The Easy Three-Fund Retirement Portfolio: A Beginner's Guide

Here's something the financial industry would rather you didn't dwell on: making investing look complicated is good for business. A portfolio stuffed with 15 or 20 or 50 funds looks impressive. It sounds like somebody smart is in charge. And complicated stuff is a lot easier to charge you money for than a three-fund portfolio ever will be.

- Three low-cost index funds — U.S. stocks, international stocks, and total-market bonds — capture nearly all the diversification that exists in the global market.

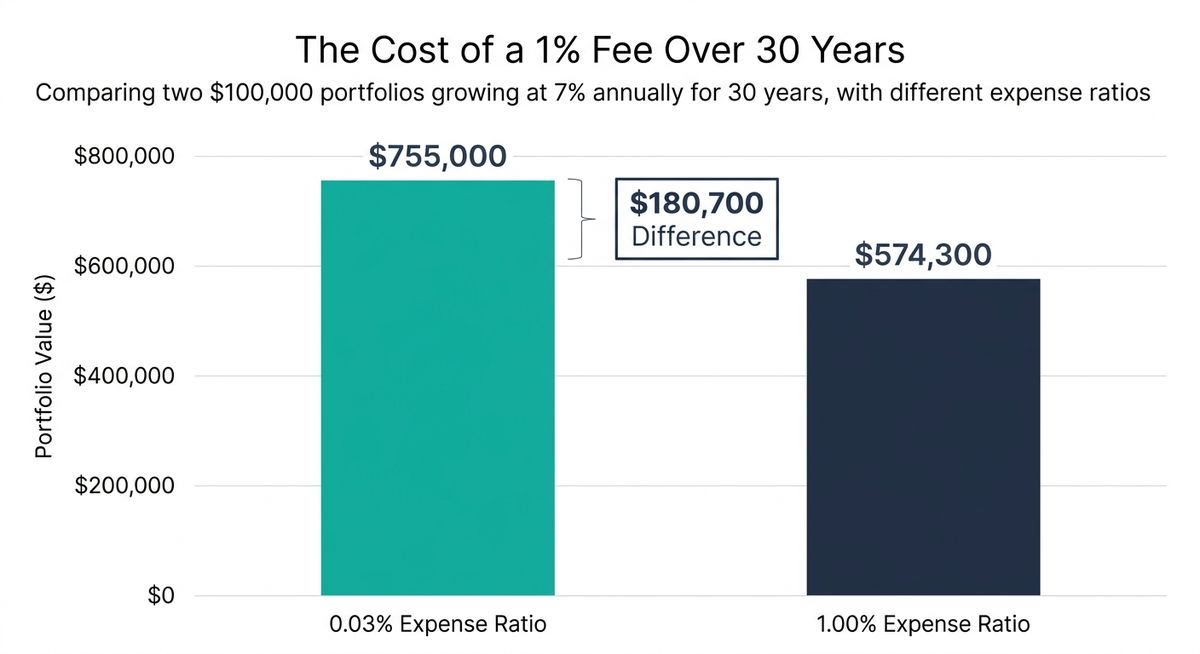

- Fees compound against you: a 1.00% expense ratio versus a 0.03% one can cost roughly $180,700 on a $100,000 portfolio over 30 years.

- Your stock/bond split matters more than which funds you pick, and it should shift more conservative as you approach the "retirement red zone."

- Smart asset location — which account holds which fund — can add 0.25% to 0.75% a year in after-tax return for free.

- Automatic monthly investing and once-a-year rebalancing do almost all of the real work. No market timing required.

Bottom line: three funds, tax-smart placement, and one rebalance a year get you most of the way there. The rest is just staying out of your own way.

Three funds. That's the whole trick.

But if you're within ten years of retirement, or you're already kicking back on the porch, complicated is working against you. It doesn't buy you more diversification. It usually buys you higher fees, a bunch of funds that all own the same companies, and a portfolio you're more likely to panic-sell the next time the market takes a dive.

So let me tell you the thing nobody selling you a product will say out loud: you can own the entire global stock and bond market with three funds. Three. Whether you're protecting five thousand dollars or five million, the same three pieces do the job. U.S. stocks, international stocks, and total-market bonds. Buy them as cheap index funds and you scoop up nearly all the diversification that exists on planet Earth while dodging the fees that quietly eat away at your money over 20 and 30 years.

