Rethinking the Golden Number: Why the Path to Financial Independence Is Broken (And How to Fix It)

Right now, somewhere in America, there's a 70-year-old logging into a brokerage account and staring at a balance that's bigger than the day they walked away from work. Not "bigger once you squint at inflation" bigger. Actually bigger. They've been retired for twenty years, and instead of spending their money, they grew it.

Here's what the data on early retirement spending actually shows:

- Most retirees still hold roughly 80% of their pre-retirement savings nearly two decades into retirement — reaching the number doesn't mean you'll ever spend it.

- Lean FIRE and Fat FIRE share the same blind spot: both optimize the balance and assume the human being will just start spending. Most don't.

- Three psychological traps sabotage FIRE savers: treating the number as an emotional cure, letting the spending muscle atrophy, and turning frugality into a status game.

- The 4% rule just moved. Bill Bengen raised his own "safe" withdrawal rate to 4.7% in 2025 — but that assumes a 30-year retirement. Early retirees should plan closer to 3.25%–3.5%.

- A blended strategy, raising income and cutting costs together, reaches financial independence almost as fast as extreme frugality, without locking in a bare-bones life.

- A 2026 wrinkle: expired ACA premium tax credits bring back a subsidy cliff that can cost early retirees five figures if they misjudge their MAGI.

The hard part was never reaching the number. It's learning to spend it.

And here's the thing. That's not some rare feel-good story. It's one of the most common ways financial independence actually plays out, and honestly, it's one of the quietest money tragedies going.

BlackRock and the Employee Benefit Research Institute dug into this, and what they found stopped me cold. Most retirees still had about 80% of their pre-retirement savings nearly two decades into retirement. It's more pronounced for the folks who saved the hardest. The higher-asset retirees still had 83% of their money sitting there 18 years in, and 42% of them were still hanging onto at least 80% of their original nest egg a full 21 to 22 years later. More than a third of retirees don't just protect their pile. They keep growing it, with balances still climbing past age 85. It's such a consistent pattern that it has a name of its own: why most retirees die with too much money.

These people won. They nailed the spreadsheet. They hit the number. And then they found out the number was never the hard part.

That's the crack running right down the middle of the FIRE movement (Financial Independence, Retire Early), and it isn't a math problem. The math is gorgeous. The movement proved something genuinely wild: regular households can save 40% to 70% of their income and reach financial independence decades early, in a country where the average person saves just 3.6% of their disposable income. That's real. The trouble shows up on the far side of the finish line, when a lifetime of saving muscle runs smack into a spending muscle nobody ever bothered to train.

Two Roads, One Blind Spot

When people decide they're done with the standard 40-year career grind, they usually pick one of two lanes. (If you want the full spectrum, we've mapped out the different flavors of FIRE in more detail.)

Lean Independence

- Typical annual budget $30K–$50K

- Portfolio target (25x) ~$750K–$1.25M

- The trade Total lifestyle minimalism

Fat Independence

- Typical annual budget ~$120K

- Portfolio target (25x) ~$3M

- The trade Bigger number, same fear

Now here's the part no spreadsheet ever warns you about. The fat retiree with $3 million and the emotional room to actually enjoy a business-class seat? Still going to wince when it's time to click "book." And the lean retiree who spent fifteen years treating every purchase like a pop quiz on their character doesn't suddenly loosen up the second the account crosses seven figures. Both roads have the exact same blind spot. They optimize the number and just kind of assume the human being will fall in line. The human being, most of the time, does not.

The Three Traps That Turn Freedom Into a Locked Room

Let me be fair, because the FIRE movement has earned a lot of respect. It blew up the lazy old idea that a 10% savings rate is something to brag about. But that laser focus comes with a bill, and it shows up as three pretty predictable head games.

Trap 1: Thinking the Number Is a Cure

A lot of wealth-builders quietly tell themselves that some specific net worth is going to fix how they feel. Hit $1.5 million and the worry just switches off. It doesn't work like that. A person's emotional relationship with money has almost nothing to do with the balance in the account.

