costing an extra $50,000 or more in federal tax alone.

2026 Tax Bracket Key Numbers

For married filing jointly: 22% bracket ceiling is $211,400, 24% bracket ceiling is $403,550. Standard deduction is $32,200. These exact figures let you calculate your own bracket-filling room.

Situational: Front-Loading

If you're between jobs, taking a sabbatical, or retiring mid-window, front-load your distributions into low-income years. A year where you earn $30,000 instead of $130,000 creates room for $100,000 or more in inherited IRA withdrawals at the 22% rate.

One caution: front-loading pulls money out of a tax-deferred account sooner, which means fewer years of tax-free growth. The tax savings typically outweigh the lost growth, but it's worth modeling both scenarios.

The Collateral Damage Nobody Warns You About

A large inherited IRA distribution doesn't just push you into a higher tax bracket. It triggers a cascade of secondary hits that can add thousands to your annual costs.

Medicare IRMAA Surcharges

Medicare premiums are income-tested, based on your tax return from two years prior. A large distribution in 2029 raises your premiums in 2031. A single IRMAA tier jump costs Medicare couples $2,296 or more per year in surcharges on Parts B and D combined. Jump two or three tiers, and you're paying hundreds extra per month for the same coverage.

Dave, age 63, inherited his father's $600,000 IRA in 2020. He coasted for years on minimal distributions, then pulled $400,000 in 2029 and the remainder in 2030. His 2029 income triggered the highest IRMAA tier, adding hundreds per month to his Medicare premiums starting in 2031.

Net Investment Income Tax (NIIT)

IRA distributions raise your Modified Adjusted Gross Income (MAGI), which can cause existing investment income to become subject to the 3.8% Net Investment Income Tax. The NIIT threshold is $250,000 for married couples filing jointly and $200,000 for singles. A year-10 lump sum distribution significantly increases the likelihood you'll hit these thresholds.

Lost Deductions and Credits

Many tax benefits phase out at higher income levels. A spike in AGI can reduce or eliminate deductions you normally count on.

State Tax Amplifiers

If you live in California (13.3% top rate), New Jersey (10.75%), or New York, state taxes dramatically compound the federal damage. Sarah's NJ taxes alone accounted for tens of thousands of her $271,000 worst-case bill.

Who Gets a Pass: The Exempt Beneficiaries

Not everyone is stuck with the 10-year window. Eligible Designated Beneficiaries (EDBs) can still stretch distributions over their life expectancy:

- Surviving spouses (who can also roll the IRA into their own account)

- Minor children of the account owner (but only until age 21, when the 10-year clock starts)

- Disabled individuals (meeting the IRC definition)

- Chronically ill individuals

- Beneficiaries who are not more than 10 years younger than the deceased owner

If you fall into one of these categories, the old stretch rules still apply. If you inherited before January 1, 2020, the old rules also still apply regardless of your relationship to the deceased.

Inherited Roth IRAs: A Different Playbook

If you inherited a Roth IRA, the 10-year rule still applies, but the calculus flips. Roth distributions are tax-free. There are no annual RMD requirements (the owner never had RMDs, so you're always in the "before RBD" category). The optimal inherited Roth IRA strategy is the opposite of a traditional IRA: let every dollar grow tax-free for as long as possible and withdraw it all in year 10.

Important Roth IRA Limitation

Non-spouse beneficiaries cannot convert an inherited traditional IRA to a Roth. That door is closed. Spouses who roll over to their own IRA can convert, but that's a different situation entirely.

🎯 Your Inherited IRA Action Plan

- Step 1: Answer the RBD question. How old was the original owner when they died? Had they started taking RMDs? This determines whether you must take annual distributions or have full flexibility.

- Step 2: Calculate your deadline. Count 10 years from the year after the owner's death. That's your final withdrawal date.

- Step 3: Check your 2026 obligation. If the owner died after their RBD, you owe an annual RMD this year. The IRS is no longer waiving penalties. Calculate your distribution amount using the IRS Single Life Expectancy Table.

- Step 4: Project your income for all remaining years. Include salary, Social Security, pensions, investment income, and any other sources. Identify the bracket ceiling you want to target (22% and 24% are the most common sweet spots).

- Step 5: Build a year-by-year withdrawal schedule. Fill the gap between your projected income and your target bracket ceiling each year. Adjust annually as circumstances change.

- Step 6: Watch for collateral triggers. Model the IRMAA impact for any year you'll be on Medicare. Check NIIT exposure. Factor in state taxes.

- Step 7: Execute and monitor. If you have room, consider the timing of larger withdrawals. Review your strategy annually as tax laws and personal circumstances change.

The difference between a thoughtful bracket-filling strategy and a panicked year-10 liquidation is real money: $50,000, $100,000, or more on a mid-sized inherited IRA.

The Bottom Line

The inherited IRA 10-year rule isn't just a deadline. It's a tax planning problem that rewards the prepared and punishes the passive. The difference between a thoughtful bracket-filling strategy and a panicked year-10 liquidation is real money: $50,000, $100,000, or more on a mid-sized inherited IRA.

The IRS gave everyone a four-year head start by waiving penalties from 2021 through 2024. That runway is gone. If you haven't started planning your distributions, 2026 is the year to begin. Every year you delay compresses the remaining withdrawals into fewer years, higher brackets, and bigger collateral hits.

Run the numbers. Build the schedule. And if the math gets complicated (it will), find a tax-focused financial planner who understands inherited IRA distribution strategies, not just a generalist who'll tell you to "take it out over 10 years" without modeling the brackets.

Your parent spent a lifetime building that IRA. Spend a few hours making sure the IRS doesn't take more than its share.

This article is for informational purposes only and does not constitute tax or financial advice. Consult a qualified tax professional or financial advisor for guidance specific to your situation.