I'll walk you through the three-fund setup. Then I'll do the thing most beginner guides skip right past: I'll show you how to adjust it if you're near retirement or already in it, because that's when the rules genuinely change on you.

The Three Pillars

The whole idea is to split your money across three broad buckets that don't step on each other's toes. Each one has a job. Together they cover just about the entire investable world.

U.S. Stocks

One total-market index fund holds the whole publicly traded American stock market — not just the Apples and Microsofts, but everything down to the little guys. Vanguard's Total Stock Market ETF (VTI) holds around 3,280 companies for a 0.03% expense ratio — about $3 a year per $10,000 invested.

International Stocks

The typical U.S. investor keeps 70–80% of their stock money at home, even though the U.S. is only 42–60% of the world's market value. One total international fund like Vanguard's VXUS holds more than 8,500 companies across developed and emerging markets for 0.05%.

Total-Market Bonds

Instead of juggling government, corporate, high-yield, and international bonds separately, one total bond index fund bundles it all together. Vanguard's BND holds roughly 17,700 government and investment-grade corporate bonds at 0.03%. It's the ballast that keeps the boat steady.

Vanguard's own research says a 30 to 40 percent international slice grabs more than 95 percent of the diversification benefit that's out there. That's exactly why their own Target Retirement funds go 40 percent international. If the folks running the funds do it, that tells you something.

Add it up and with these three funds you own more than 11,000 stocks and over 17,000 bonds all over the world. That's the real deal — the same institution-grade diversification the big money uses. And you can set the whole thing up in an afternoon, coffee in hand.

You're not married to Vanguard, either. Pick one fund family and stick with it, so you're not accidentally owning the same companies twice without realizing it.

| Asset Class | Vanguard | Fidelity | Schwab |

|---|---|---|---|

| U.S. Stocks | VTI — 0.03% | FZROX — 0.00% | SCHB — ~0.03% |

| International Stocks | VXUS — 0.05% | FZILX — 0.00% | SCHF — ~0.03% |

| Total-Market Bonds | BND — 0.03% | FXNAX — 0.025% | SCHZ — ~0.03% |

The Fee Nobody Ever Mails You a Bill For

Expense ratios look too tiny to care about. They're not. They're actually the single most reliable predictor of how a fund performs over the long haul, and they compound against you in the exact same relentless way that returns compound for you.

The Real Cost of a 1% Fee

Picture two identical $100,000 portfolios, both growing at 7% a year for 30 years. One pays a 0.03% expense ratio and grows to about $755,000. The other pays 1.00% — pretty normal once you add an actively managed fund or an advisor — and grows to about $574,300. Same market, same returns, same everything except cost. The difference: roughly $180,700, handed over in fees for a product that, on average, actually does worse than the cheap index fund.

John Bogle, the Vanguard founder who invented the first index fund, put it about as plainly as anyone ever has.

"The miracle of compounding returns is overwhelmed by the tyranny of compounding costs."

Cutting your fees is about the closest thing to a guaranteed raise your portfolio is ever going to get. Take the raise.

What History Actually Shows (and One Number You Should Not Trust)

The long-run numbers make the case for simple, balanced, boring investing better than any slick sales pitch ever could. Let's take a standard starting point: 50 percent U.S. stocks, 30 percent international, and 20 percent bonds.

Say you'd dropped a one-time $10,000 into that mix back in 1987 and then completely forgot about it through 2021. It would have compounded at about 8.64 percent a year and grown to over $168,000. Not bad for doing absolutely nothing. That 8.64 percent is the market's true annual return — what the analyst types call a time-weighted return.

Now let's make it look like how people actually invest. Same $10,000 to start, but now you also add $500 every month and rebalance once a year. The ending balance jumps to over $1.6 million. And here's where you'll sometimes hear somebody call that a "16 percent return," and this is exactly where I need you to slow down and pay attention, because that framing will fool you.