You can see the proof in the "magic number" itself, which turns out not to be a number at all. Ask Americans what they need to retire comfortably and you get $1.26 million from Northwestern Mutual's 2025 study, $1.6 million from Charles Schwab's 401(k) survey, and $2.1 million from a BlackRock poll. Those answers are more than half a million dollars apart, and the guesses from higher earners run past $2.6 million. If this were an actual mathematical fact, the numbers would land in the same spot. They scatter because the "number" is really just a feeling wearing a dollar sign. Chasing it like it's a cure is chasing a feeling you've decided to put off.

Trap 2: The Spending Muscle Goes Soft

To yank retirement forward by decades, people often white-knuckle their way through ten or fifteen years of hardcore frugality, promising themselves they'll enjoy the money later. Trouble is, human psychology isn't a light switch.

Spending money well is a skill, and skills get rusty when you never use them. Spend your prime adult decades over-training the saving muscle while the spending muscle just withers, and you're basically carving deep grooves of money fear into your brain. Do it long enough and those grooves set like concrete.

"I don't even have the muscle to spend money. When we have a surplus, what do I do? Pay down debt."

Ramit Sethi, who wrote I Will Teach You to Be Rich, had a guest from the FIRE world nail this perfectly. She was sitting on a big surplus and admitted as much. She's got the money. She flat out cannot enjoy it.

And there's a real irony buried in here. Mr. Money Mustache, one of the founding voices of this whole thing, once wrote a post literally called "Frugality as a Muscle." The community trained that one muscle so hard that the opposite one just went slack. David Blanchett over at Morningstar calls the result an identity problem: you've seen yourself as a saver for decades, so spending more feels wrong in your gut even when the spreadsheet is sitting right there telling you it's totally safe.

Trap 3: Turning Doing Without Into a Trophy

In a lot of financial independence corners of the internet, there's this competitive undercurrent where the person who suffers the most and spends the least gets the gold star. It quietly becomes a status game. Well-off members feel judged for buying a nice car or a comfortable seat, so they just don't.

Haley Sacks, better known as Mrs. Dow Jones, called the extreme end of FIRE a "sham," comparing it to "financial anorexia." That's a heavy phrase, but her point is that it's so much doing-without that it warps how you see things. You end up convinced you always need "a bit more" while you're visibly going without. Money deserves respect, discipline, and smart investing. I believe that all the way down. But at the end of the day it's a tool, and tools are meant to be used to build a richer human life. A tool you refuse to ever pick up isn't an asset. It's just a little monument to fear sitting on the shelf.

The Number Everybody Argues About (aka the Safe Withdrawal Rate)

Before we get into how you actually speed up the timeline, we've got to clear up the single most misunderstood figure in the whole movement: the withdrawal rate.

Definition

The Safe Withdrawal Rate: It's not a guess about the return your money earns. It's the slice of your portfolio you can pull in year one, then bump for inflation, with a good chance of not running dry. Bill Bengen worked it out back in 1994. Your investments still have to go earn their own return underneath the whole thing.

And even that number is moving now. In his 2025 book A Richer Retirement, Bengen bumped his own "safe" rate up from 4.0% to 4.7%, pointing to a more diversified portfolio. So the guy who invented the frugal rule spent 2025 telling retirees to spend more, and warning that inflation, not overspending, is a retiree's "greatest enemy." (We break down exactly what changed in why the 4% rule is broken in 2026.)

Here's the wrinkle that separates a solid plan from one that blows up on you: Bengen's 4.7% assumes a 30-year retirement. If you retire at 40, you're planning for 45 or 50 years, and sequence-of-returns risk (a rough first decade hurts you way more than a so-so long-run average) drags that safe rate down. Researchers like Wade Pfau, Michael Kitces, and the Early Retirement Now crew put the safe withdrawal rate closer to 3.5% at 40 to 45 years, and around 3.25% at 50 years. A 40-year-old who grabs Bengen's shiny new 4.7% is quietly borrowing against a retirement that might just outlive the math.

Every retirement plan is different, and the right rate for you depends on your own time horizon, spending pattern, and portfolio mix, not an average pulled from someone else's 30-year plan. ReadyAimRetire lets you test how these withdrawal assumptions play out against your specific numbers instead of borrowing a rate that may not fit your timeline.

So there's no single golden number. There's a range, and where you land inside it comes down to how long your money has to stretch.