Time-Weighted vs. Money-Weighted Returns

The market didn't magically start earning 16 percent. The underlying return was still about 8.64 percent in both cases. That 16 percent number is a money-weighted return, or internal rate of return, and it mashes together actual investment performance with how much you put in and when. Over those 34 years, you personally added more than $200,000 of your own money — the extra wealth came from your savings habit plus compounding, not a hotter market. Calling both numbers "CAGR" just muddies the water.

Why should you care? Because one day you'll open your brokerage app, see a "personal rate of return" that beats the market, and instead of getting confused or, worse, chasing some strategy that promises to reproduce that number, you'll know exactly what you're looking at. It's mostly your own contributions showing up wearing a disguise — the same blended-math trick behind a lot of retirement calculators that get this wrong, so it pays to double-check what any tool is actually telling you.

The honest lesson still stands: steady, automatic investing is the engine. When you put in a fixed dollar amount every month, you buy more shares when prices are low and fewer when they're high, and you never have to guess where the market's headed next. If you're still working and funding a 401(k), guess what — you're already doing this with every single paycheck. Go you.

The Lump-Sum Wrinkle

Research going all the way back to 1926 shows that investing a lump sum all at once actually beats spreading it out about 73 percent of the time, simply because markets go up more often than they go down. Dollar-cost averaging isn't magic math that outsmarts the market — it's just the discipline of investing consistently, and it takes away the temptation to time your entries. That's worth a whole lot for your peace of mind.

Building Your Mix: The Asset Allocation Decision That Matters Most

Your single biggest choice is not which funds you buy. It's your asset allocation — the split between stocks and bonds. That ratio drives both your long-term return and, just as important once you're retired, how far your portfolio can drop in a rough year.

Here's how three common mixes have behaved over the years:

90/10 — Aggressive

- Standard Deviation ~13.6%

- Max Historical Drawdown ~49%

The highest expected returns, and the wildest ride. Almost half your money, gone on paper in the worst years.

80/20 — Balanced

- Standard Deviation ~12%

- 2008–09 Drawdown ~41%

- Time to Recover ~39 months

The classic sweet spot for people still building. A 30-year VTI/BND blend returned near 9.3% annualized.

70/30 — Moderate

- Standard Deviation ~10.6%

A noticeably calmer ride. You give up only a small slice of long-run return to get it.

Every retirement is different, and the right mix for you depends on your timeline, your other income sources, and how much volatility you can actually stomach when it shows up on your statement. ReadyAimRetire lets you test how these allocations play out using your own numbers instead of relying on someone else's averages.

If you're 30, an 80/20 or even 90/10 stance makes all the sense in the world, because time heals every one of those drops. But if you're five years out from retirement, those same numbers describe a real threat to your plans. And that's usually the exact spot where the beginner guides go quiet on you.

The Retiree's Real Danger: Sequence of Returns

When you're still building your nest egg, a crash is almost a gift. Your monthly contributions buy shares on sale. But when you're pulling money out to live on, that same crash can do lasting damage, because you're selling shares to fund your life at exactly the wrong moment.

Sequence-of-Returns Risk

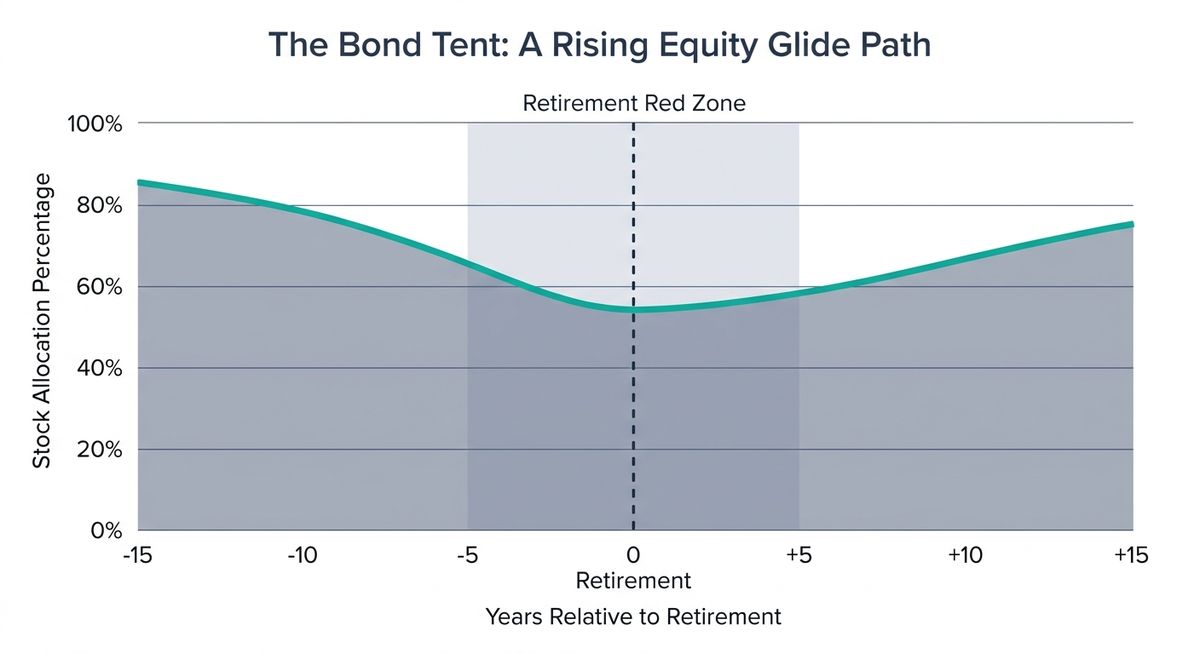

This has a name. It's called sequence-of-returns risk, and it's concentrated in the five to ten years right around your retirement date — a stretch planners nicknamed the "retirement red zone."

Two people can earn the identical average return over 30 years and land in completely different places, purely based on whether the bad years showed up early or late. Picture my friend Mark, who retired in 2007 holding nothing but stocks, then watched his portfolio fall more than 40 percent while he was drawing a paycheck out of it. Selling into a slide like that can lock in losses you just never get back. Mark's fine now, by the way, but those first couple years took years off his life.

This is why the bond pillar earns its keep. It's not there to juice your returns. It's there so that when stocks drop 40 percent, you can spend from your bonds and cash instead of selling stocks at the bottom. Two practical tools come out of this idea:

The bond tent

In the years right around retirement, you temporarily bump up your bond allocation, then slowly let stocks drift back up once you're safely through the red zone. You raise the tent when you're most exposed, and you lower it once the danger's behind you. Simple as that.

The rising equity glide path

Research from Wade Pfau and Michael Kitces found something counterintuitive: starting retirement more conservative, say 60/40 or 70/30, and then slowly increasing your stock allocation over time can actually improve the odds your money lasts. It sounds backwards, I know. But it takes direct aim at sequence risk, and the math holds up.

The takeaway: as you get close to retirement, plan to shift from an aggressive 90/10 or 80/20 building stance toward something more like 60/40 or 70/30. You're trading a little long-term growth for a lot of protection at the one moment in your life you can least afford a nasty surprise.

Ready to Run Your Own Numbers?

Every retirement is different. See how your own timeline, savings rate, and risk tolerance stack up using ReadyAimRetire's retirement planning tools, instead of guessing from someone else's averages.

Asset Location: Free Money Hiding in Plain Sight

Asset allocation decides what you own. Asset location decides where you keep it, and it's honestly one of the most valuable and least talked-about moves you've got available.

The Easiest Money You'll Ever Make

Done right, smart placement can add roughly 0.25 to 0.75 percent a year in after-tax return without you changing a single one of your investments. That's found money.

The logic is simple. Different funds get taxed differently, so you put each one where it stings the least:

| Fund Type | Best Location | Why |

|---|---|---|

| Bonds & REITs | Tax-advantaged (IRA, 401(k)) | Income taxed at higher ordinary rates — shelter it from yearly taxation. |

| U.S. Stock Index Funds | Taxable brokerage | Low turnover and qualified dividends make them tax-efficient already. |

| International Stock Funds | Taxable brokerage | Throws off a foreign tax credit you can claim — that credit vanishes if held in an IRA. |

Two people can own the exact same three funds and end up thousands of dollars apart over time based on this alone. If you've got both a taxable account and an IRA, spend an hour getting the placement right. It pays off better than almost anything else on this whole list.