Three Blueprints for Speeding Up the Crossover Point

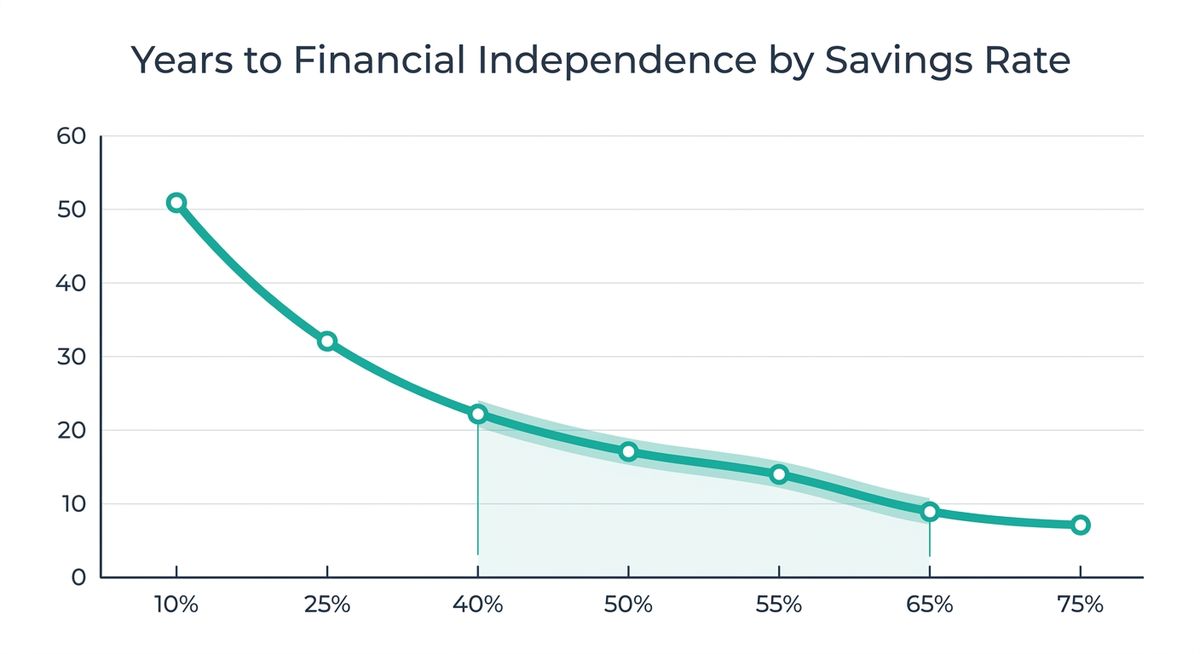

Okay, the practical part. What actually moves your timeline is not your income. It's your savings rate, the percentage of your take-home pay you get to keep. That one idea, made famous by Mr. Money Mustache's "shockingly simple math," rearranges everything.

Assuming a 5% real return, a 4% withdrawal rate, and roughly $0 to start, here's what the working years to financial independence look like:

| Savings rate | Approximate working years to FI |

|---|---|

| 10% | ~51 |

| 25% | ~32 |

| 40% | ~22 |

| 50% | ~17 |

| 55% | ~14.5 |

| 65% | ~10.5 |

| 75% | ~7 |

Now let's make it real. Take a household with $80,000 in take-home pay and $6,000 a month in expenses ($72,000 a year). That leaves just $8,000 going into savings, a 10% rate, and a finish line sitting about half a century out. Here are three ways off that treadmill.

| Blueprint | Strategy | Savings rate | Timeframe | Portfolio target | The trade-off |

|---|---|---|---|---|---|

| 1. Aggressive cost-cutting | Cut monthly expenses in half, to $3,000 ($36,000/yr) | ~55% | ~14 to 15 years | $900K (25 × $36K) | Fast, but locks in a permanently tight lifestyle |

| 2. Income optimization | Keep your lifestyle, land a 30% raise, invest 100% of it | ~31% | ~27 years | $1.8M (25 × $72K) | Slower, but keeps a comfortable $72K baseline |

| 3. The blended approach | Raise income 30% and cut expenses 30%, spending $50.4K | ~51% | ~17 years | $1.26M (25 × $50.4K) | Nearly as fast as cutting alone, at a much more livable spend |

Look at what the honest math is telling you here. Pure cost-cutting (Blueprint 1) is technically the quickest, but you buy that speed with fifteen years of going without and a permanent $36,000 lifestyle waiting at the end. The blended approach gets you to independence only a couple of years later while letting you live on $50,000. That combo, real speed plus a life you'd actually want to live, is why the blended path is the sweet spot for most families. Attacking one side of the ledger is a diet. Attacking both is a strategy.