Tuning the Core: Optional Tilts

The three-fund portfolio is a complete meal all by itself. But if you want to chase a few specific premiums, you can add up to three tilts. Just treat these like seasoning, not the main course.

Four-Fund: Small-Cap Value Tilt

Move about 10% of your U.S. slice into a dedicated small-cap value fund. The long-run premium is real in the data, but it shows up in long, uneven cycles — small value trailed the S&P 500 for a good chunk of 2008–2024, roughly 8.6% versus 9.8% annualized in one long window.

Five-Fund: Emerging Markets Accent

Carve 10% off your international slice for emerging markets. High expected returns and high volatility — historically around a 6% 30-year return with a rough 22% standard deviation. A 3–10% slice adds growth potential without shaking the whole portfolio apart.

Six-Fund: Real Estate

A small REIT allocation adds real estate to the mix — one of the tools some retirees lean on for an inflation-proof retirement portfolio. Some experienced index investors skip a dedicated REIT fund entirely, figuring its returns are already mostly captured by small-cap value. Reasonable people land on both sides of this one.

REIT Tax Treatment: What Changed in 2025

REITs have to hand out at least 90 percent of their taxable income, and most of those dividends get taxed at ordinary rates as high as 37 percent — that's why the classic rule says keep REITs out of taxable accounts. That rule still holds. But REIT dividends also qualify for the Section 199A qualified-business-income deduction, letting you deduct 20 percent of that dividend income before tax. The One Big Beautiful Bill Act, signed July 4, 2025, made that 20 percent deduction permanent, wiping out the sunset that had been scheduled for the end of 2025. (An increase up to 23 percent passed the House but got dropped from the final law, so the rate stayed at 20 percent.) The tax drag is real, but the 199A deduction takes a solid bite out of it, and that break is now locked in instead of expiring on you.

The Even-Easier On-Ramp

If three funds still sounds like more than you want to babysit, and honestly, for a lot of retirees the whole goal is zero babysitting, you've got even simpler options. And these options defuse the single biggest risk of all: your own behavior when the market's falling.

A single target-date fund (Vanguard's run about 0.08%) holds all three asset classes, rebalances itself, and automatically gets more conservative as you get older. Or a single total-world stock fund like VT owns nearly every investable stock on Earth in one ticker. Either one rebalances on its own and takes away the temptation to go in and fiddle.

Think of it like a ladder. VT or a target-date fund is the bottom rung, hands-off and easy. The three-fund portfolio is the next rung up, a little more control and lower cost in exchange for you rebalancing once a year yourself. The four-, five-, and six-fund tilts sit up top for the folks who really want to fine-tune. And listen, there's zero shame in staying on the bottom rung. The best portfolio in the world is the one you'll actually leave alone.

What to Do This Week

You don't need a tangled web of high-fee funds to retire well. You need low costs, broad diversification, and the discipline to stay put when things get scary. Start by modeling your own numbers at ReadyAimRetire.com so you know where you actually stand before you buy a single fund. Here's where to start:

🎯 Your Action Plan This Week

- Pick your split. If retirement is more than 15 years off, an 80/20 stance is a fine default. If you're in the red zone, lean toward 60/40 or 70/30.

- Buy the three funds (or one target-date fund) at a low-cost provider, and set your contributions to automatic. Automatic is your friend.

- Max out what you can. For 2026, that's up to $24,500 in a 401(k) and $7,500 in an IRA, with an $8,000 catch-up once you hit 50, and a bigger $11,250 "super catch-up" for ages 60 to 63. One heads-up: high earners — folks who made more than $150,000 in prior-year wages — now have to make their catch-up contributions as Roth, one of several SECURE 2.0 changes taking effect in 2026 worth knowing about.

- Place your funds by tax type, keeping bonds and REITs tucked into sheltered accounts.

- Rebalance once a year, or when any slice drifts 5 percent off target. Vanguard found that annual rebalancing and much more frequent rebalancing produce nearly identical results, so all that extra tinkering just adds work, not return.

Set it up, automate it, and let time and low costs do the heavy lifting for you. That's the whole strategy. And yeah, it's boring on purpose. Boring is what works.

Thanks for reading if you've made it this far. Now go set it up and get back to your life.

Peace!