You can run these numbers for your own situation at ReadyAimRetire to see which blueprint gets you to your own crossover point fastest, instead of guessing at the trade-offs from a table built around someone else's income and expenses.

The 2026 Curveball the Spreadsheet Never Sees Coming

If you needed one last bit of proof that FIRE can't be boiled down to a formula, 2026 served it up on a plate.

The beefed-up Affordable Care Act premium tax credits expired in January 2026, and the old subsidy cliff came roaring right back. For a two-person household, the line sits at $84,600 of modified adjusted gross income (MAGI). Earn one single dollar over that, and you lose the entire subsidy. For folks who were getting subsidized, the average out-of-pocket premium more than doubled once the enhanced credits lapsed, jumping an estimated 114%, and the old repayment caps are gone. So a couple that overshoots can owe back $10,000 or more come tax time. Picture a 52-year-old couple retiring on $85,000 of portfolio income: on paper, they cleared the cliff by a few hundred bucks, and now they owe back $12,000 in premium credits. That's a five-figure surprise the spreadsheet never breathed a word about.

How to Stay Under the Cliff

Qualified Roth withdrawals are MAGI-neutral, meaning they don't count toward that ACA income line, which makes Roth the most subsidy-friendly place to spend from. Pre-tax contributions, HSA deductions, and the self-employed health-insurance deduction can all pull your MAGI back under the cliff. Some early retirees sidestep the cliff a different way entirely, by picking up part-time work with benefits attached; see how a part-time bridge can protect your health insurance for how that trade-off works.

Financial independence in 2026 isn't a balance you reach and forget. It's a set of decisions you keep making, year after year.

Redefining the Goal

Here's the reframe that flips financial independence on its head. Both earning more and spending on purpose are skills. Neither one was handed to you at birth, and neither one is optional. You've spent your whole working life training one of them. The job ahead is to train the other one before you need it, not after.

The Confidence Gap Is the Real Crisis

Among pre-retirees 55 and older, 57% of the ones with a decumulation plan feel highly confident they can manage their spending, versus just 26% of the folks flying blind. Retirees with guaranteed, annuitized income spend roughly twice as much as people holding the same amount in a regular savings account, not because they have more, but because the permission is built right in.

The anxiety keeping nearly half of retirees from ever touching their savings doesn't get cured by a bigger balance. It gets cured by a plan.

So start now, wherever you are on the road:

🎯 Start Training the Muscle You've Never Used

- Practice spending while you're still working. Pick one "money dial," one category you genuinely love, and spend on it on purpose this year. You're training a muscle, and muscles need reps before game day.

- Write a decumulation plan, not just a savings goal. Decide ahead of time which accounts you'll pull from, in what order, and how that plays with your MAGI and your subsidies.

- Match your withdrawal rate to your real time horizon. Use 4.7% only if you're planning for 30 years. If you're retiring early, start down near 3.25% to 3.5% and adjust from there.

- Pick a blueprint on purpose. Blended for most people, aggressive if speed truly beats lifestyle for you, income-first if you flat out refuse to shrink your life. Mix them to fit your values, not some forum's approval.

Start by modeling your own retirement at ReadyAimRetire to see where your number and timeline actually land before you commit to a blueprint.

The Crossover Point was never supposed to be a wall you crash into and stop. Vicki Robin and Joe Dominguez, who came up with the term in Your Money or Your Life, didn't even tell people to retire the second they hit it. The real destination isn't running away from work. It's automating your finances so completely that work turns into a choice you make on a Monday morning because you want to, not a sentence you're serving because you have to.

That's the number worth chasing. Not the one in the account. The one that finally lets you spend it.